The Currency

Be current.

Be current.

Get insights and intel on your money.

*If you’re already registered with Empower, please use the same email address as your existing account.

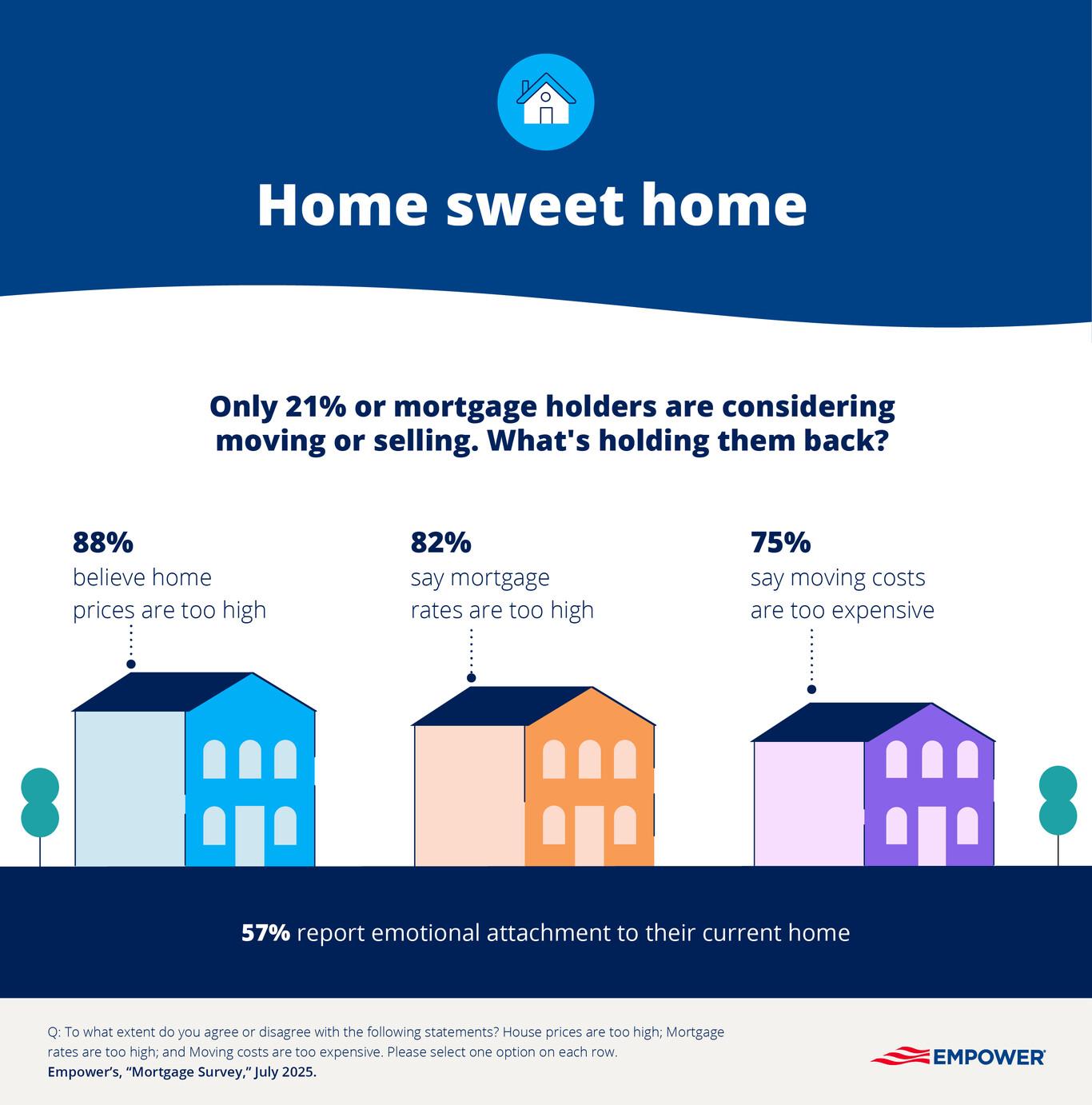

According to Empower research, more than a quarter of mortgage holders have a mortgage rate between 3% and 3.99%, and the housing market has taken on new dynamics:

According to Empower research, more than a quarter of mortgage holders have a mortgage rate between 3% and 3.99%, and the housing market has taken on new dynamics:

Explore by topic

🛤️ Stay on track

Money

Theme Slug

category--money

Pathauto Slug

money

Nearly half (47%) of Americans wish for a “do-over” on savings, making every opportunity to maximize returns count. Here's this month's money news.

Becoming the 401(k) millionaire next door

Life

Theme Slug

category--life

Pathauto Slug

life

The amount of retirement millionaires continues to grow, according to Empower data, with 21.9% of Americans falling into this category of retirement savers.

What is the five-year rule for a Roth IRA?

Life

Theme Slug

category--life

Pathauto Slug

life

Learn the Roth IRA 5-year rule, when the clock starts, how conversions differ, and what can happen with early withdrawals.