The Currency

Be current.

Be current.

Get insights and intel on your money.

*If you’re already registered with Empower, please use the same email address as your existing account.

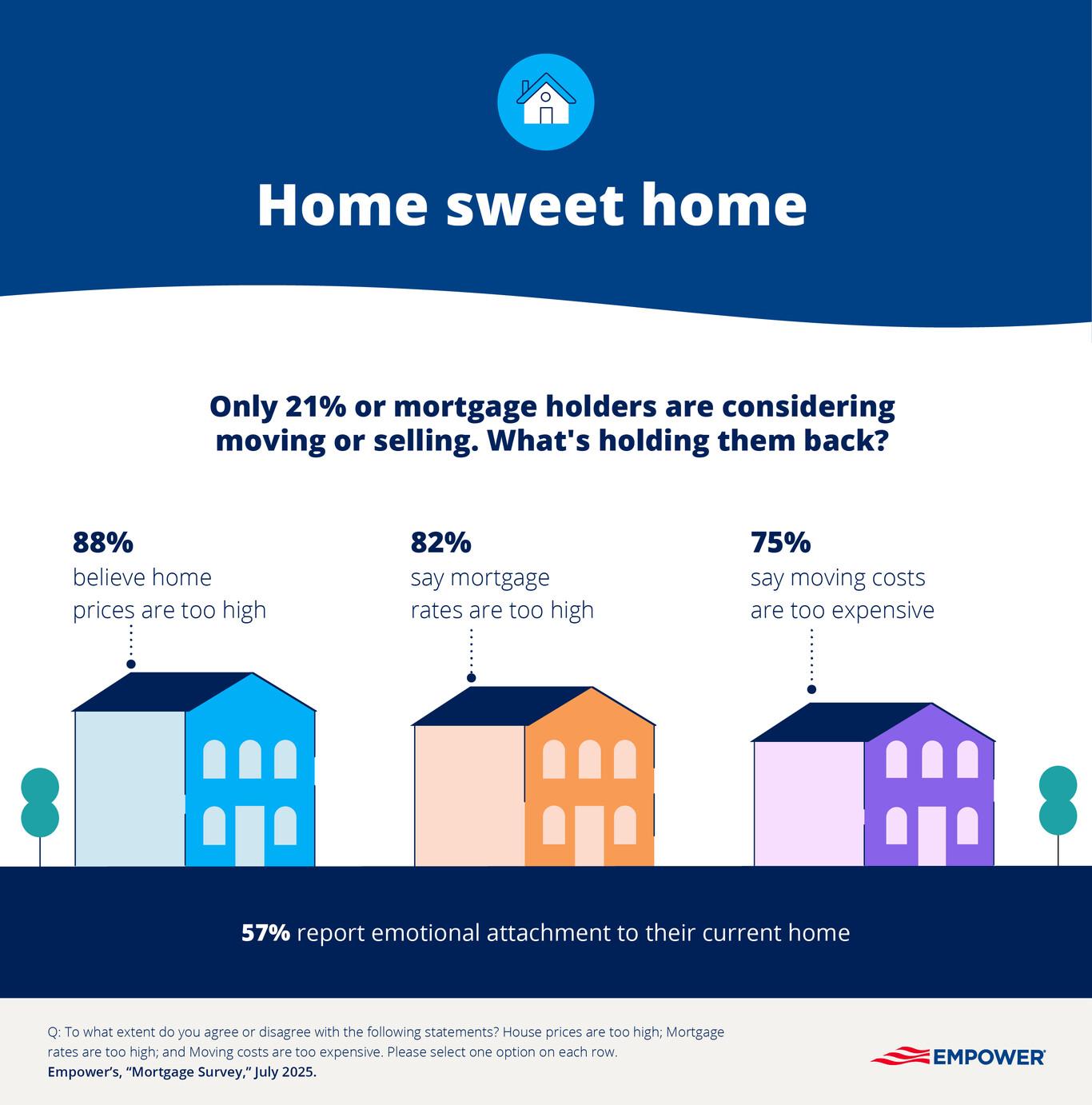

According to Empower research, more than a quarter of mortgage holders have a mortgage rate between 3% and 3.99%, and the housing market has taken on new dynamics:

According to Empower research, more than a quarter of mortgage holders have a mortgage rate between 3% and 3.99%, and the housing market has taken on new dynamics:

Explore by topic

SIMPLE IRA contribution limits in 2026

Money

Theme Slug

category--money

Pathauto Slug

money

Learn the 2026 SIMPLE IRA contribution limits for employee deferrals, catch-ups, and employer contributions. Discover key deadlines and how to maximize savings

What is a high-yield savings account?

Money

Theme Slug

category--money

Pathauto Slug

money

Learn how a HYSA works, when to use one, and how it can fit into a well-rounded financial plan.

What is a Health Reimbursement Arrangement (HRA)?

Life

Theme Slug

category--life

Pathauto Slug

life

A health reimbursement arrangement (HRA) is an employer-funded benefit that reimburses eligible medical costs while offering potential tax savings