Between the margins May 2026

May 2026

Market recovery part deux

May 2026

Market recovery part deux

Executive summary

- The April recovery bears a striking similarity to the recovery after Liberation Day.

- It’s not just the fierceness of the rally; it’s the catalyst: AI to the rescue again.

- This isn’t random; we can learn a few things from what we’ve seen:

a. Take care in interpreting headlines.

b. Expect AI “moments of doubt.”

c. Watch valuations, not prices.

Nearly one year after Liberation Day, the world awoke to another surprise: A war in Iran. And just as it did a year ago, the market staged a massive recovery after an initial sell-off.

In both cases, we can thank artificial intelligence (AI).

Sure, other factors were at play. In 2025, the Trump administration gave the market some breathing room by reducing tariffs from the more extreme April 2 levels. In 2026, the hot war evolved into a blockade, still restricting passage through the Strait of Hormuz, but with ongoing negotiations rather than daily bombings.

However, while those developments may have staunched the market’s losses, it was the roar of AI that spurred its acceleration.

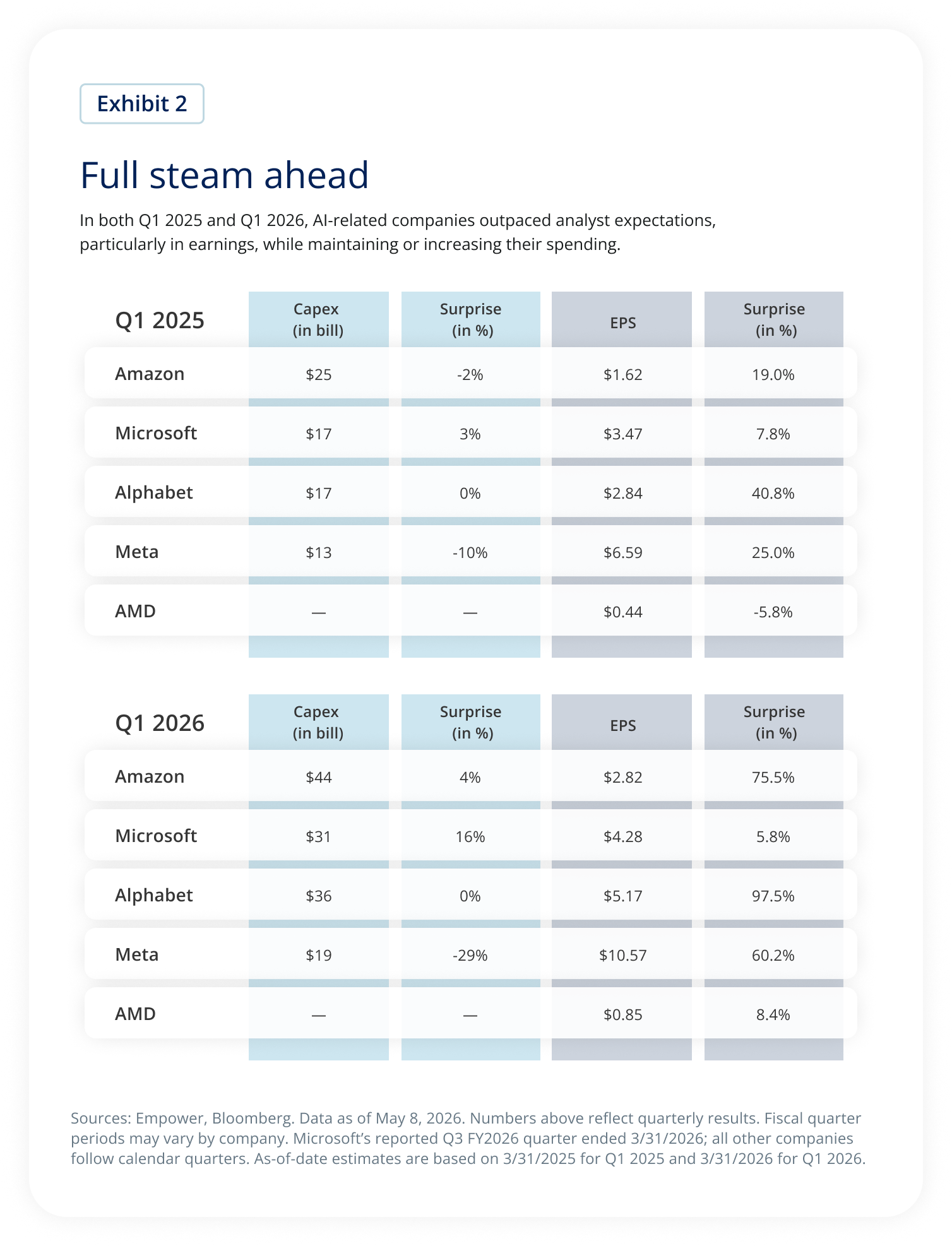

As Q1 2025 earnings season unfolded after Liberation Day, companies at the center of the AI trade — think the hyperscalers,1 Meta, and the chip companies — announced surprisingly strong earnings growth, and, in the case of the hyperscalers, continued investment in the AI build-out.

We’ve seen much the same during Q1 earnings season in 2026, which has transpired amid continued turmoil in the Middle East. Nvidia won’t report until May 20, but others among the “AI A-List,”2 including the hyperscalers, not only increased their spending plans, benefiting chip companies, but showcased eye-catching earnings growth tied to their core business plans and AI.

Here’s another similarity. In both 2025 and 2026, these AI names entered Q1 earnings season in a malaise. In 2025, China’s DeepSeek — an effective AI model built at a far lower cost — caused investors to question the seemingly profligate spending by U.S. AI names.

In 2026, AI companies weren’t in freefall, but they’d lost their shine since their peak on October 29, 2025. Investors worried about circular financing; AI demand; and, of course, the spending. This resulted in weak returns for five months, though earnings continued to deliver.

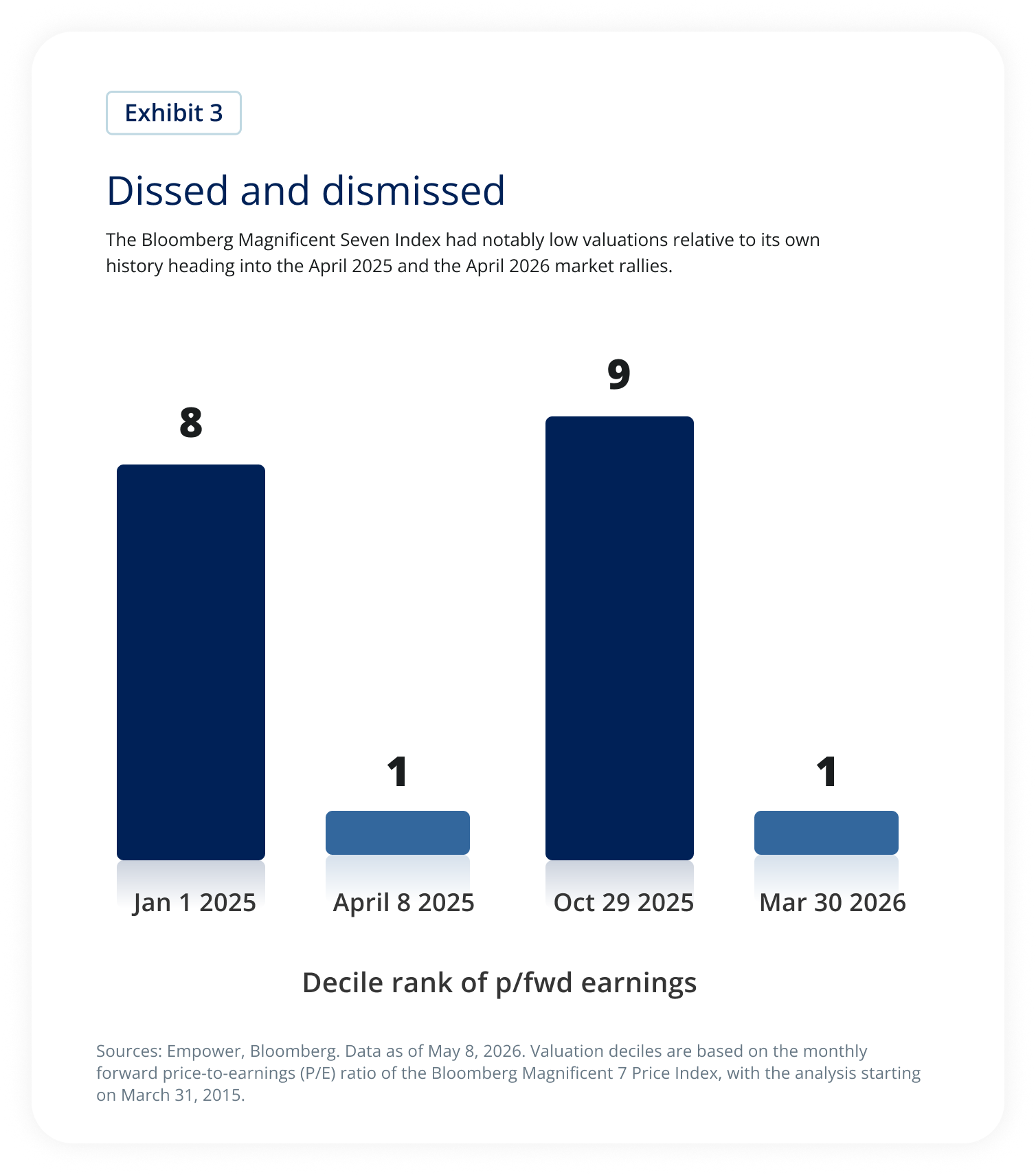

In both years, valuations reflected the poor showings. As shown in the chart below, by the market bottom on April 8, 2025, the Bloomberg Magnificent 7 Index,3 home to a number of these companies, traded in the first decile of its own history. It was similarly priced on March 31, 2026, sitting once again in the first decile of its own history.

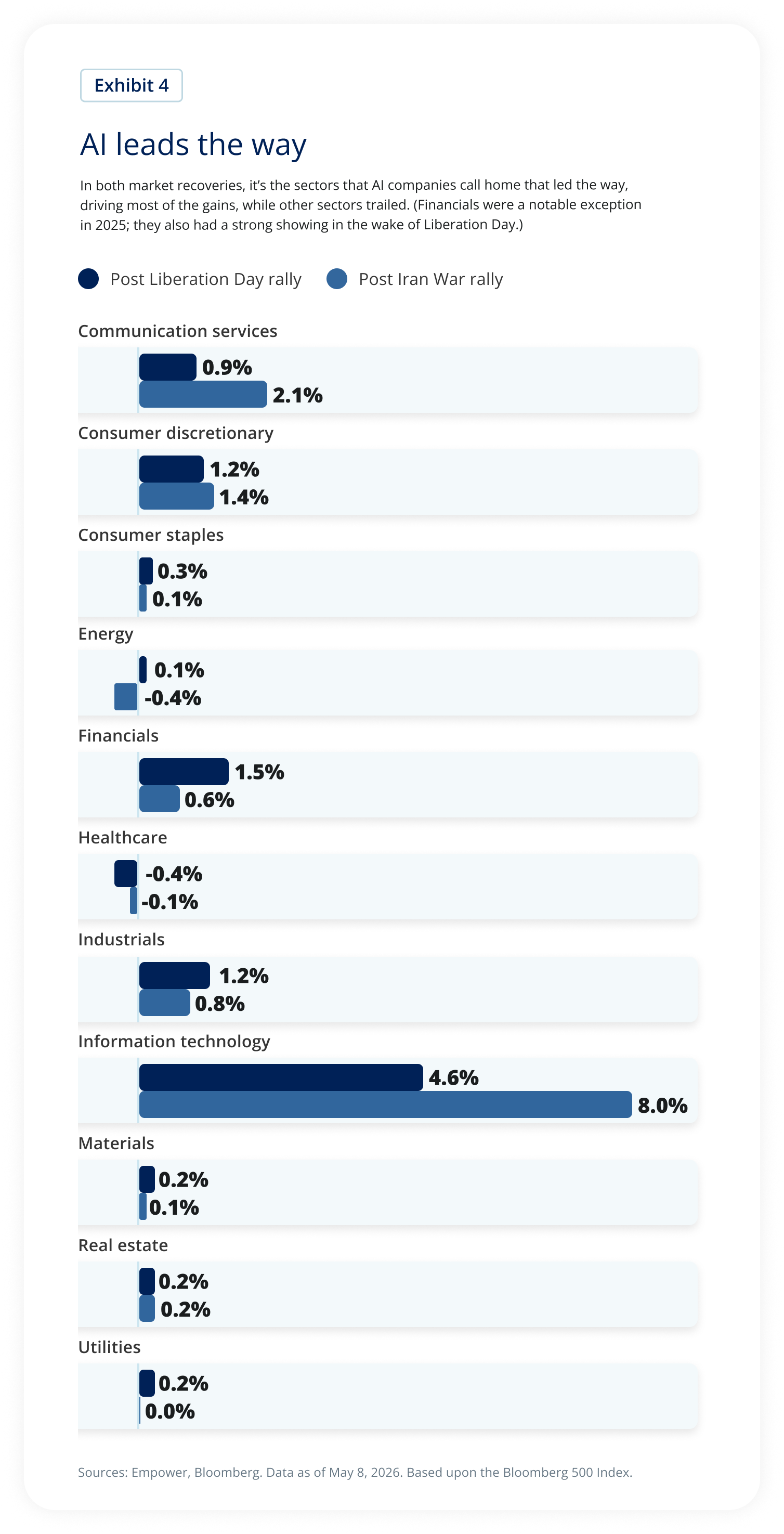

Broad market performance reflects the impact of the AI-A list, and other related companies like memory chips. In the spring of 2025 and again in April 2026, the technology, consumer discretionary, and communication services sectors — home to many of these names — drove the results of the broader index, with other areas of the market lagging behind.

Investment implications: The “So what?”

OK, great, so AI to the rescue twice. But is there anything we can take from these very similar situations to frame our expectations for the market and the economy? Relatedly, how do we manage portfolios in a world that feels less predictable than ever?

Actually, I see three principles to help guide investors in the current climate.

First — and, ironically, this relates to the second question: Take care in interpreting headlines.

It’s so tempting to translate headlines directly to the economy or markets. Not just for individual investors, but also for the professionals out there. Most of us struggle with multi-variable analysis; we see a big headline — “Oil above 100!” — and suddenly that’s the only variable that matters, and it matters immediately.

But the reality is that the U.S. economy is complex and broad, and we can rarely assume a single variable will have a one-for-one impact on the whole.

Does that mean higher oil prices don’t matter? Nope, they absolutely do, and the longer they stay high, the more they matter. But we should consider their impact in the broader context of a developing AI economy and a U.S. consumer who isn’t heavily indebted, is generally employed, and has tax rebates hitting their accounts at the same time as they’re shilling out more dollars for gas.

Second: Expect periodic “moments of doubt” when it comes to AI.

I’ve written regularly about this. The build is long. And expensive. And no one — not even your favorite AI CEO — knows exactly what the future looks like in an AI world. As we wait for clarity to slowly emerge, investors can emotionally bounce from the risks around AI to the opportunity it may unlock. This can lead to periods of strength and “moments of doubt.”

I’d argue we saw a “moment of doubt” with DeepSeek in the first half of 2025. And we saw another one this past winter as investors fretted about spending, returns on investment, and circular financing.

That brings me to my last principle: Watch valuations, not prices.

We put a lot of stock in how much the market moves any given day. But when it comes to what matters, price is only the numerator. We should also keep an eye on the denominator: the underlying value.

A big disconnect between the two can signify either risk or opportunity.

Think about this in the context of AI “moments of doubt.” Investors can grow too pessimistic on AI, focusing inordinately on the spending while dismissing the potential upside from returns on those investments. They can worry about customer concentration or a lack of immediate monetization — concerns top of mind for investors at the start of this year. And as those worries consume investors, we can see prices fall dramatically, no longer reflecting any upside to the AI trade.

I’d argue these periods of pessimism could offer opportunity; here in Empower’s Strategist Office, we’ve pointed out the growing valuation discrepancy over the course of 2026 as select AI stocks disappointed.

The reverse can also occur. If investors grow optimistic about an AI future, they could push prices higher — perhaps a bit too enthusiastically. Since we don’t fully understand the challenges we’ll face as AI develops, this creates the risk of future disappointment. Periods of excessive valuation become a reason to potentially lighten up on exposure to companies at the core of AI.

There’s another application of this valuation focus that we can apply to the market as a whole. An eye on the underlying value often keeps you invested. While prices can bounce around a great deal — as they should in a big, liquid market — underlying value typically doesn’t move all that much. Scary headline and major market drop? Take comfort: It’s unlikely businesses are worth far less than they were the day before.

Looking ahead

Nvidia looms large on May 20, with key questions related to whether it will retain its dominance as competitors chase. We also face a Fed transition: We’re on the cusp of the Kevin Warsh era, which appears especially bumpy given the oil-driven surge in inflation and Jerome Powell’s decision to stay on the Federal Reserve Board of Governors for the foreseeable future. And of course we have the war in Iran. Plus, we’re tracking IPO developments, and we’re watching the consumer to continue to evaluate whether the data supports our view that the U.S. economy remains resilient.

Sounds like we’re headed for a busy summer.

Our mission is to empower financial freedom for all Empower is a customer-obsessed financial services company delivering investment, wealth management, and retirement services to more than 19M people.4 The following tenets guide the development and management of products and solutions we provide to the investors we serve: Commit to an unwavering duty of care Our investors are our priority. We steward every dollar we invest with care, attention, and respect. Emphasize fundamental analysis We keep our eyes on the horizon by rooting our analysis in the underlying drivers of long-term investment returns, not fleeting news and noise. Plan for better outcomes through thoughtful diversification We build resilient portfolios by relying on thoughtful diversification that plans for a range of outcomes, rather than a narrow result. |

Explore previous editions

April 2026 | March 2026 | February 2026 | December 2025 I October 2025

Stay up to date |

1 Hyperscalers are large-scale cloud service providers that offer the computing, networking, and storage infrastructure required to support global-scale applications and data processing.

2 We define the AI A-List as an evolving group of companies involved in the AI build-out and early stage deployment. For the purposes of this commentary, the list includes Microsoft, Amazon, Meta, Alphabet, Oracle, Nvidia, AMD, and Broadcom.

3 The Bloomberg Magnificent Seven Index is an equal-weighted equity benchmark designed to track the seven closely followed mega-cap technology companies in the U.S. market.

4 As of September 30, 2025. Investing involves risk, including possible loss of principal.

Past performance, where discussed, is not a guarantee of future results. Historical trends and economic data discussed may not be indicative of future conditions which may change.

This material is for informational/educational purposes only; it may not be suitable for all investors, not tailored to any specific investor’s objectives or financial situation and is not intended as investment, legal, tax, or accounting advice.

The opinions expressed represent the current, good-faith views of Empower at the time of publication, are provided for limited purposes, and should not be relied upon as investment or legal advice.

This content is based on information available at the time and may change based on more current conditions. This is neither an endorsement of any security, index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index. References to asset classes or sectors are for illustrative purposes only and are not recommendations.

The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information.

Predictions, opinions, and other information contained in this communication are subject to change without notice and may no longer be true after the date indicated.

Bloomberg® and the referenced indices are trademarks or service marks of Bloomberg Finance L.P. and its affiliates. Bloomberg and any third-party providers are not affiliated with Empower and do not approve, endorse, review, or recommend the financial products referenced. Bloomberg does not guarantee the timeliness, accuracy, or completeness of any data related to the indices or financial products.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. INV-WMLPNV-WF-6303900-0526 RO5457017-0526