Between the margins March 2026

March 2026

New month, new narrative

March 2026

New month, new narrative

Executive summary

- The Iran war has lived up to the reputation of a classic geopolitical event: Few saw it coming.

- I'd argue long-term investors shouldn't necessarily do anything as a result, but understanding the range of outcomes is still a useful exercise.

- In a worst-case scenario, analysis suggests we could see a hit to both inflation and growth should energy infrastructure suffer long-lasting damage.

- Meanwhile, I'd argue asset class performance during the conflict makes some sense, given the risks the market faces in this environment.

- So is the volatility creating opportunity? Maybe on the margin.

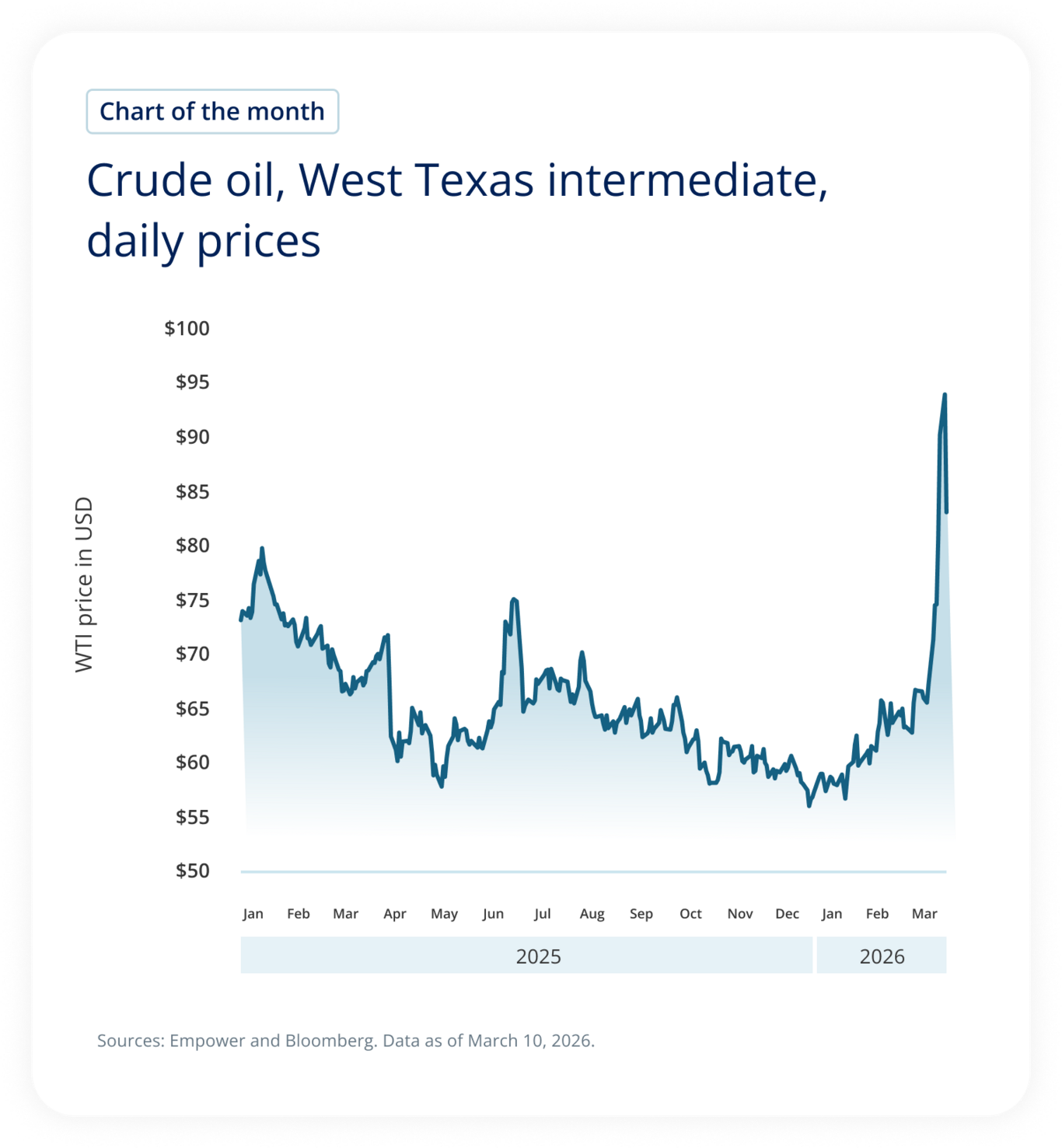

After Israel and the U.S. began their offensive on February 28, the energy market turned the page to a new chapter, as demonstrated by oil prices in our Chart of the month.

Ranges from $72 to $95 from year 2025 to 2026

Immediately investors transformed from artificial intelligence (AI) experts to geopolitical wizards. However, the reality is that few of us (actually, none of us) know how this will play out. The war itself was a surprise; oil prices wouldn’t have been quite so low — with commentary focused quite so much on the global supply glut — if analysts and experts had seen it coming.

So. What’s a long-term investor to do?

Consider standing still. Geopolitical conflict is just one of the unknowns regularly thrown at markets, and, at least for most U.S. investors, a well-diversified portfolio in the past has generally weathered this kind of storm quite well.

But even for the stay-the-course types, framing expectations can be a valuable exercise. It helps take some of the edge off volatility by providing context and understanding for potential market moves. And, on occasion, it can give investors the information not just to survive the volatility but potentially take advantage of it.

In the current climate, a few contextual questions leap to mind: What is the range of outcomes when it comes to energy prices and the possible resulting impact on the economy? Also, thus far the reaction by certain asset classes doesn’t fit conventional understanding. Why not? And finally, if volatility is opportunity, where could the opportunity be today?

The range of outcomes: Energy prices

Let’s set the stage. About three-fourths of the energy in the U.S. comes from either oil or natural gas. With the U.S. the world’s largest producer of both, most of its needs are met domestically.1

In the midst of geopolitical conflict, that self-sufficiency offers a measure of protection for the U.S. economy, helping to limit the likelihood of 1970s-style shortages from oil or gas disruptions in the Middle East.

With natural gas still a regional market to some extent, the U.S. economy is also unlikely to see price shocks; in fact, we have seen only a 13% increase in gas prices since February 27 through March 12, while Europe, which sources gas supply from Qatar, among other places, has seen prices skyrocket 53% over the same stretch.2

Oil is a different story. As a global market, price movements overseas also impact U.S. prices, though generally to a slightly more moderate extent.

Consider the price moves on March 9. As fears of oil market disruption spiraled, Brent Crude, which measures the global oil market, peaked at $119.50 midday. West Texas Intermediate (WTI), which measures U.S. crude, similarly spiked, peaking at a similar level. (Both have since fallen, and as of March 12 hover just below $100/barrel.)

Therein lies the inflation concern for the U.S. economy, as high oil prices filter through to the broader economy. But what kind of price levels could we be talking about and for how long? And what does that mean for inflation, growth, or both?

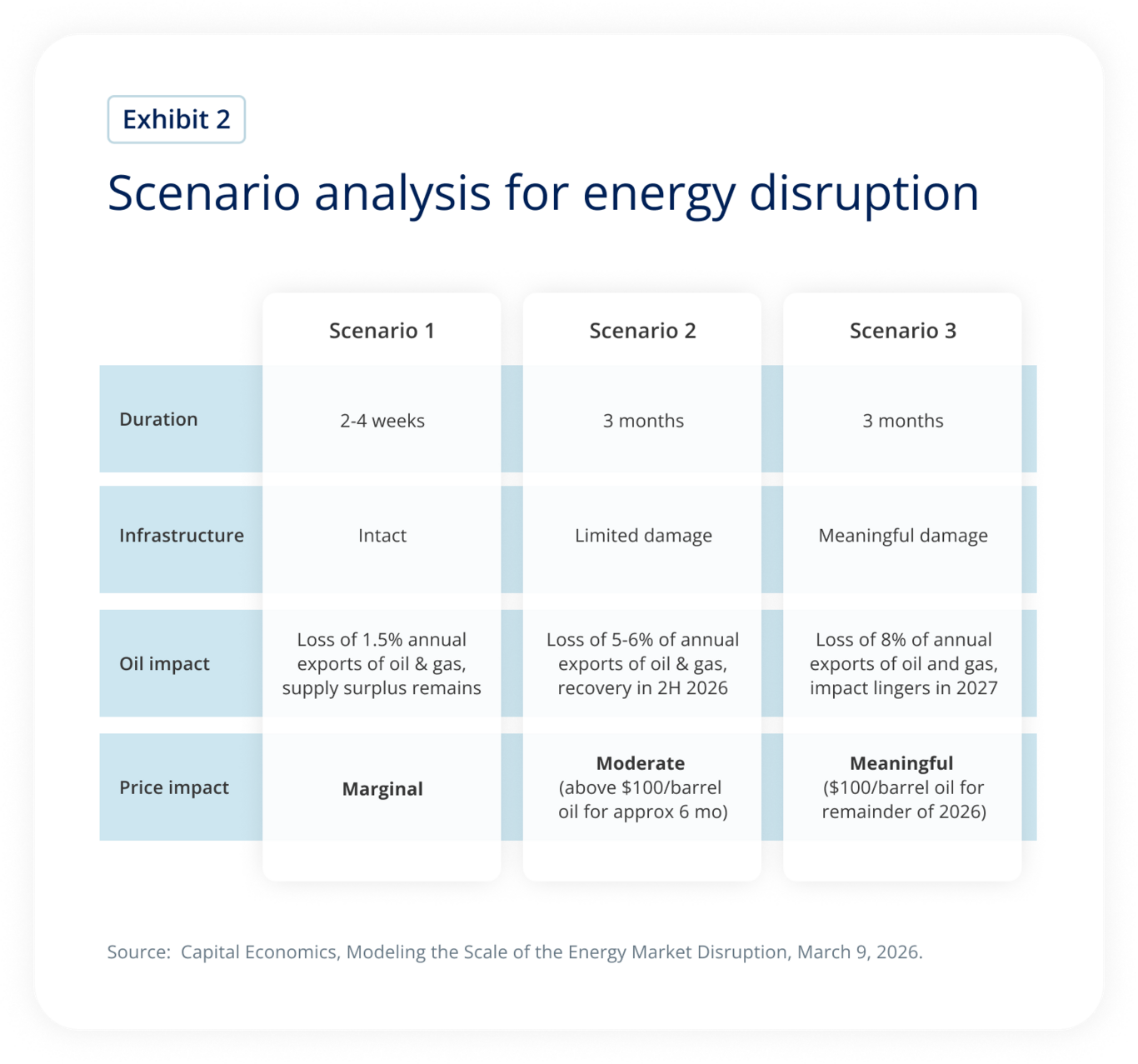

Here’s where the scenario analysis comes in handy. Capital Economics painted three different possible scenarios, the last of which focuses on the most severe disruption.

Based on research from the Federal Reserve Bank of Dallas, while Scenarios 1 and 2 could have an impact on headline inflation, the effects are likely near term in nature and likely to fade; in other words, they wouldn’t necessarily get ingrained in consumer inflation expectations and create a persistent inflationary surge.

If we are looking at the triple-digit prices for the better part of the year (Scenario 3), the inflationary impact is likely to be more severe and more persistent.

It’s hard not to imagine a knock-on growth effect as well for Scenario 3, as the extra cost could impact discretionary spending. That said, there are few caveats to (happily) report:

- The U.S.’s status as the world’s largest oil producer3 likely lessens the GDP hit.

- Research by Ben Bernanke and others suggest that it is a knee-jerk policy response to raise rates in the wake of the oil shock that causes the most damage to the economy, rather than the oil shock itself.

The market response

Feel better? As long as Scenario 3 exists somewhere in the ether, maybe not. For what it’s worth, Scenario 3 isn’t my base case, or even a high likelihood event (though, like all possibilities on the left side of the distribution, it’s not a zero-probability event either).

That’s what brings us to the matter of asset class performance. After all, we invest in diversified portfolios because we don’t know which of the three scenarios — or infinite scenarios! — will actually play out.

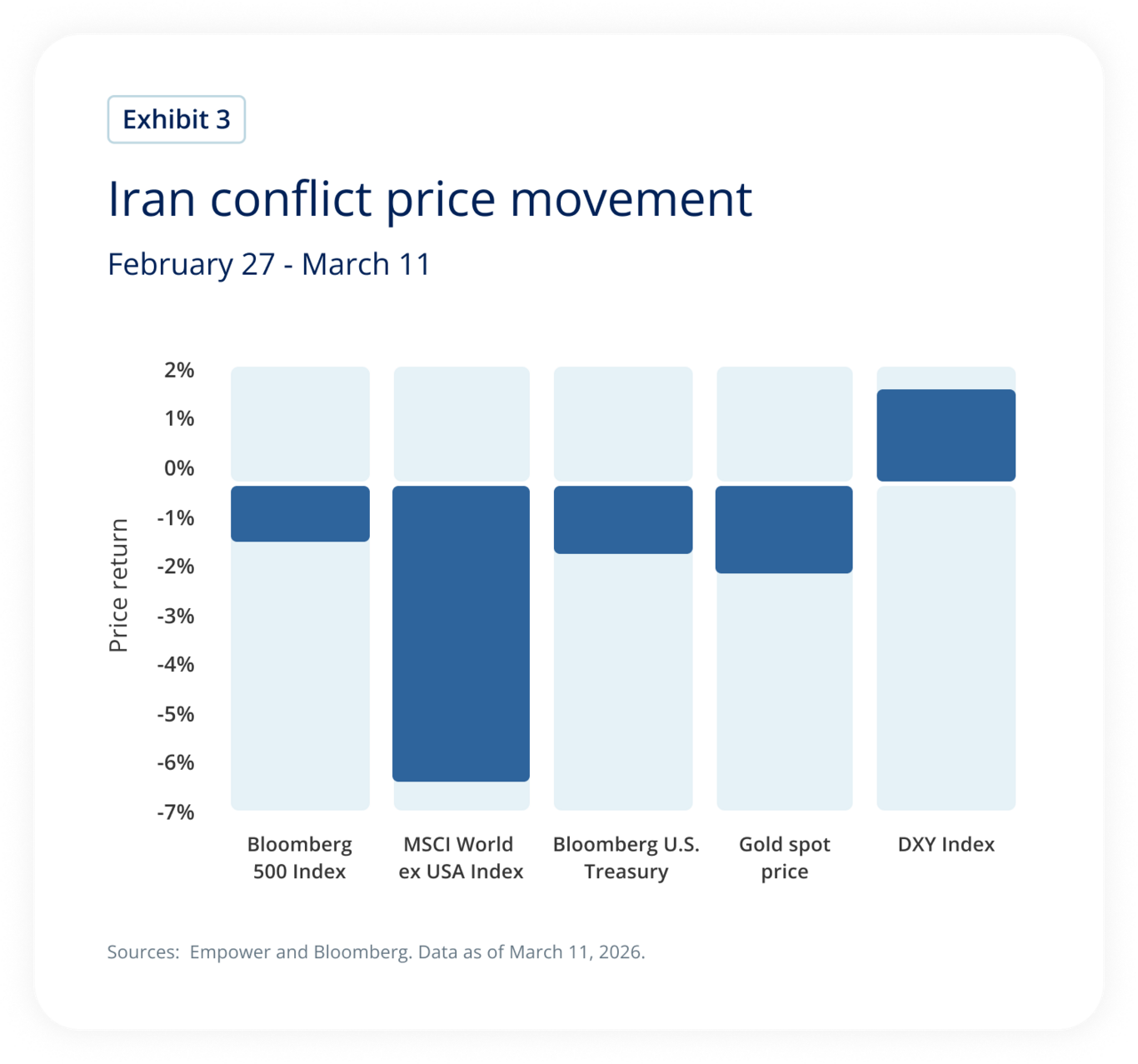

But those keeping a close eye on the day-to-day movements by their diversified portfolios may feel a bit frustrated. U.S. equities have held the line fairly well, slipping only modestly from near record highs over the course of the conflict. But non-U.S. equities have taken a tumble, gold has been a wash, and U.S. Treasuries have slipped a bit. Thank goodness for the good old U.S. dollar, which pushed back against the dollar bears to gain ground against other currencies.

Price return ranging from -6% to +1%.

What gives?

It’s a matter of the underlying dynamics of each asset class. Given the self-sufficiency I described earlier, U.S. stocks are far less exposed to energy disruption than non-U.S. markets, meaning the bulk of the fear is felt overseas.

Meanwhile, while U.S. Treasuries have historically acted as a hedge to equity market fears; in this particular case one of the primary fears is inflation. That hits Treasuries where they hurt, as Treasuries are a fixed-income asset, meaning that inflation eats away at their value.

What about gold? Sigh. As regular readers may have picked up (as always, hi Mom!), I find gold a bit irritating. Without cash flows, it’s hard to value, and it’s subject to technicals. Thus, while it historically has behaved as a store of wealth — not a bad thing to have in inflationary times — a growing contingent has instead treated it as if it were a creator of wealth. The resulting buildup has left it vulnerable to sudden stops or reversals, which may have contributed to its mediocrity recently.

And the U.S. dollar? Many expect an inverse relationship between oil and the USD. But that’s changed in recent years. For the millionth time, the U.S. is an energy exporter, and exporters tend to fare better during supply shocks, since they reap the benefits for the higher prices. There’s also the petrodollar consideration — as oil moves higher, buyers need more dollars to buy it — and the safe haven trade; when the world is a scary place, the U.S. dollar is one of the beneficiaries, since it has the heft of the U.S. government behind it.

So. A reason for everything. But have diversified portfolios still delivered, given the inflation fears? I’d argue yes. Global stocks are currently down, but to varying degrees; the U.S. dollar has supported those in U.S. financial markets; and while U.S. Treasuries have disappointed, they haven’t collapsed a la 2022 (we’ve got those higher yields to thank, along with the notion that, for now at least, we are contending with inflation fear and not inflation reality).

Making lemonade: The potential opportunities

Having come of age as an investor during the Global Financial Crisis and managing money through all sorts of exciting times since then, including sovereign debt crises, COVID, and the rip-roaring inflation in the post-pandemic era, I’ve found some of the best opportunities have emerged when fear is climbing and markets are falling.

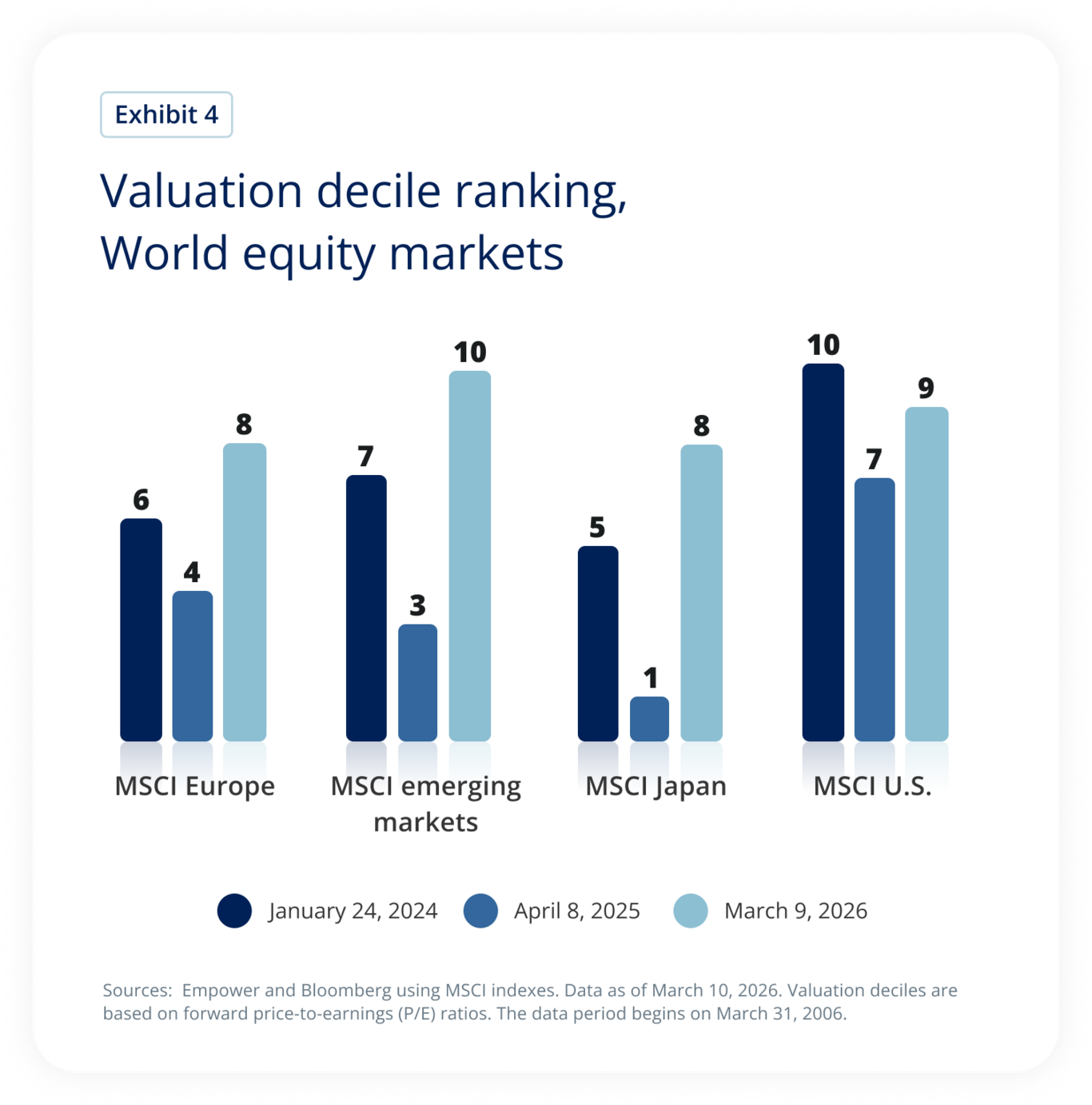

What I look for: Not just price movement, but valuation movement. In other words, keep an eye not just on the numerator (the price) but the denominator too (the earnings or whatever other fundamental factor is in play).

Take global equities. We’ve seen a sudden sell-off around the world, but in the lens of our analysis, most regions still look expensive, with Europe and Japan only now beginning to come off their higher valuations.

A buying opportunity? I’m not quite sure just yet. But potentially there’s room to rebalance into those markets as a starting point.

Should the sell-off continue and valuations grow more appealing, next steps would include fundamental research and, if still interested, likely a dollar-cost-averaging approach. This helps spread out the risk, offering the choice to add additional exposure at lower prices if the market continues to drop. And of course, all buying would occur within the confines of a broader portfolio so an investor doesn’t suddenly find themself with an absurd amount of exposure to particular opportunities.

Parting thoughts

Geopolitical headlines are among the scariest and almost beg investors to act; to make emotional changes to portfolios based on terrifying developments. But financial wisdom tells us it’s not moments like the current one that should dictate our portfolios, but rather a more sober look at financial goals and the portfolios designed to help get you there. Yes, we can take advantage of opportunities, but we don’t need to tear up our investment strategy and start anew on a day-by-day basis.

Steady as she goes.

Our mission is to empower financial freedom for all Empower is a customer-obsessed financial services company delivering investment, wealth management, and retirement services to more than 19M people.4 The following tenets guide the development and management of products and solutions we provide to the investors we serve: Commit to an unwavering duty of care Our investors are our priority. We steward every dollar we invest with care, attention, and respect. Emphasize fundamental analysis We keep our eyes on the horizon by rooting our analysis in the underlying drivers of long-term investment returns, not fleeting news and noise. Plan for better outcomes through thoughtful diversification We build resilient portfolios by relying on thoughtful diversification that plans for a range of outcomes, rather than a narrow result. |

Explore previous editions

February 2026 | December 2025 I October 2025 I September 2025

Stay up to date |

1 trade.gov/selectusa-energy-industry?anchor=content-node-t14-field-lp-region-1-1, trade.gov/selectusa-energy-industry?anchor=content-node-t14-field-lp-region-1-1, 2024.

2 Bloomberg data as of March 12, 2026.

3 trade.gov/selectusa-energy-industry?anchor=content-node-t14-field-lp-region-1-1, 2024.

4 As of September 30, 2025.

Diversification and asset allocation do not ensure a profit or protect against loss in declining markets.

Rebalancing and dollar-cost averaging do not ensure a profit and do not protect against loss in declining markets. Dollar-cost averaging requires continuous investment regardless of fluctuating price levels and may result in purchasing securities at higher prices.

International investing involves additional risks, including currency fluctuations and geopolitical risk.

Fixed income securities are subject to interest rate risk and inflation risk.

Investments, including gold, may be more volatile than traditional equity or fixed income investments.

“Bloomberg®” and the indices referenced herein (the “Indices,” and each such index – an “Index”) are trademarks or service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Index (collectively, “Bloomberg”), and/or one or more third-party providers (each such provider, a “Third-Party Provider”) and have been licensed for use for certain purposes to EMPOWER RETIREMENT, LLC (the “Licensee”). To the extent a Third-Party Provider contributes intellectual property in connection with the Index, such third-party products, company names, and logos are trademarks or service marks, and remain the property, of such Third-Party Provider. Bloomberg is not affiliated with the Licensee or a Third-Party Provider, and Bloomberg does not approve, endorse, review, or recommend the financial products referenced herein (the “Financial Products”). Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Indices or the Financial Products.

Investing involves risk, including possible loss of principal. This material is neither an endorsement of any security, index, or sector, nor a solicitation to offer investment advice or sell products or services.

The opinions expressed in this communication represent the current, good-faith views of Empower at the time of publication and are provided for limited purposes, are not intended as investment or legal advice, and should not be relied on as such. This content is based on the information available at the time of the recording and may change based on more current conditions.

Past performance, where discussed, is not a guarantee of future results. Investing involves risk. This is neither an endorsement of any index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index.

The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information. Predictions, opinions, and other information contained in this communication are subject to change and without notice of any kind and may no longer be true after the date indicated.

Commentary may contain forward-looking statements based on reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict.

The S&P 500® Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Empower Retirement, LLC. ©2026 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, SPFS, Dow Jones, their affiliates nor their licensors (“S&P DJI”) make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and S&P DJI shall have no liability for any errors, omissions, or interruptions of any index or the data included therein.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

©2026 Empower Annuity Insurance Company of America. All rights reserved.

INV-FBK-WF-5944153-0326 RO5295412-0326