Between the margins April 2026

April 2026

Risks, uncertainty, and your portfolio

April 2026

Risks, uncertainty, and your portfolio

Executive summary

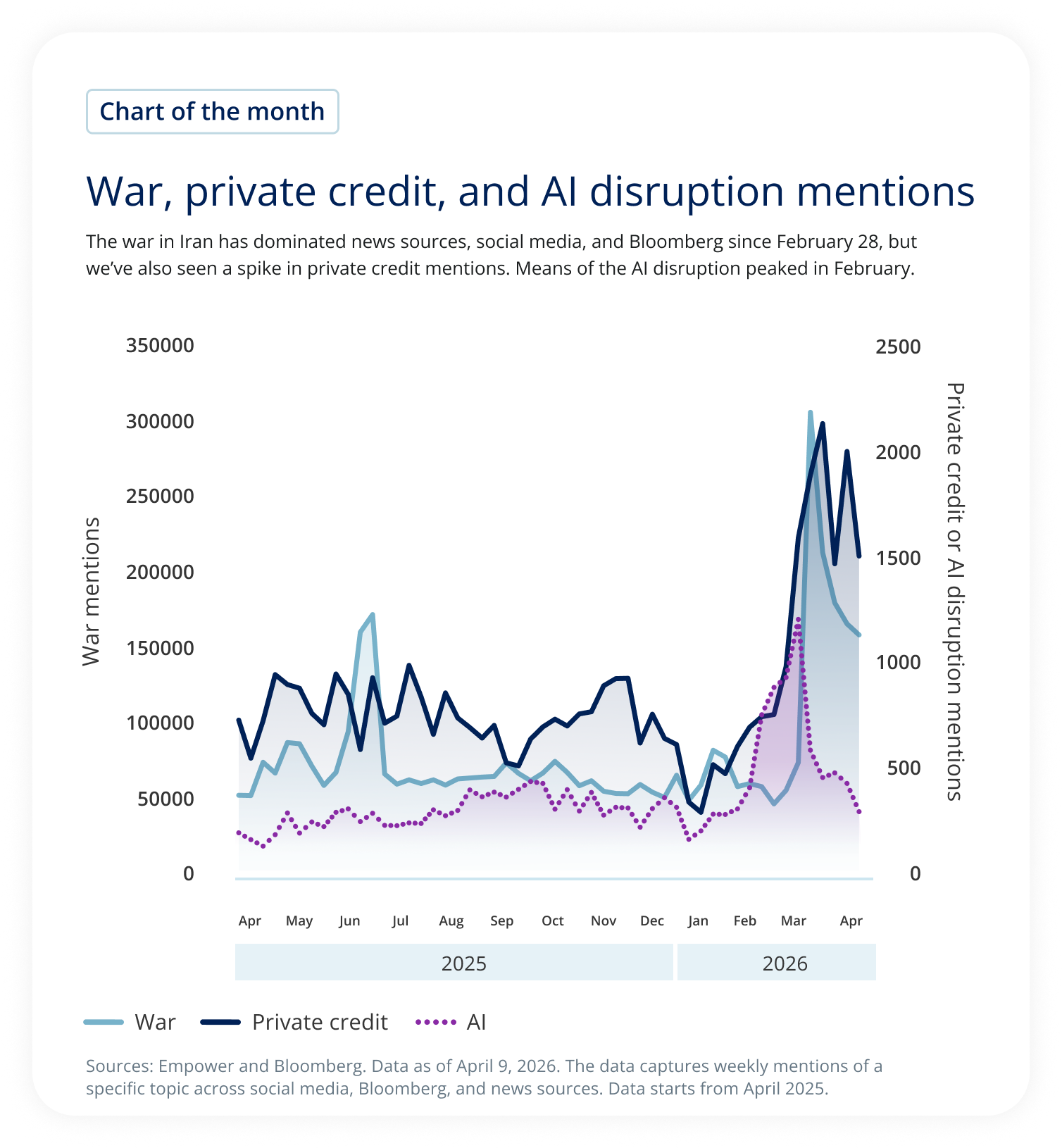

- Current headlines ping pong between concerns about the war in Iran, the vulnerability of private credit, and where artificial intelligence (AI) disruption will hit next.

- Can we handicap the range of outcomes? Probably not; we’ve got a “three-body problem” on our hands.

- So what to do? First, a reminder: I’d argue we entered this period in good shape.

- And there are offsets: For example, this isn’t our parents’ oil price shock.

- Still, with uncertainties like the ones we face today, I believe it’s good to put valuation and diversification on your side.

Risks are on the rise. That’s at least the way it feels as headlines ping pong across the Iran war, private credit concerns, and AI disruption.

The data captures weekly mentions of a specific topic across social media, Bloomberg, and news sources. Data starts from April 2025.

Here’s the uneasiness for many investors: How threatening are these risks to the U.S. economy?

If only we could say with certainty.

The reality is that each of these risks comes with unknowns on magnitude, duration, and significance.

As I write this commentary, a tenuous U.S.-Israel-Iran ceasefire has taken hold. But none of us know whether that ceasefire will continue and, if it does, what the negotiation terms will actually be. Thus, while the Iranian people may have welcome relief at the moment, the economic effects for the U.S. and the rest of the world may linger.

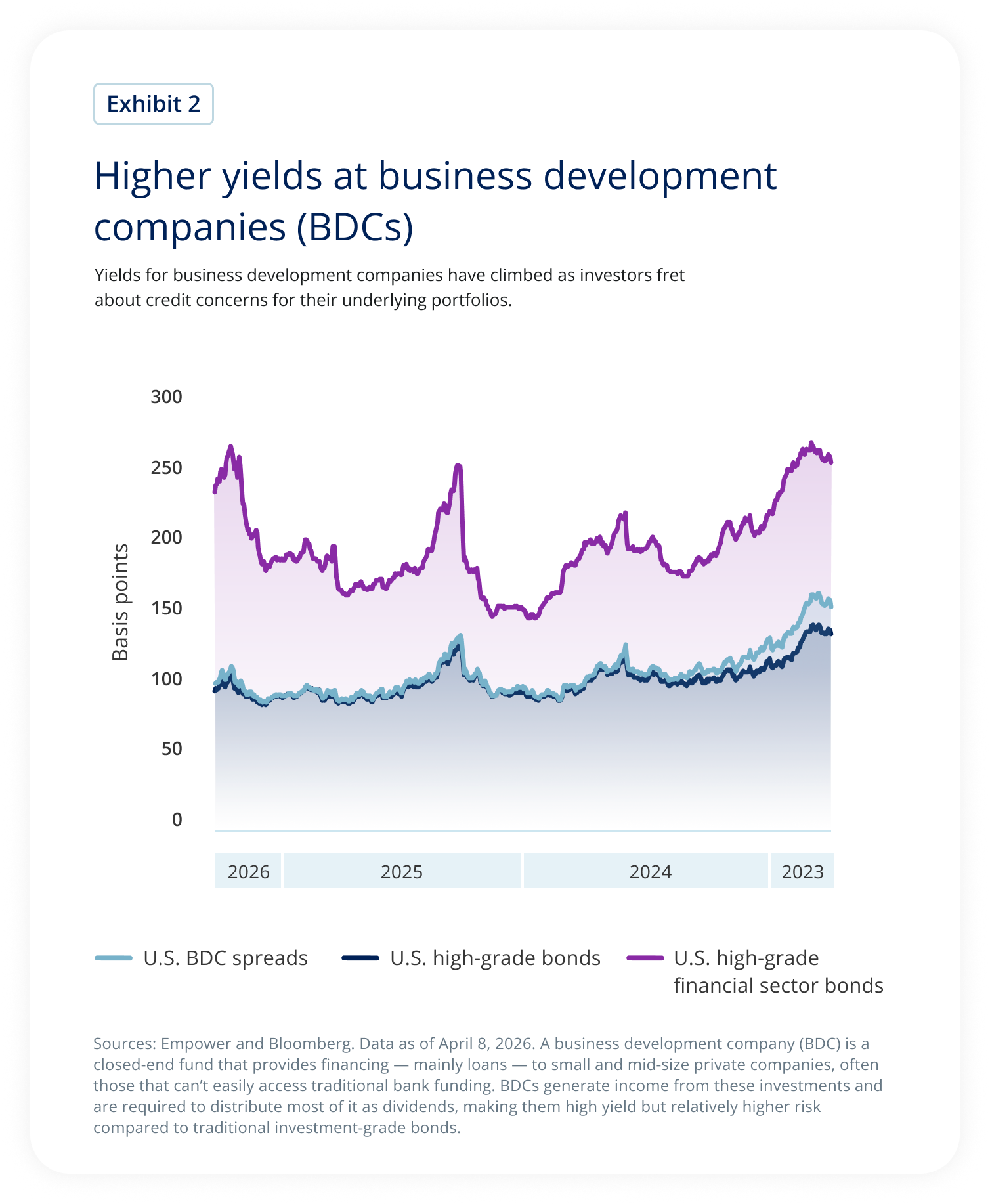

The scale of the true problems within private credit also is difficult to handicap. We know private credit has seen rapid growth over the past 10 years, particularly from weaker borrowers that turned to non-bank lending in the wake of the Global Financial Crisis. We also know private credit has exposure to the beleaguered software industry — and some of the end investors may not have the temperament or wherewithal for the long-time horizon required for private investing. What we don’t know for this opaque, data-light asset class: Are those concerns on the margin or in the main?

A Business Development Company (BDC) is a closed-end fund that provides financing—mainly loans—to small and mid-sized private companies, often those that cannot easily access traditional bank funding. BDCs generate income from these investments and are required to distribute most of it as dividends, making them high-yield but relatively higher-risk compared to traditional investment-grade bonds.

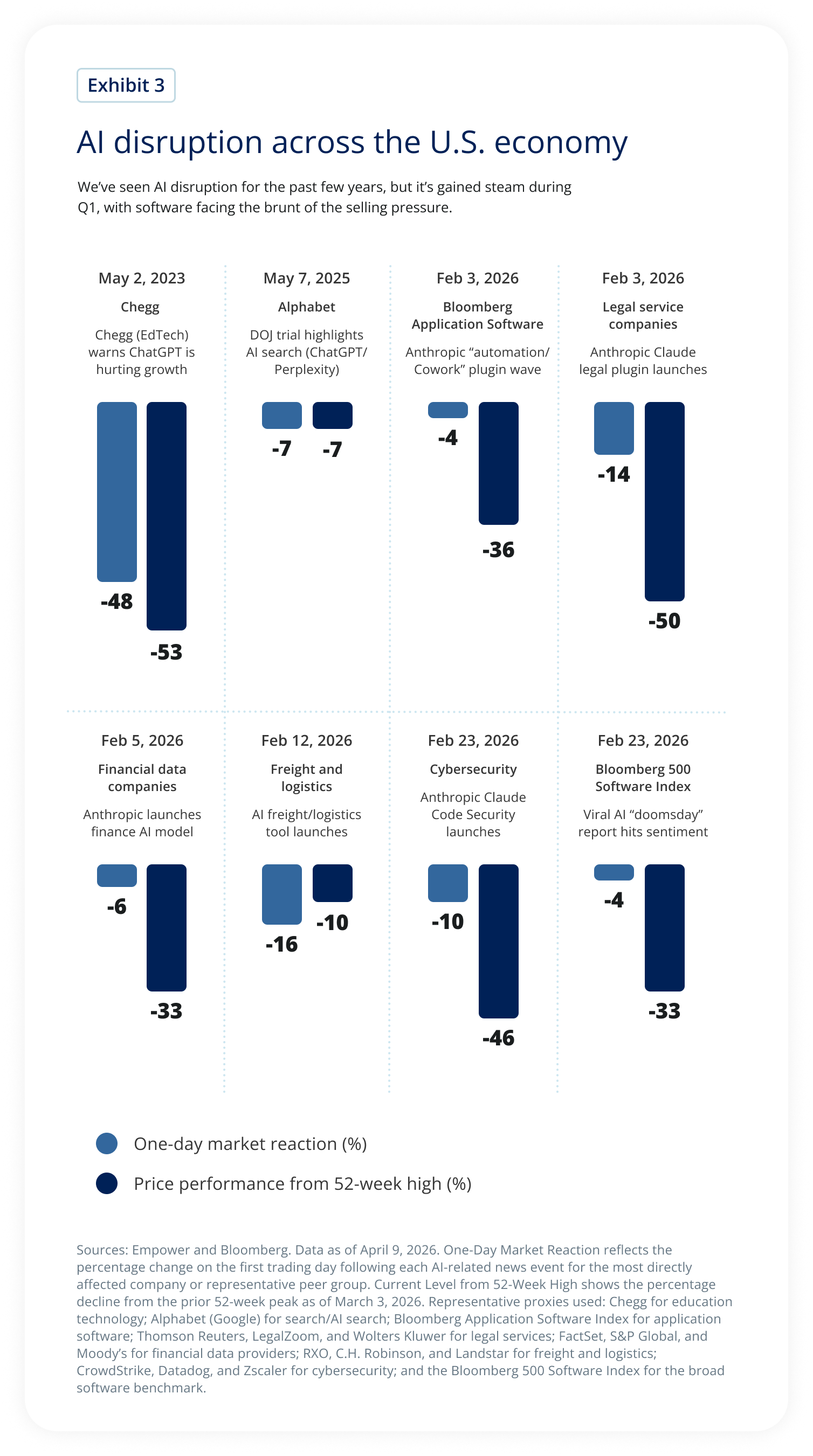

Finally, on AI disruption: Model companies have entered the early stages of monetization, dropping enterprise plug-ins aimed at streamlining workflows in legal work, wealth management, and logistics. With each new announcement, another legacy industry shudders. Not only do investors wonder whether incumbents will collapse, survive, or thrive in an AI world; they also worry about which industry will come into the crosshairs next.

One-Day Market Reaction reflects the percentage change on the first trading day following each AI-related news event for the most directly affected company or representative peer group. Current Level from 52-Week High shows the percentage decline from the prior 52-week peak as of March 3, 2026. Representative proxies used: Chegg for education technology; Alphabet (Google) for search/AI search; Bloomberg Application Software Index for application software; Thomson Reuters, LegalZoom, and Wolters Kluwer for legal services; FactSet, S&P Global, and Moody’s for financial data providers; RXO, C.H. Robinson, and Landstar for freight and logistics; CrowdStrike, Datadog, and Zscaler for cybersecurity; and the Bloomberg 500 Software Index for the broad software benchmark.

With prevailing conditions clouded by uncertainty, my impulse is to turn to scenario analysis, often rooted in historical corollaries, to zoom in on the range of outcomes. But if we’re truly spanning all of these risks, from the Iran war to private credit to AI disruption, what historical corollary exists? Do we experiment with a mix of the 1970s plus a “lite” version of the Global Financial Crisis, with a touch of the late 1990s mixed in? No, thanks. That’s a three-body problem (which my colleague Tom Nun tells me also is a good book for the sci-fi fans out there).

Here’s what I do know: Entering this period, the U.S. economy appeared remarkably resilient.

Our recent affordability study suggested that, despite the roller coaster of the post-pandemic years, the U.S. consumer — across all income levels — is modestly better off now than back in 2015, with income growth exceeding spending growth. Relatedly, we’ve seen the wealth effect in full effect, bolstering spending with strong market gains — and, more importantly in our estimation, housing gains. With our research suggesting high home prices are likely to remain rangebound over the course of 2026, we don’t expect that pillar to crumble despite the other pressures on the U.S. economy.

Source: Empower and Bureau of Labor Statistics Consumer Expenditure Survey. Data as of 12/19/2025. Essentials are defined as food, housing, transportation, apparel, and healthcare.

Meanwhile, though the fog of war clouds the long-term impact on commodities, we can take some reassurance that this isn’t our parent’s oil shock. Unlike in the 1970s, the U.S. is now the world’s largest oil and gas producer, which provides price protection for the U.S. gas market and shortage protection for U.S. businesses and consumers across the board. Moreover, energy dependency has declined over the years, and fuel prices were below the three- and five-year averages before the war (though they have since shot higher).

Gasoline prices: April 7, pre-war, and historical averages2

Pre war: $3.52

April 7: $4.88

3Y average: $3.77

5Y average: $3.88

10Y average: $3.31

Can I offer any similar reassurances on private credit? The opacity here is real, with time lags surrounding any aggregated read of default rates. Recent data from Cliffwater shows non-accrual rates (the percentage of loans relative to fair value or cost that have stopped paying interest or principal) remain below the 10-year average.1 And I’m not throwing in the towel on software names, some of which I think will adapt and thrive in the AI world order.

In regard to AI disruption, I can’t deny that I think there is more to come, particularly for complacent high-margin businesses. But is this something that could take down the U.S. economy? In fact, I think it’s far more likely to create a boom than a bust at the aggregate level, though particular industries, or, better said, particular businesses, could face more existential questions.

The base case

It appears I have a base case after all: Resilience. That’s not to say I’m not uneasy. Threats abound, and those with more pessimistic views can paint compelling pictures that bear a striking resemblance to recession. This is why earnings season will loom as large as ever over the next few weeks, with guidance again playing an outsized role amid uncertainty.

But even as I nervously say resilience, as an investor I think a valuable approach in this environment comes back to margins of safety (cheap valuations) and diversification across risk factors.

It’s for that reason that I celebrate the better valuations among technology — in fact, the Mag 7 is in the second lowest decile of its own history, dating back to 2015 — and emerging markets, which have dropped to the sixth decile. (Of course, in this environment not all emerging markets are created equal; consider the split between importers and exporters.)

Start dates for the indices are as follows: MSCI begins on April 28, 2006; B500 begins on March 31, 2003; and Mag 7 begins on July 31, 2015.

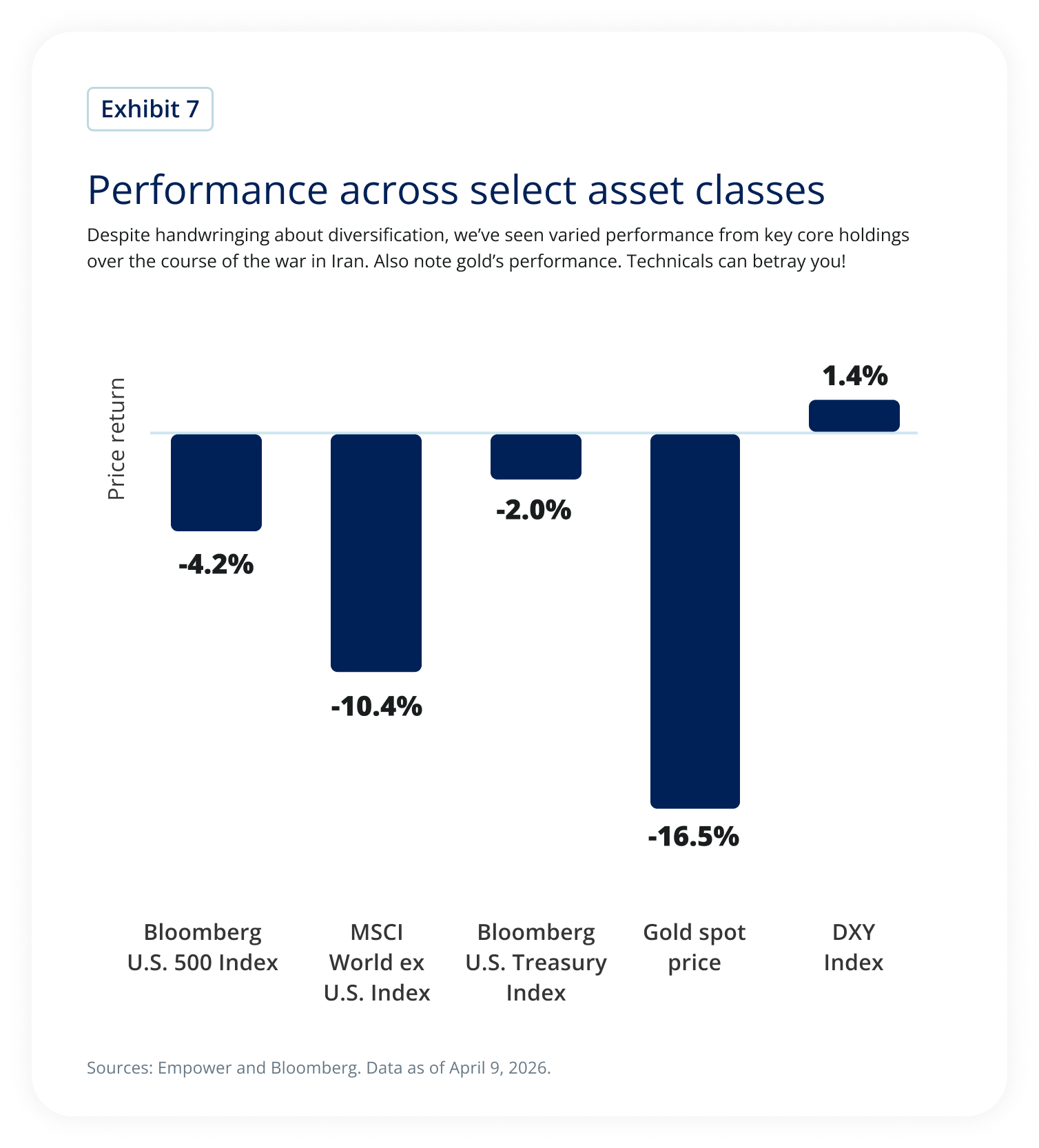

As for diversification: Investors have bemoaned the Treasury market weakness of late, but I’d argue nothing is broken there. Given inflation concerns, Treasuries have edged lower but could easily surprise to the upside if inflation concerns subside and growth concerns take hold. Meanwhile, we’ve seen strength from the U.S. dollar, but U.S. equities have proven less vulnerable than their global counterparts.

In other words, spreading portfolios across an assortment of global asset classes has done its job amid uncertainty. As uncertainty persists, such diversification remains a favorite risk-management tool of mine.

Our mission is to empower financial freedom for all Empower is a customer-obsessed financial services company delivering investment, wealth management, and retirement services to more than 19M people.3 The following tenets guide the development and management of products and solutions we provide to the investors we serve: Commit to an unwavering duty of care Our investors are our priority. We steward every dollar we invest with care, attention, and respect. Emphasize fundamental analysis We keep our eyes on the horizon by rooting our analysis in the underlying drivers of long-term investment returns, not fleeting news and noise. Plan for better outcomes through thoughtful diversification We build resilient portfolios by relying on thoughtful diversification that plans for a range of outcomes, rather than a narrow result. |

Explore previous editions

March 2026 | February 2026 | December 2025 I October 2025 I September 2025

Stay up to date |

1 As of September 30, 2025.

“Bloomberg®” and the indices referenced herein (the “Indices,” and each such index – an “Index”) are trademarks or service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Index (collectively, “Bloomberg”), and/or one or more third-party providers (each such provider, a “Third-Party Provider”) and have been licensed for use for certain purposes to EMPOWER RETIREMENT, LLC (the “Licensee”). To the extent a Third-Party Provider contributes intellectual property in connection with the Index, such third-party products, company names, and logos are trademarks or service marks, and remain the property, of such Third-Party Provider. Bloomberg is not affiliated with the Licensee or a Third-Party Provider, and Bloomberg does not approve, endorse, review, or recommend the financial products referenced herein (the “Financial Products”). Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Indices or the Financial Products.

Investing involves risk, including possible loss of principal. This material is neither an endorsement of any security, index, or sector, nor a solicitation to offer investment advice or sell products or services.

The opinions expressed in this communication represent the current, good-faith views of Empower at the time of publication and are provided for limited purposes, are not intended as investment or legal advice, and should not be relied on as such. This content is based on the information available at the time of the recording and may change based on more current conditions.

Past performance, where discussed, is not a guarantee of future results. Investing involves risk. This is neither an endorsement of any index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index.

The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information. Predictions, opinions, and other information contained in this communication are subject to change and without notice of any kind and may no longer be true after the date indicated.

Commentary may contain forward-looking statements based on reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict.

The S&P 500® Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Empower Retirement, LLC. ©2026 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, SPFS, Dow Jones, their affiliates nor their licensors (“S&P DJI”) make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and S&P DJI shall have no liability for any errors, omissions, or interruptions of any index or the data included therein.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. INV-FLY-WF-5764450-0226 RO5206223-0226