Between the margins February 2026: AI and the software scare

February 2026

AI and the software scare

February 2026

AI and the software scare

Executive summary

- With the software sell-off, the AI revolution finally feels real.

- Some of the selling may be warranted, but it's widescale enough to wonder if bargains could emerge.

- And while software may be the first, it likely won't be the last (as wealth managers have learned this week).

- Things to consider? Avoid the expensive stuff, consider opportunity alongside risk, and look at a portfolio approach a portfolio approach.

On February 3, the AI shoe dropped.

Anthropic released an innocuous press release, sharing that its AI platform was open for legal work. To software stocks, that was the shot heard round the world. Already under pressure, the Bloomberg Software and Tech Services Index dropped 4% in a day.

Take a look at the freefall below in our Chart of the Month.

Why such drama? Because it made the AI revolution real.

Recall that Alphabet CEO Sundar Pichai called AI more transformative than electricity or fire back in 2018. But until now, all that AI has really transformed is Big Tech, turning asset-light businesses into capital-intensive businesses that create insatiable models on the backs of pricey semiconductor chips and pour concrete for what feels like city-sized data centers.

Then comes the first week of February. With Anthropic offering a plugin called Legal, which would allow Claude Cowork, its AI platform, to assist with tasks like contract reviews and legal briefs, the status quo appears on the precipice of real transformation.

Of course, this has implications for businesses that service the legal field — we saw Thomson Reuters take a beating last week — but also for software companies. Investors could reason that if AI platforms like Claude can embed themselves in the legal field, model plug-ins can similarly replace third-party software vendors.

So here’s the question for investors. Is that true? Is software suddenly in trouble?

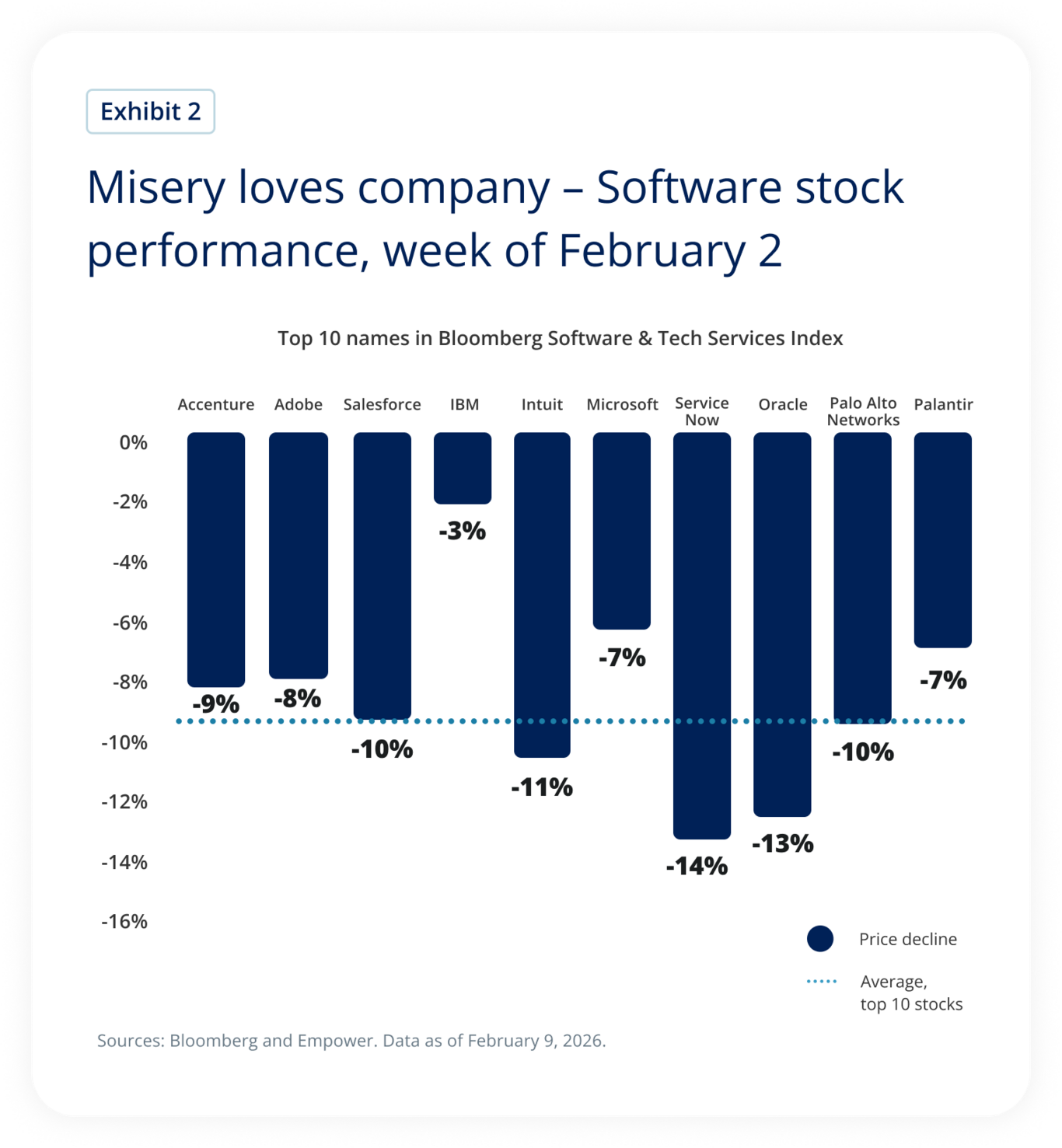

The immediate reaction suggested as much. Despite different business models and applications, the top 10 names of Bloomberg’s Software and Tech Services Index dropped in unison the week of February 2, down an average 9%.

Nvidia CEO Jensen Huang scoffed at this reaction. “Would you use a screwdriver or invent a new screwdriver?”

I guess that comes down to cost, right?

If a plugin comes at the right price and can easily replace a more expensive application, or if an AI agent model requires fewer “seats” (software speak for licenses), then maybe a switch from a software vendor to an AI platform could make sense.

But what if the software is more infrastructure than application? Don’t forget, Microsoft sits in the software industry. And, yes, it has applications, but it also has its own AI models and a cloud business that supports — you guessed it — AI. Is its business model ruined now, too, by an AI plugin?

That’s hard to believe.

Here’s how I’m thinking about software stocks these days. We’re indeed in an era of transformation, and applications that skate across the surface likely have far less value in this new world order.

But software that acts more like infrastructure tends to be less vulnerable. Maybe there is a re-rating that reflects greater competition or new pricing models. But I think it could be well worth sorting through the industry to look for those that may, in the end, prove winners, or at least survivors, in the great AI race. After all, valuations today no longer reflect Marc Andreeson’s 2011 Wall Street Journal editorial, “Why Software is Eating the World.” And now, after the sell-off, some stocks may in fact be a bit too cheap than is warranted for their particular business models.

The big picture and the path forward

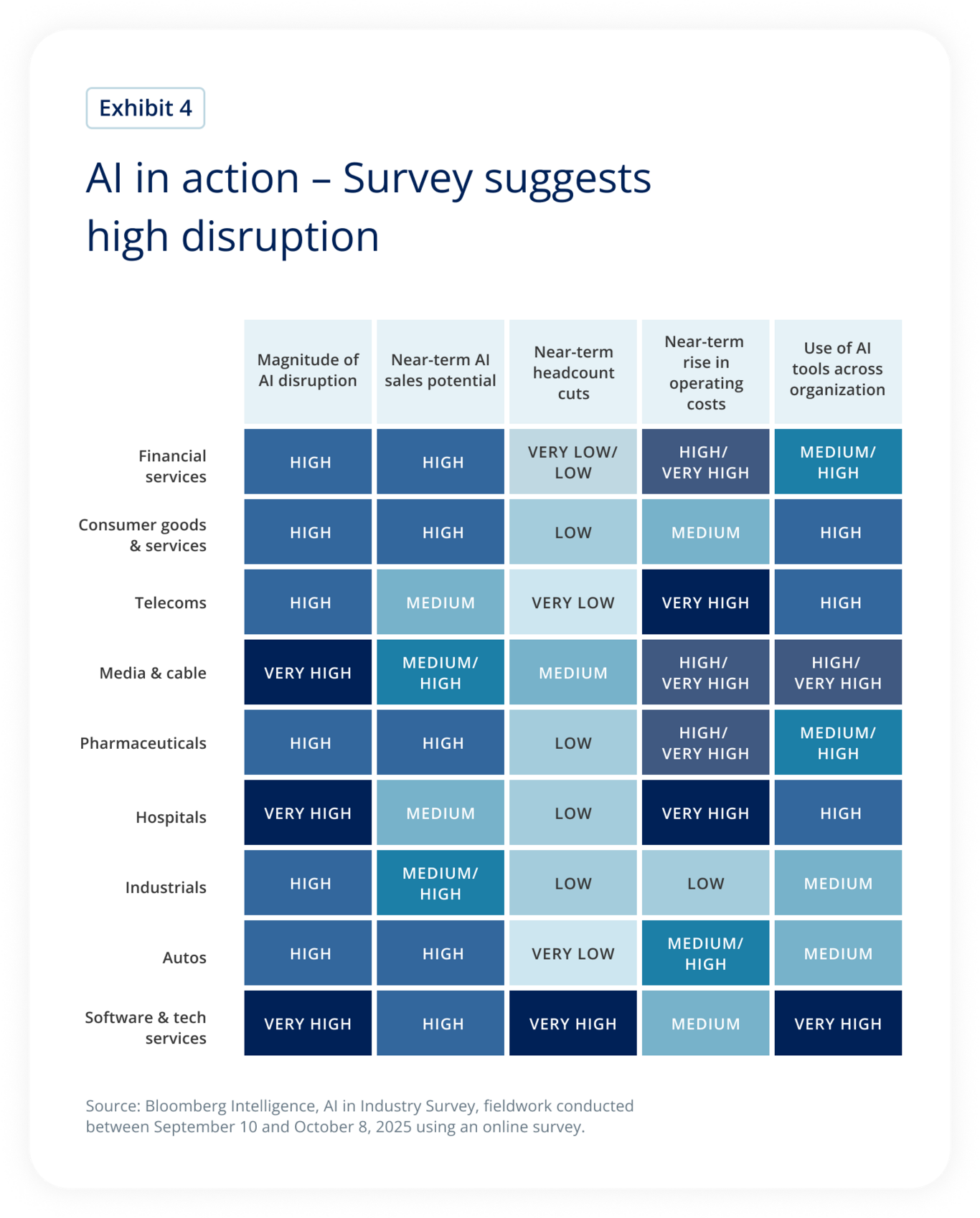

Software’s collapse is likely just the beginning. Other industries are equally vulnerable to AI disruption. Consider this week's bloodbath in wealth management. Or accounting firms. Or content creation. Or really anything.

According to a recent survey by Bloomberg, industries across the economy are vulnerable to some level of disruption sooner or later.

So how can investors help guard against this?

A few rules of thumb I think are worth keeping in mind:

1. Avoid the really expensive stuff.

Few can predict the future with any sort of specificity, particularly as we peer around bends, like the current AI hairpin.

But we can spot some vulnerabilities. One of the biggest vulnerabilities in markets is likely complacency around established businesses. And that describes software to a T.

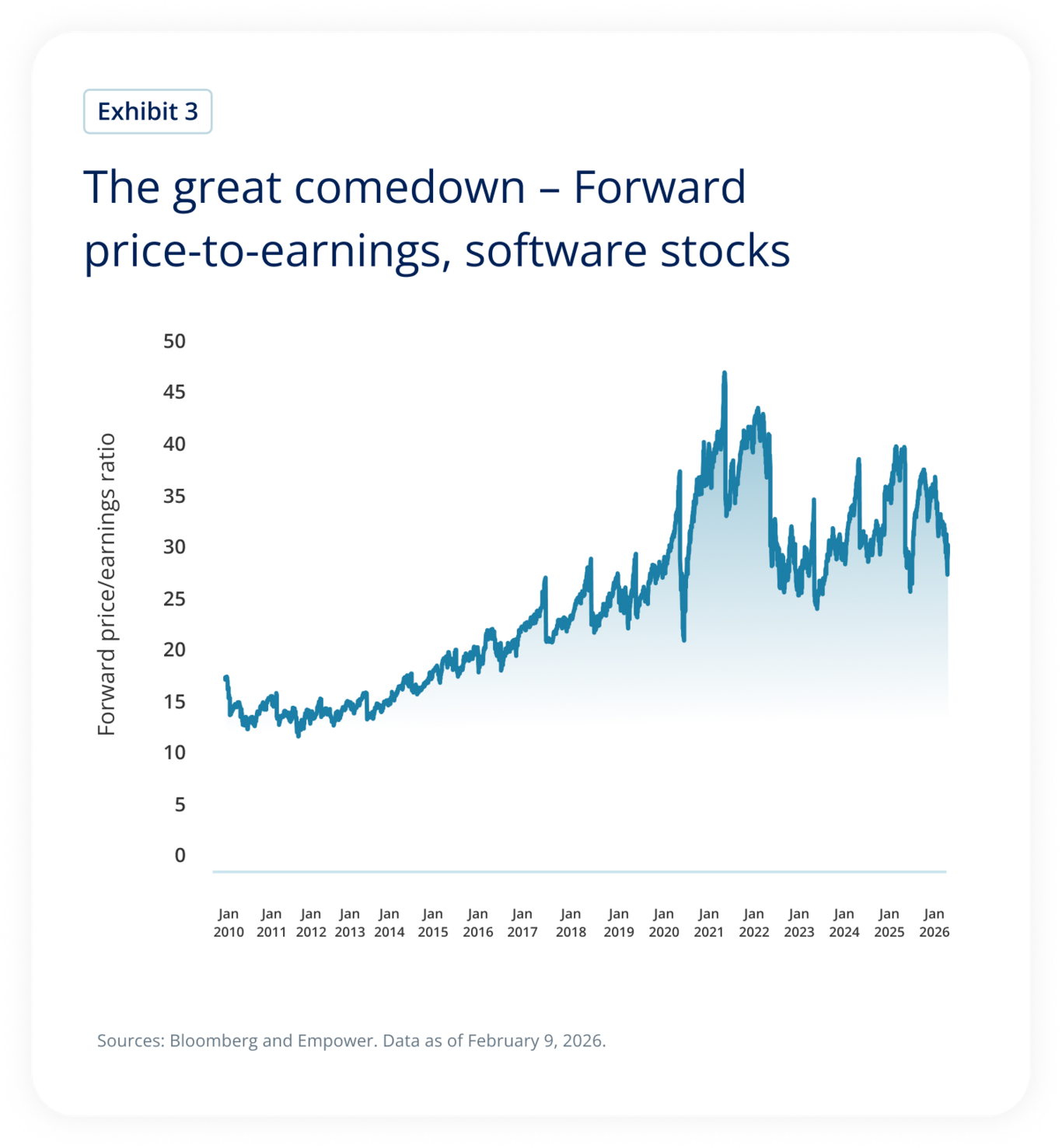

We see it most clearly in its valuations over the past 10 years. Due to its ubiquity, the software industry has seen ever-expanding valuations. Since the start of 2016, investors have given software’s forward price-to-earnings ratio an average nine percentage points premium relative to the broader market (as measured by the Bloomberg 500 Index).

Now, as disruption explodes and sentiment collapses, the stocks don’t trip over their feet, they crash from the sky. And therein lies the risk of extreme valuations: They just have further to fall when things go wrong. Because very few think anything can go wrong.

It’s for this reason we don’t just eyeball valuation metrics, we also look at long-term histories and evaluate sectors by their valuation decile. This helps us identify extremes and give a side eye to sectors that sit in the 9th or 10th deciles of their own history. (And in fact, at the start of 2026, software sat in the 10th decile of its price/forward earnings history. As of February 7, it had slipped to the 8th decile.)

2. Consider the potential opportunity, not just the risk.

So avoid the pricey stuff, huh? That’s a tall order when nearly the entire U.S. equity market looks expensive. Indeed, from the perspective of our decile ranking, nine of 10 sectors (we don’t run this analysis on real estate) sit in the 9th or 10th decile.

Two thoughts here.

First, recognize when excessive valuations are less excessive than they first appear. Consider healthcare. It looks pretty pricey in our deciles today — it sits in the 9th decile — but, unlike other sectors, it’s only recently broken away from years of middling valuations.

Moreover, this is where independent fundamental analysis comes into play. If we think a company can reverse its fortunes, it may still prove reasonably priced, even if its multiple sits above historical levels.

Second, when everything sports a high price tag, market collapses are especially valuable since they offer the potential for scarce valuation opportunities. Consider the market doubt that surrounds AI-Alist companies, which means some of these businesses now sport surprisingly attractive valuations despite their incredible earnings. And, of course, the topic du jour: Software companies selling off en masse could mean investors are tossing babies along with the bath water.

So rather than fleeing markets in freefall, something to consider: As I described for software companies in my comments earlier, it may very well pay to sort through collapsing markets for companies with resilient business models that now come with far lower valuations.

3. Take a portfolio approach.

As I describe looking for opportunity amid sell-offs, I also have to acknowledge how difficult it can be to identify the winners, or even the survivors.

The rationale is twofold. First, surviving a transition to an AI world is a bit of a call on management, making it at least partly subjective. Second, in our AI world, technology is shape shifting in real time, meaning an approach that seemed right a few years ago may now be obsolete.

Rather than trying to play kingmaker, I’m partial to a portfolio approach. Undoubtedly that will mean exposure to some companies that don’t make the transition well. But it could also help capture companies that surprise to the upside. And in an AI world, this applies both to the suppliers — the hyperscalers and the chipmakers, for example — and the deployers like software companies, biotech companies, or indeed the broader economy.

Take heart

The big developments over the coming month that I’m watching: Hiring/firing trends; the inflation trajectory; and Nvidia earnings, which is now a macro indicator. I’ll also keep an eye out for new affordability proposals, which have inched closer in recent weeks to impacting earnings.

But as we watch the world unfold, a bit of encouragement: For many, it seems as though no matter where we look — at markets, geopolitics, or technology — the tectonic plates are shifting. (Trust me: I feel it every Monday as I revise my Friday talking points after weekend developments. No rest for the weary!)

But these tectonic shifts don’t have to mean massive portfolio repositioning (unless, of course, you’re as excited as I am about the potential opportunities from market disruption). A well-diversified portfolio properly aimed at individual investment goals and rooted in long-term fundamentals could help an investor sleep easier at night, even as the windows rattle.

Until March. In the meantime, take heart.

Our mission is to empower financial freedom for all Empower is a customer-obsessed financial services company delivering investment, wealth management, and retirement services to more than 19M people.1 The following tenets guide the development and management of products and solutions we provide to the investors we serve: Commit to an unwavering duty of care Our investors are our priority. We steward every dollar we invest with care, attention, and respect. Emphasize fundamental analysis We keep our eyes on the horizon by rooting our analysis in the underlying drivers of long-term investment returns, not fleeting news and noise. Plan for better outcomes through thoughtful diversification We build resilient portfolios by relying on thoughtful diversification that plans for a range of outcomes, rather than a narrow result. |

Explore previous editions

Stay up to date |

1 As of September 30, 2025.

“Bloomberg®” and the indices referenced herein (the “Indices,” and each such index – an “Index”) are trademarks or service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Index (collectively, “Bloomberg”), and/or one or more third-party providers (each such provider, a “Third-Party Provider”) and have been licensed for use for certain purposes to EMPOWER RETIREMENT, LLC (the “Licensee”). To the extent a Third-Party Provider contributes intellectual property in connection with the Index, such third-party products, company names, and logos are trademarks or service marks, and remain the property, of such Third-Party Provider. Bloomberg is not affiliated with the Licensee or a Third-Party Provider, and Bloomberg does not approve, endorse, review, or recommend the financial products referenced herein (the “Financial Products”). Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Indices or the Financial Products.

Investing involves risk, including possible loss of principal. This material is neither an endorsement of any security, index, or sector, nor a solicitation to offer investment advice or sell products or services.

The opinions expressed in this communication represent the current, good-faith views of Empower at the time of publication and are provided for limited purposes, are not intended as investment or legal advice, and should not be relied on as such. This content is based on the information available at the time of the recording and may change based on more current conditions.

Past performance, where discussed, is not a guarantee of future results. Investing involves risk. This is neither an endorsement of any index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index.

The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information. Predictions, opinions, and other information contained in this communication are subject to change and without notice of any kind and may no longer be true after the date indicated.

Commentary may contain forward-looking statements based on reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict.

The S&P 500® Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Empower Retirement, LLC. ©2026 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit www.spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, SPFS, Dow Jones, their affiliates nor their licensors (“S&P DJI”) make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and S&P DJI shall have no liability for any errors, omissions, or interruptions of any index or the data included therein.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. INV-FLY-WF-5764450-0226 RO5206223-0226