The Currency

Be current.

Be current.

Get insights and intel on your money.

*If you’re already registered with Empower, please use the same email address as your existing account.

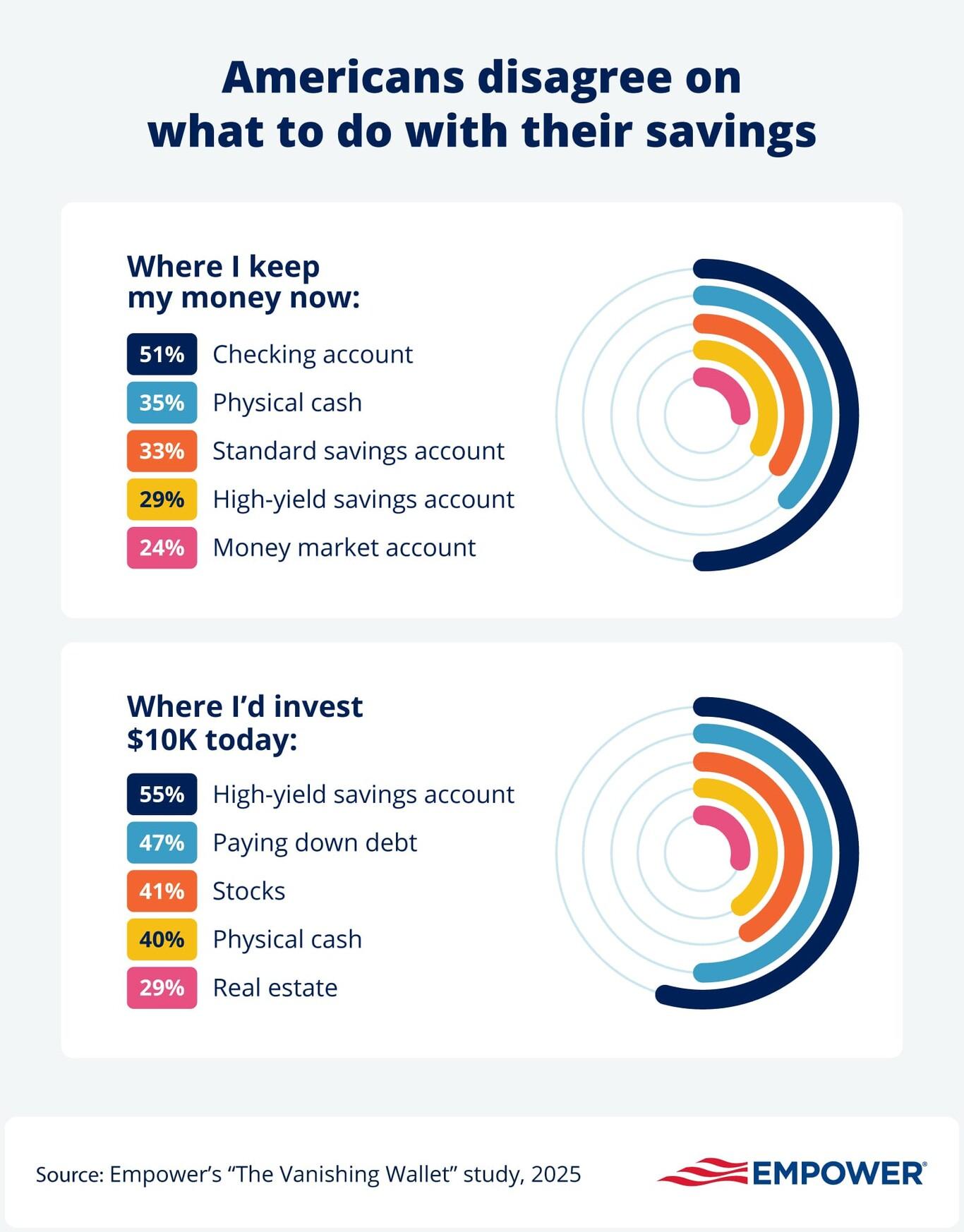

The average American holds between $51 and $100 cash in their “wallet,” according to Empower research. Here’s how people approach where to keep their liquid savings:

The average American holds between $51 and $100 cash in their “wallet,” according to Empower research. Here’s how people approach where to keep their liquid savings:

Explore by topic

Solo 401(k): Understanding self-employed retirement plans

Life

Theme Slug

category--life

Pathauto Slug

life

The solo 401(k) is popular among self-employed individuals thanks to its high contribution limits and tax advantages.

Beyond tax season: Why year-round tax planning can pay off

Money

Theme Slug

category--money

Pathauto Slug

money

Tax filing season is a few months. Tax outcomes are shaped by financial choices and life events that happen throughout the calendar year.

Valentine’s Day spending set to reach record $29.1B

Play

Theme Slug

category--play

Pathauto Slug

play

Valentine’s Day spending is growing at roughly twice the pace of overall U.S. retail sales, and is set to reach $29.1B in 2026.