Q3 outlook overview 2026

U.S. economic and market outlook 2026

Q3 outlook overview

U.S. economic and market outlook 2026

Q3 outlook overview

Economy

March 2026

We thought the ongoing artificial intelligence (AI) build would continue to propel the economy forward while the consumer remained resilient despite higher energy prices.

With the AI build still in the early stages and AI implementation just beginning to take shape, we expected both to accelerate over the quarter, supporting the broader economy regardless of any near-term headwinds. Meanwhile, we didn’t expect the consumer to fold under the pressure of higher energy prices, arguing that the dynamics at work in the current climate were different than historical corollaries.

Since then

We did indeed see AI continue to spur economic activity, with the consumer holding the line.

Massive spending around AI continued; hyperscalers even raised equity and floated debt to continue their investments. The sustained spending magnified the bottleneck in memory chips and fueled a speculative rally in the broader chip space. The first-quarter GDP print reinforced the impact of AI on the economy, with the growth in tech-related investment spending outstripping that of consumer spending.

Higher gas prices showed up in inflation prints, but the labor market showcased surprising strength, and consumers continued to spend (on more than just gasoline), buoyed at least in part by the housing gains of prior years and the stock market gains of today.

June 2026

We expect AI to roll on but have a more nuanced view on the U.S. consumer.

Both the AI build and implementation remain in their early stage. Moreover, as the AI race is a matter of existential risk and opportunity for U.S. mega tech, we don’t anticipate meaningful sensitivity to the macroeconomic factors that tend to weigh on the rest of the economy; inflation, for example, or the prospect of higher rates.

We think the story is more nuanced for consumers. We anticipate continued labor market durability but expect a certain measure of unevenness, with some industries increasing hiring due to the AI spend and others remaining stagnant.

Meanwhile, as we move away from tax refunds, we expect higher gas prices to hit a bit harder. Of course, with the Strait of Hormuz potentially reopening, we could get some relief from today’s levels, but we don’t anticipate an immediate return to the low pump prices we saw in the first quarter, particularly given the time it will take for oil wells to come back online. Other consumer pressures include the possibility of continued disappointment in real wage growth and an extended hold by the Federal Reserve, allowing little improvement in mortgage rates, among other consumer loans.

Even with those headwinds, though, we don’t expect the consumer to buckle. That’s not just because of our view of labor market resilience. It’s also because of the wealth effect: ongoing stock market gains combined with the housing gains of prior years.

Net-net, we view the consumer as resilient but not accelerating, as some suggest.

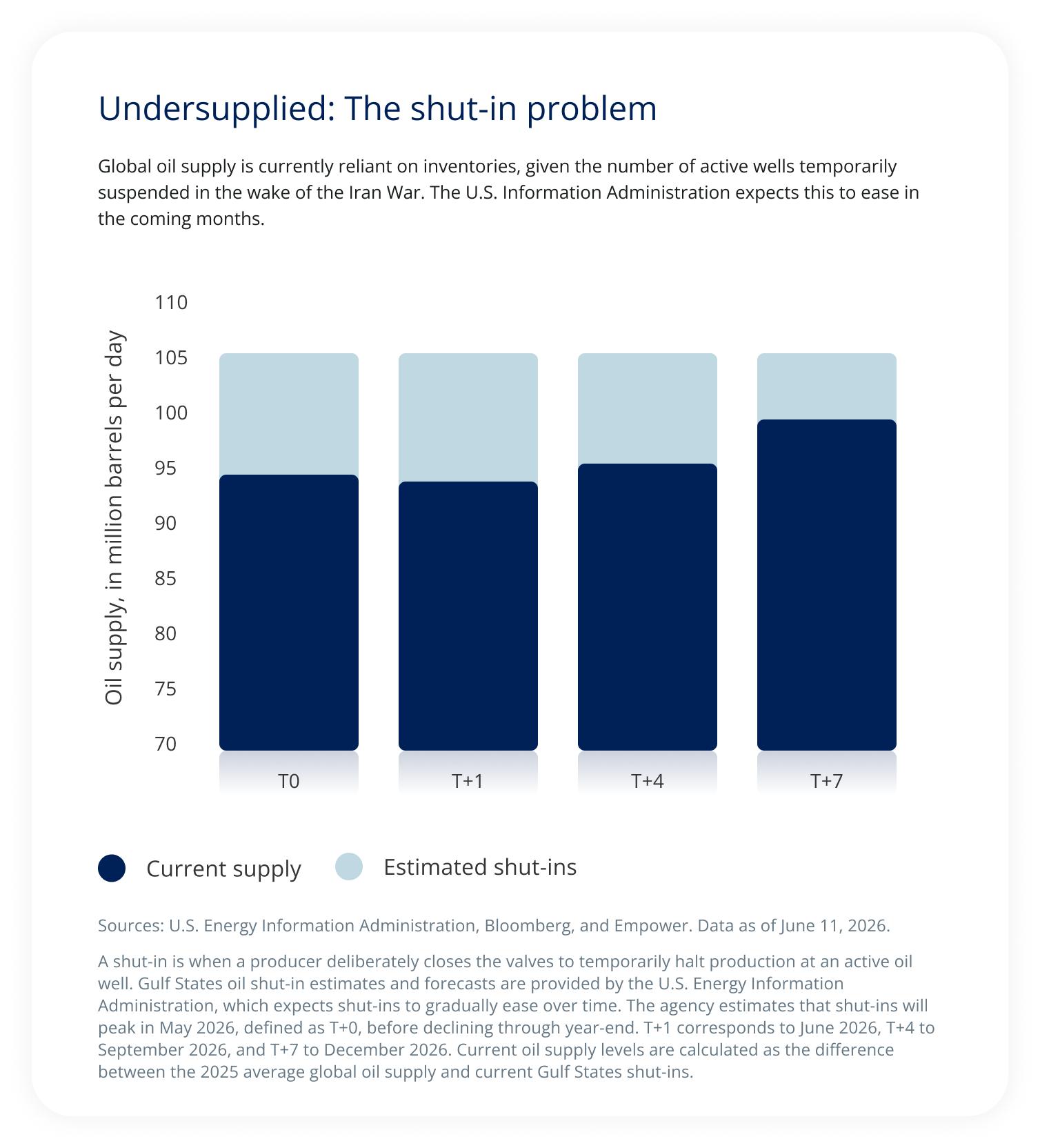

Global oil supply is currently reliant on inventories, given the number of active wells temporarily suspended in the wake of the Iran War. The U.S. Information Administration expects this to ease in the coming months.

Stocks

March 2026

We thought software and select names of the Magnificent Seven (Mag 7) were attractively priced. Otherwise, we were ambivalent about the U.S. stock market.

The first quarter saw little traction for the market’s biggest AI names, which, in light of their outstanding earnings, enhanced their valuations. We considered this an opportunity to add to the AI trade at reasonable prices.

We also thought software was fertile ground for the long-term investor; valuations across the industry had collapsed amid AI disruption fears, but the sell-off was indiscriminate, treating companies that could survive and thrive in an AI world as though they were broken businesses.

The rest of the market didn’t look overly compelling to us. We thought earnings would do well in a resilient economy but didn’t see much valuation opportunity.

Since then

It’s been a runaway market.

But not across the board. Semiconductor and memory chips have generated outstanding outperformance, though in early June they gave some of those returns back. The Mag 7 names as a group also outperformed until they hit a roadblack in June; their remarkable results were more about continued earnings momentum — they blew past analyst expectations — rather than price performance.

Software was a volatile group but no longer collapsing.

Other sectors delivered a solid Q1 earnings season but saw less progress in the stock market.

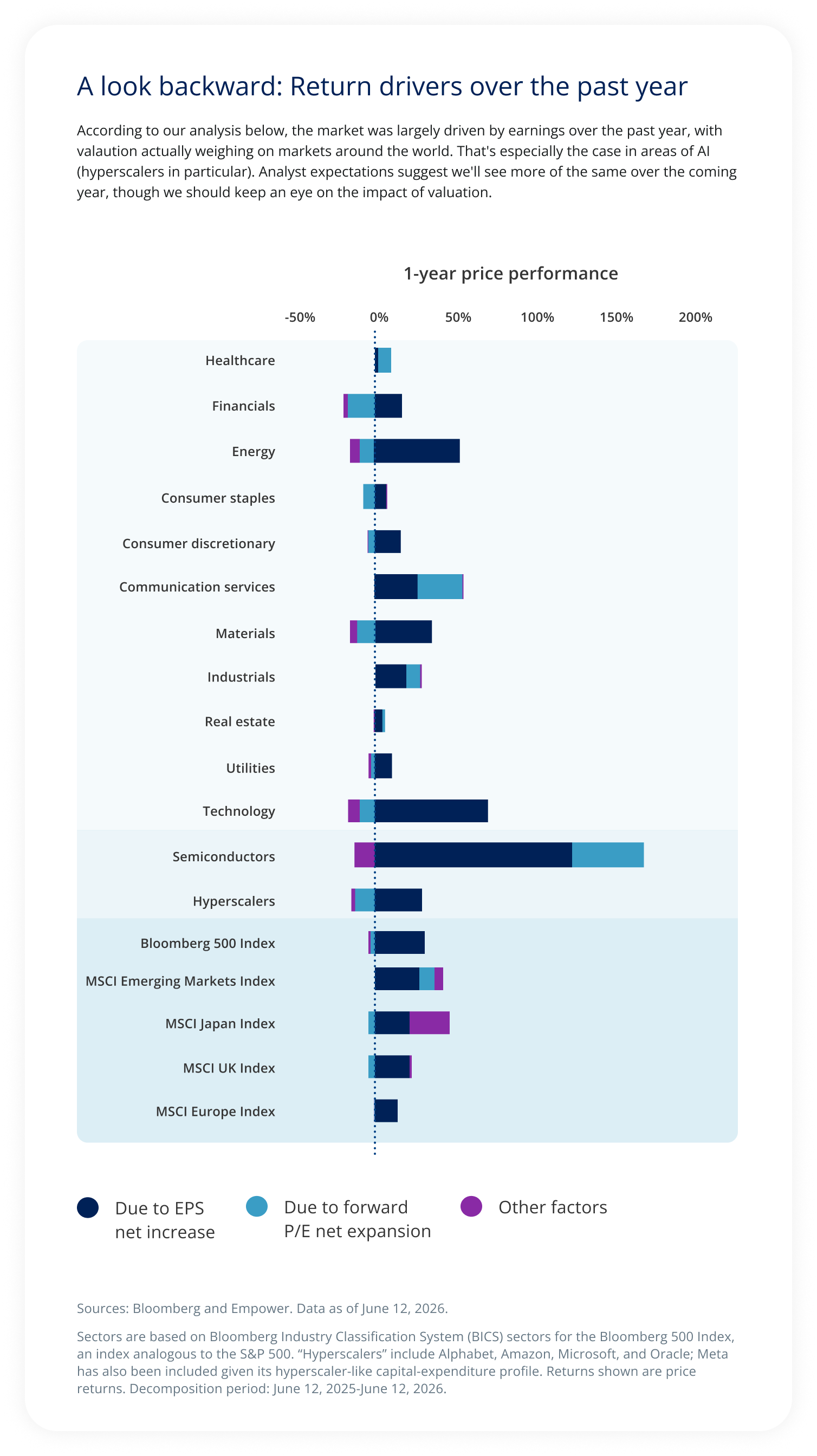

In fact, when we look at returns across the global equity market over not just the last quarter but the last year, we find many areas where earnings drove results.

According to our analysis below, the market was largely driven by earnings over the past year, with valaution actually weighing on markets around the world. That's especially the case in areas of AI (hyperscalers in particular). Analyst expectations suggest we'll see more of the same over the coming year, though we should keep an eye on the impact of valuation.

June 2026

We expect the AI trade to remain sensitive to big sentiment swings. But with the Q2 market rally concentrated in a narrow segment of the market, we don’t consider U.S. equities as a whole overly frothy today.

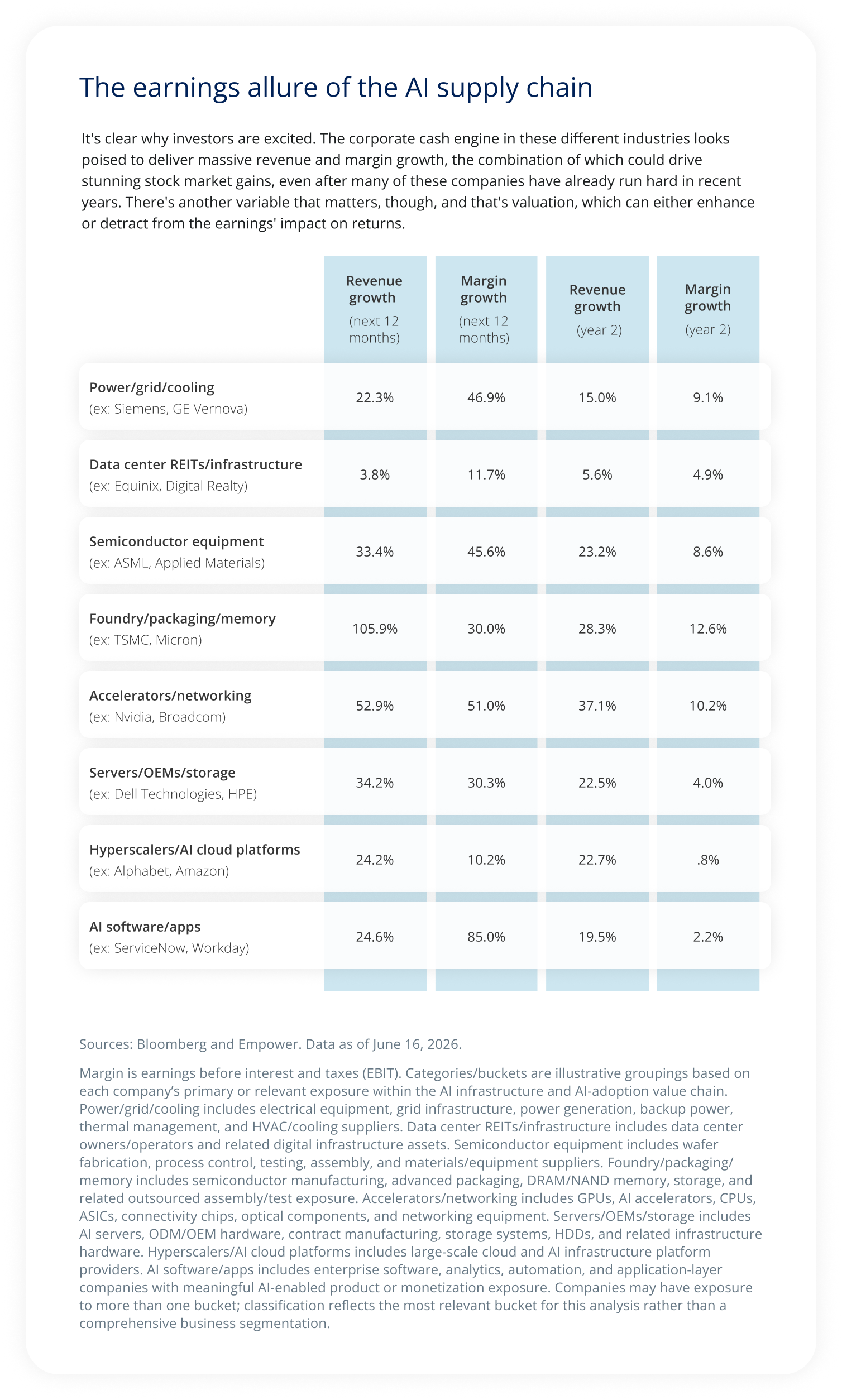

There’s no question the market centers around AI. Due to remarkable AI-fueled revenues and margins, investors expect big returns across the AI supply chain, given that earnings are a major contributor to equity performance, particularly over the long term.

It's clear why investors are excited. The corporate cash engine in these different industries looks poised to deliver massive revenue and margin growth, the combination of which could drive stunning stock market gains, even after many of these companies have already run hard in recent years. There's another variable that matters, though, and that's valuation, which can either enhance or detract from the earnings' impact on returns.

The trouble is quickly shifting sentiment, which could undercut valuations and evaporate at least some of those returns. This was an added source of return over the past year, as some of these markets rerated higher, but it could also cut the other way, evaporating at least some of the gains expected from earnings and income. We saw as much last quarter in the memory and semiconductor space. In fact, we think we could see continued volatility across both. Though they have sold off, their earlier rally was fierce enough that they still look a bit stretched to us.

Other areas of AI may not have the same vulnerability. That’s especially true for the mega-tech companies that sit at the epicenter of the AI trade but remain reasonably priced, particularly as their earnings strength continues.

With quieter performance and still-reasonable fundamentals, the broader U.S. equity market isn’t necessarily exciting, but it’s also not concerning. Valuations have come down since the start of the year in a handful of sectors. Among the defensive subset, we still consider consumer staples expensive but see some appeal to healthcare. It’s a bit cheaper and tends to hold up better in difficult market environments.

Even with underlying strength, we think investors should prepare for volatility. SpaceX is now public, with a series of lock-ups offering the potential for more float to hit the market. OpenAI and Anthropic aren’t far behind. The trio of cannonballs have the potential to cause not just big waves but ongoing ripples as indexes, passive strategies, and active investors adjust portfolios accordingly.

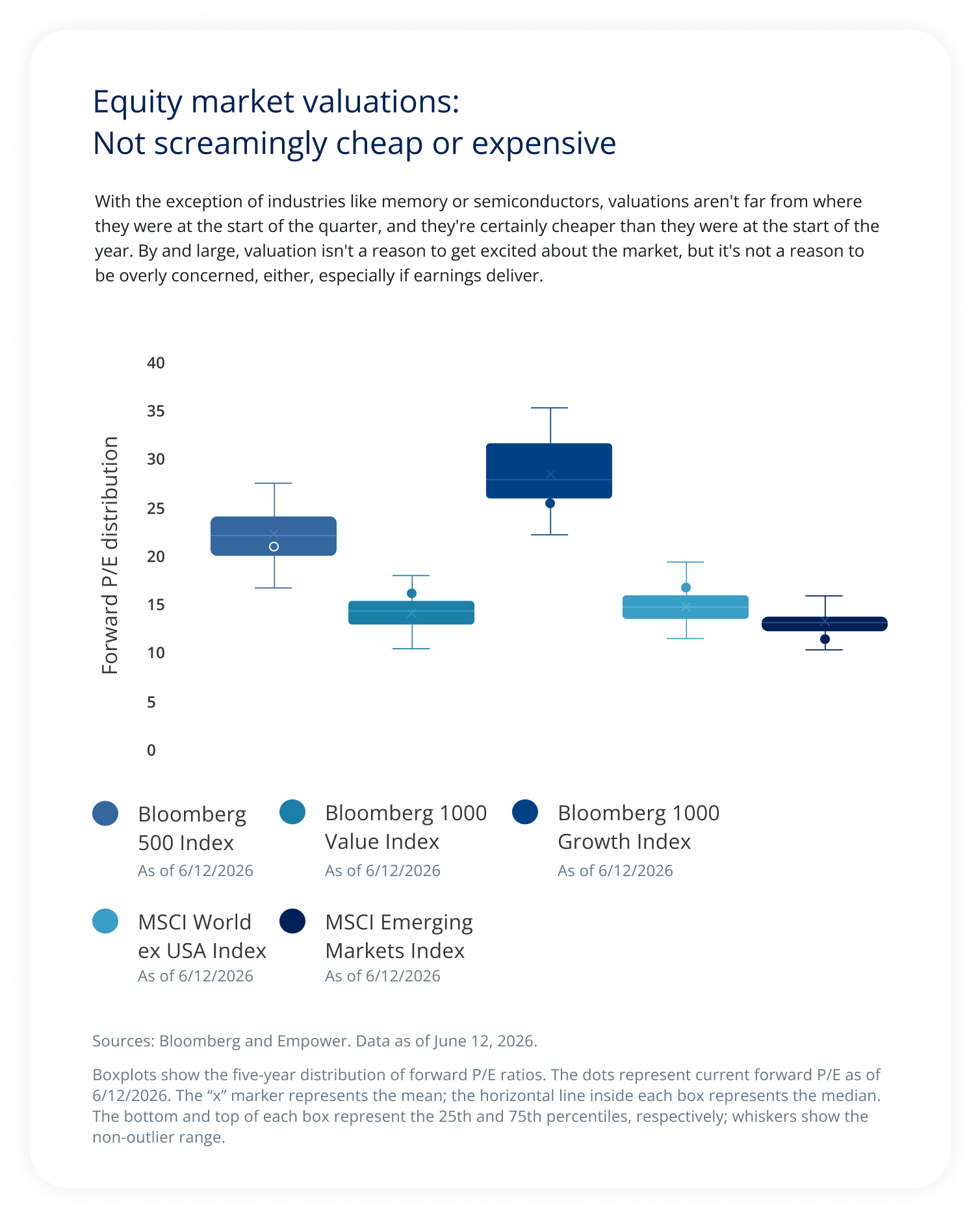

With the exception of industries like memory or semiconductors, valuations aren't far from where they were at the start of the quarter, and they're certainly cheaper than they were at the start of the year. By and large, valuation isn't a reason to get excited about the market, but it's not a reason to be overly concerned, either, especially if earnings deliver.

Bonds

March 2026

We were unconvinced we would get a rate cut in Q2, given the developing Iran War. Still, we were more concerned about the long end of the Treasury curve than the short end. We were sanguine on credit markets, expecting a healthy economy to limit broad credit stress.

We noted cross currents that would complicate monetary policy. Hiring remained weak, but we theorized the Iran War and the resulting surge we expected in headline inflation might cause the Fed to slow its roll.

Within credit, we thought tight spreads made risk-taking less appealing, but we weren’t overly concerned about a massive dislocation given the healthy economy and strong corporate earnings.

Since then

The Treasury curve has shifted higher.

Credit held the line in Q2. The real action was the U.S. yield curve, which climbed across most maturities, but with the largest moves at the short end.

Inflation indeed surged, in line with our expectations. The bigger surprise was the job market, whose sails caught some wind during the second quarter. In particular, payrolls accelerated in May, with hiring broader based than in prior prints. Continued consumer resilience also surprised some market participants.

The trifecta of inflation, jobs strength, and consumer resilience has shifted consensus expectations. After initially expecting cuts over the course of 2026, Fed funds futures now price in the possibility of a rate hike in the back half of the year.

June 2026

We expect the Fed to keep rates steady during the third quarter. We’re rolling forward our credit view.

With limited concern on the economic front and expectations for earnings strength to continue, we remain comfortable expecting minimal credit-market disruption. However, we continue to view tight credit spreads as a warning to avoid excessive risk-taking.

On rates, we’re not entirely aligned with the consensus view. We think the data calls for an extended pause but not yet a hike. New Fed Chair Kevin Warsh may be anxious to leave his thumbprint on policy, which introduces another element of uncertainty, though we view him as a solid choice to lead the Fed.

More specifically, we don’t expect the Fed to adjust rates in the third quarter. While we believe the consumer is resilient, we don’t anticipate strengthening demand; instead, we expect the marginal economic strength to come from AI acceleration. Moreover, we think much of the inflation surge came from the (waning?) conflict in Iran. Higher rates won’t bring that inflation down, nor will it slow the AI spend, though it could create additional pressure on the consumer.

In this climate, bonds may offer a reasonable opportunity. Higher yields today can help compensate investors for the rate and inflation risk while potentially setting fixed-income investors up for better future returns over time.

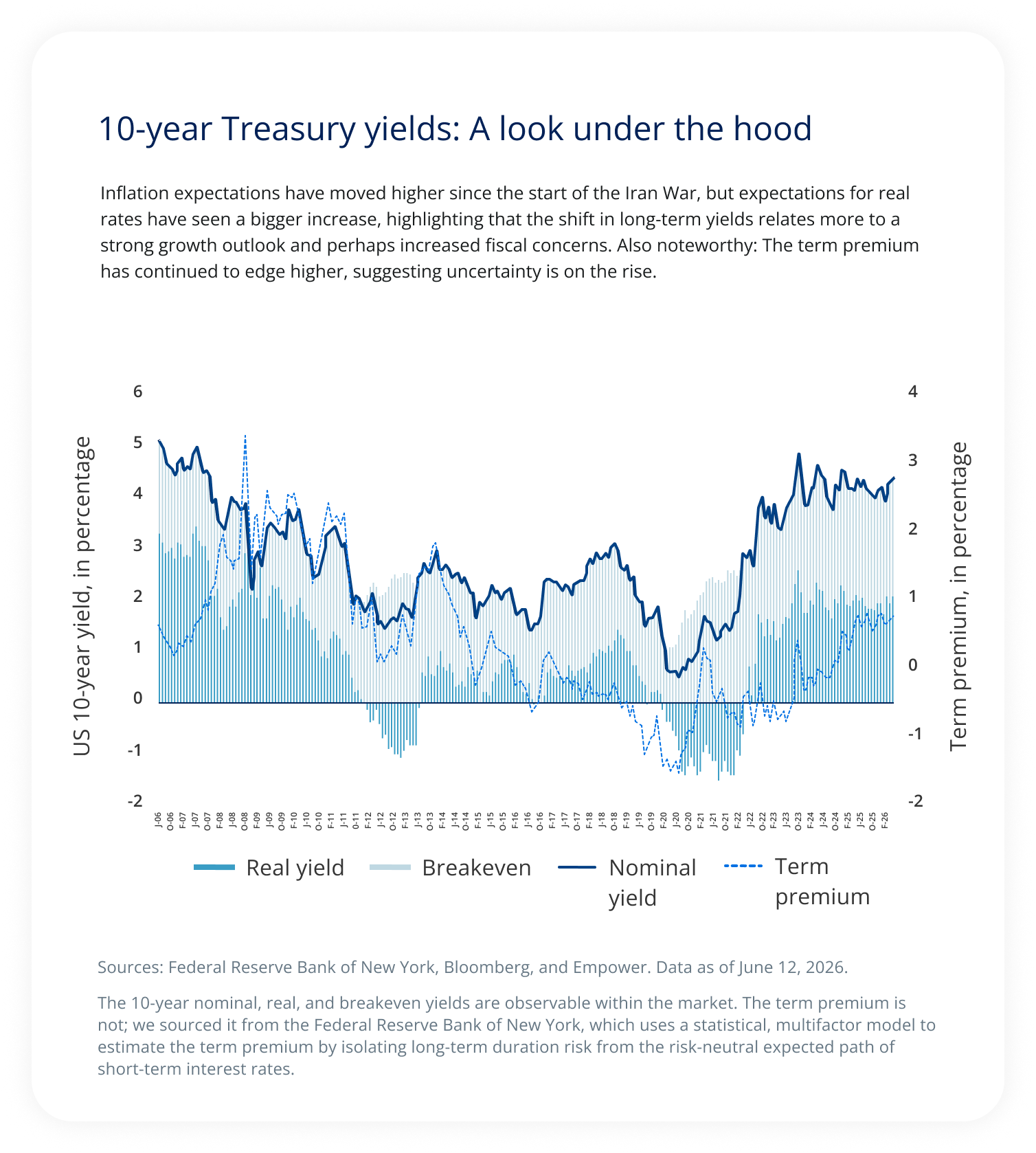

Inflation expectations have moved higher since the start of the Iran War, but expectations for real rates have seen a bigger increase, highlighting that the shift in long-term yields relates more to a strong growth outlook and perhaps increased fiscal concerns. Also noteworthy: The term premium has continued to edge higher, suggesting uncertainty is on the rise.

Asset allocation barometer

Equity

- We think there is a good opportunity for valuation expansion in the Mag 5 (i.e., Nvidia, Meta, Amazon, Microsoft, and Alphabet) and in software, given the significant drawdown. We think limiting exposure to AI bottlenecks, such as memory chips, can make sense; they are vulnerable to major sentiment swings, particularly after the big run in the first half of the year.

- Small-cap stocks remain more attractively priced relative to the broader market, meeting our first condition for the asset class. The second — an accelerating economy — is less certain. We think the economy remains resilient, but we are less sure it will surpass expectations.

- Valuations outside the U.S. have declined, partly due to geopolitical pressures. We are watching for potential opportunities, as easing oil prices could provide support.

- We believe emerging markets could benefit from easing geopolitical tensions, particularly around the Strait of Hormuz. However, we want to be selective in countries like Korea and Taiwan, since they are vulnerable to swings in chip sentiment.

Fixed income

- Short maturity: Higher yields make the asset class more compelling, providing a measure of protection should rate hikes occur. On the flip side, they could benefit from capital appreciation if inflation and rate expectations undershoot.

- Long maturity: Yields are compelling here as well, but fiscal concerns have not eased.

- Credit: Corporate fundamentals remain strong, but spreads are tight, with distressed areas of the market showing some signs of pressure.

Explore the Q3 outlook

Explore the Q3 outlook

Explore the outlook: Overview » Research spotlight: The IPO triple threat »

Stay up-to-date |

“Bloomberg®” and the indices referenced herein (the “Indices,” and each such index – an “Index”) are trademarks or service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the Index (collectively, “Bloomberg”), and/or one or more third-party providers (each such provider, a “Third-Party Provider”) and have been licensed for use for certain purposes to EMPOWER RETIREMENT, LLC (the “Licensee”). To the extent a Third-Party Provider contributes intellectual property in connection with the Index, such third-party products, company names, and logos are trademarks or service marks, and remain the property, of such Third-Party Provider. Bloomberg is not affiliated with the Licensee or a Third-Party Provider, and Bloomberg does not approve, endorse, review, or recommend the financial products referenced herein (the “Financial Products”). Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Indices or the Financial Products.

The Bloomberg 500 Index is a broad measure of the performance of 500 large U.S. companies across major sectors of the U.S. equity market.

The Bloomberg 1000 Value Index measures the performance of U.S. large- and mid-cap companies within the Bloomberg 1000 Index that exhibit value characteristics, such as lower valuation ratios.

The Bloomberg 1000 Growth Index measures the performance of U.S. large- and mid-cap companies within the Bloomberg 1000 Index that exhibit growth characteristics, such as higher expected earnings or sales growth.

The MSCI Emerging Markets Index measures equity market performance across large- and mid-cap companies in emerging market countries.

The MSCI Japan Index measures the performance of large- and mid-cap companies in Japan.

The MSCI UK Index measures the performance of large- and mid-cap companies in the United Kingdom.

The MSCI Europe Index measures the performance of large- and mid-cap companies across developed European markets.

The MSCI World ex USA Index measures the performance of large- and mid-cap companies across developed markets outside the United States.

The S&P 500 Index is a registered trademark of Standard & Poor’s Financial Services LLC. It is an unmanaged index considered indicative of the domestic large-cap equity market and is used as a proxy for the stock market in general..

The opinions expressed represent the current, good-faith views of Empower at the time of publication, are provided for limited purposes, and should not be relied upon as investment or legal advice.

Investing involves risk, including possible loss of principal.

Past performance, where discussed, is not a guarantee of future results. Historical trends and economic data discussed may not be indicative of future conditions which may change.

This material is for informational/educational purposes only; it may not be suitable for all investors; is not tailored to any specific investor’s objectives or financial situation; and is not intended as investment, legal, tax, or accounting advice.

This content is based on information available at the time and may change based on more current conditions. This is neither an endorsement of any security, index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index. References to asset classes or sectors are for illustrative purposes only and are not recommendations.

The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information.

Predictions, opinions, and other information contained in this communication are subject to change without notice and may no longer be true after the date indicated.

Commentary may contain forward-looking statements based on reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve risks and uncertainties that are difficult to predict.

Fixed-income securities are subject to interest rate risk and inflation risk.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved.

INV-WMLPNV-WF-6514196-0626 RO5585287-0626

Investment Insights