Q3 Research spotlight: The IPO triple threat

U.S. economic and market outlook Q3 2026

Research spotlight: The IPO triple threat

U.S. economic and market outlook Q3 2026

Research spotlight: The IPO triple threat

SpaceX. OpenAI. Anthropic.

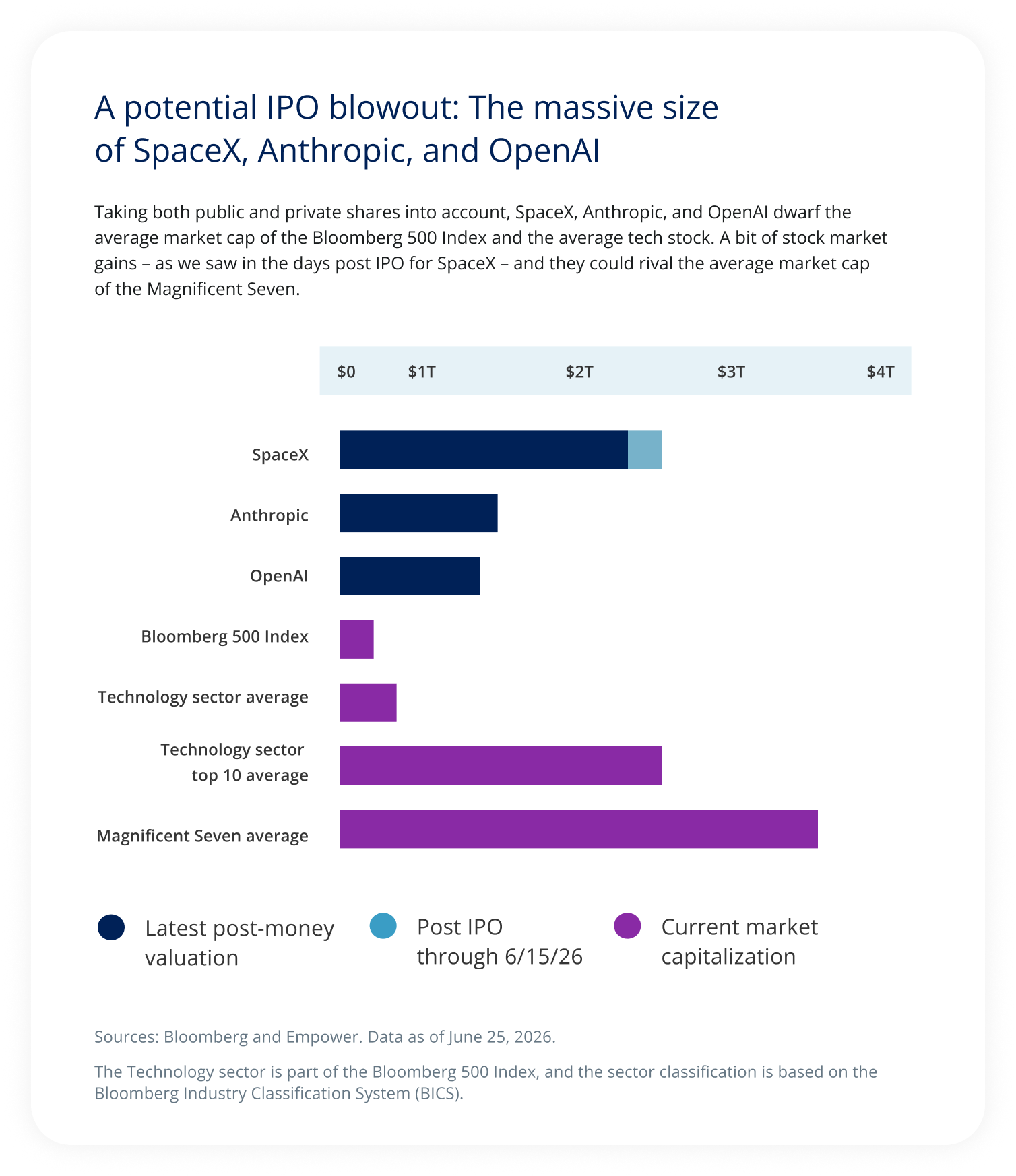

We’re looking at an extra $3.5 to $4 trillion in potential market cap for U.S. equities should all three indeed go public, as currently anticipated, over the next six to 12 months.

That’s roughly 5.4% of the aggregate market capitalization of the members of the Bloomberg 500 Index.

And, if all three were admitted into that proxy at their full valuations across private and public markets, they may very well fall in the index’s top 12 names, pushing past the likes of Eli Lilly or JP Morgan.

Taking both public and private shares into account, SpaceX, Anthropic, and OpenAI dwarf the average market cap of the Bloomberg 500 Index and the average tech stock. A bit of stock market gains – as we saw in the days post IPO for SpaceX – and they could rival the average market cap

of the Magnificent Seven.

This size of cannonball will make an epic splash for all investors, not just those who actively choose to participate (though in the case of SpaceX, it’s fair to say a lot have, and not just institutional investors).

SpaceX reportedly reserved at least 20% or more of its shares for retail investors, roughly twice as much as is typically offered. On open, the stock moved immediately higher; Bloomberg reported that the IPO drew more than $350 billion in demand across institutional and retail investors. |

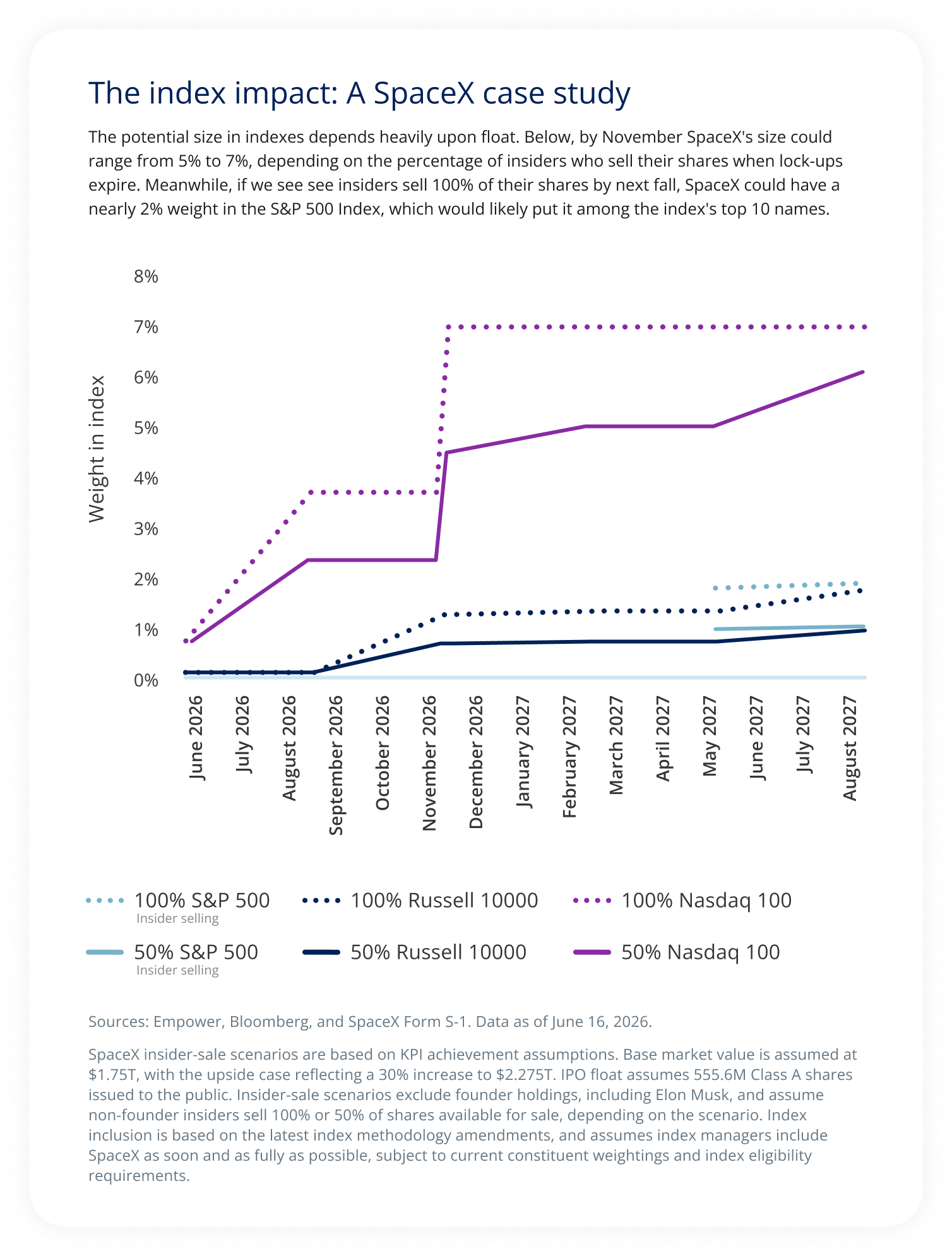

The resulting waves will be with us for quite some time. First, the IPOs of Anthropic and OpenAI are uncertain, though they seem to be gearing up to join the public market later this year. Second, we can’t discount the index impact, which will ripple across investors of all stripes, from institutional investors with index-tracking mandates to individual investors owning passive index funds or ETFs. Even at its limited float, Russell and Nasdaq decided to admit SpaceX within mere days or weeks of its IPO. However, the committee charged with overseeing who’s in and who’s out of the S&P 500® Index declined to change its rules to allow SpaceX to join shortly after its launch, likely delaying its entry to the benchmark for a year.

Those early day inclusions will likely have a modest effect, given SpaceX’s limited public float, which may very well be the blueprint for OpenAI and Anthropic as well. However, as lock-ups1 expire, we could see float increase, which would mean these stocks increasingly take larger roles within indexes, opening the door for additional volatility around quarterly rebalances.

The potential size in indexes depends heavily upon float. Below, by November SpaceX's size could range from 5% to 7%, depending on the percentage of insiders who sell their shares when lock-ups expire. Meanwhile, if we see see insiders sell 100% of their shares by next fall, SpaceX could have a nearly 2% weight in the S&P 500 Index, which would likely put it among the index's top 10 names.

While it’s reasonable to assume these IPOs will only fuel enthusiasm for equities, beware the aftershocks. It’s possible active investors, leery of too much artificial intelligence (AI) exposure, will trim related names — Alphabet seems especially vulnerable given the run it’s had since mid 2025 and its model overlap with Anthropic and OpenAI.

Indeed, we’ve wondered whether we might have already suffered a few foreshocks as SpaceX readied its launch in the form of a brief but intense sell-off in areas where valuations had recently run higher, like semiconductors and memory chips. But it’s the names the indexes could drop to make room for this triple threat, or those that suffer the biggest dilution within the indexes as they elbow their way in, that could see the greatest amount of selling pressure. While that puts the names at the bottom of the table in each of these indexes at risk for relegation, it’s the names toward the top of the list — companies like Nvidia, Apple, Microsoft, and Alphabet — that might see even more intense pressure as their index weights are recalculated to make room.

As we think about this IPO bonanza, it’s not just the market reordering that comes to mind. It’s also the transparency these IPOs bring to the AI trade. One of the biggest questions investors have had focuses on the actual dollars spent on AI, both by consumers and by businesses. With the model businesses going public, we’ll get a look at their earnings on a regular basis and gain a clearer view into the growing AI implementation, for better or for worse.

But there’s an even more foundational question that looms in our minds. Given the heft of these businesses, and the growing influence they will have on public markets as they increase their float, their fundamental prospects matter. What do investors assume about their growth prospects that justify their IPO valuations? And what does that mean for their performance from here?

It’s these questions around fundamentals that animate the rest of our Research Spotlight: The IPO Triple Threat.

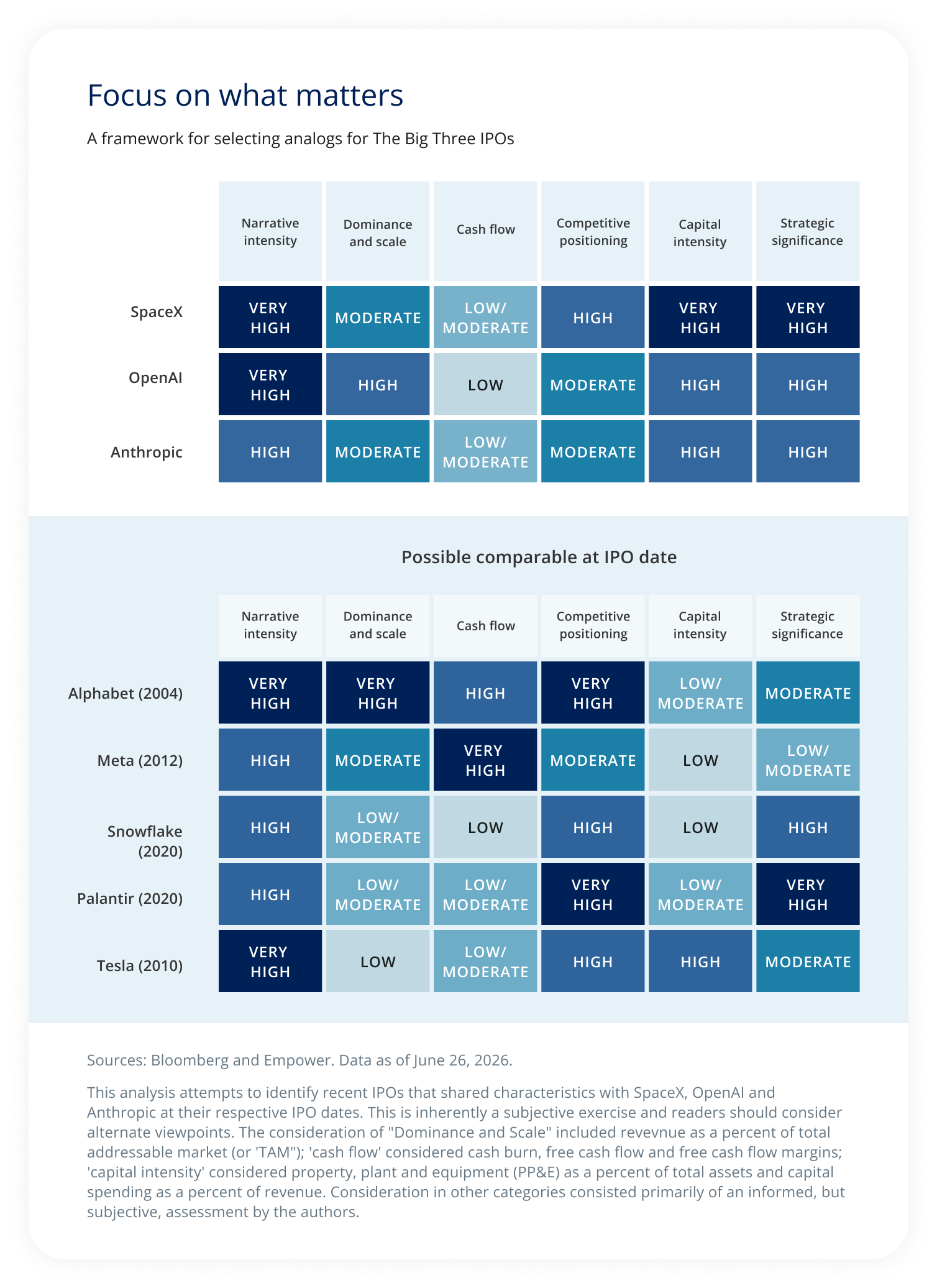

Let’s start with a list of “similars” — firms that have gone public in (relatively) recent memory that share some of the characteristics with our Big Three. That’s a more nuanced analysis than it sounds: Forget for a moment that a company like SpaceX has no perfect peer (after all, its most critical business segment involves launching things into space) and consider instead what matters most following a public listing. It’s not necessarily a company’s business model or the sector it competes in that matters most, but instead things like its pre-IPO “scarcity value,” or strategic significance, and the intensity of the narrative surrounding it.

A framework for selecting analogs for The Big Three IPOs. This analysis attempts to identify recent IPOs that shared characteristics with SpaceX, OpenAI and Anthropic at their respective IPO dates. This is inherently a subjective exercise and readers should consider alternate viewpoints. The consideration of "Dominance and Scale" included revevnue as a percent of total addressable market (or 'TAM"); 'cash flow' considered cash burn, free cash flow and free cash flow margins; 'capital intensity' considered property, plant and equipment (PP&E) as a percent of total assets and capital spending as a percent of revenue. Consideration in other categories consisted primarily of an informed, but subjective, assessment by the authors.

Narrative intensity: The "vibe factor." Was the company well-known to investors and the public before its IPO? Is its name also used as a verb ("just Google it")? Dominance and scale: Is the company early-stage, with revolutionary products but a small footprint, or is it later-stage, with lots of customers and significant revenue as a % of the total addressable market? Cash flow: A newly-public company must eventually generate positive operating cash flow to finance not only its operations, but also its growth. Competitive positioning: Does the firm control its own ecosystem (suppliers, competitors)? Does it have a wide competitive moat? Capital intensity: Does the company low a high fixed asset base? Are capital expenditures as a % of revenue high? Strategic significance: AI is different than other tech revolutions in that it has huge geopolitical significance. That provides some insulation against competition, but also invites regulatory meddling. |

Any such list is inherently subjective and challenged by a lack of data, but we believe the companies in the table above represent reasonable proxies for the Big Three, meaning we can now start to speculate how they might fare after their debuts.

But first, a word from your friendly neighborhood compliance analyst: IPOs are extremely volatile, and a thorough analysis of their prospects both pre- and post-IPO is made almost impossible by a lack of fundamental data and near-total absence of any real trading history. We had a head start on SpaceX given the timing of its filing and release of its S-1, but everything that follows is still speculative at best, and readers are strongly cautioned to exercise prudence and conduct their own due diligence.

With that disclaimer out of the way, here’s how our list of proxies performed in the days and weeks following their IPOs.

Post-IPO stock-price performance' reflects price return for each company's stock during the periods specified, relative to their IPO price. Price return for the 3-year period is annualized. 'Revenue growth' reflects year-over-year growth for each of the first five fiscal years following each company's IPO.

With only one exception — Meta (aka Facebook) — the proxies on our list enjoyed very strong price performance immediately after launch, the so-called “IPO-pop” that attracts so many starry-eyed traders in the first place. And without exception, topline growth continued to excel, too — even if profitability was more mixed. That might bode well for our Big Three, all of which are priced as if revenue growth will remain stratospheric for the next decade or more.

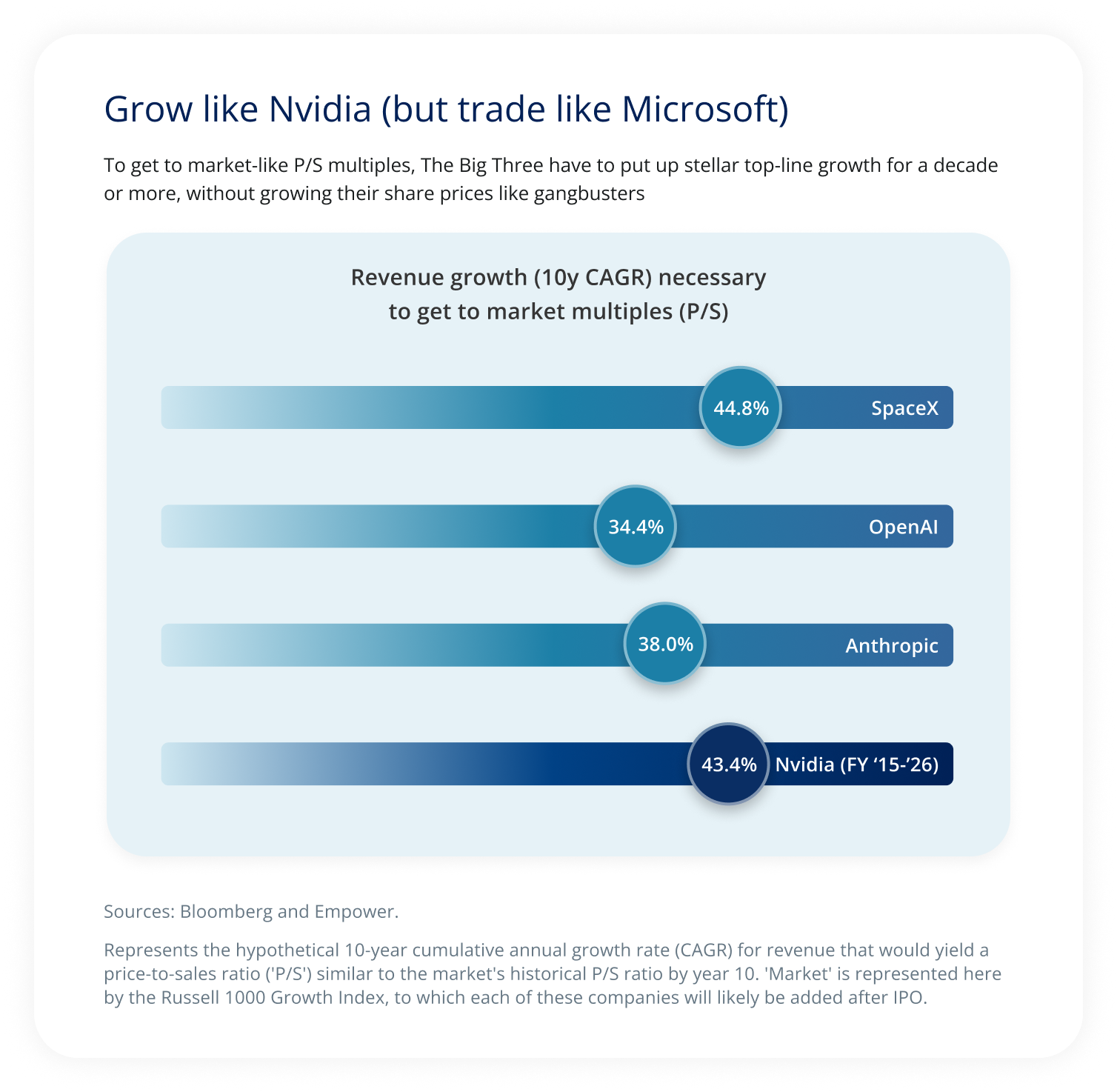

Represents the hypothetical 10-year cumulative annual growth rate (CAGR) for revenue that would yield a price-to-sales ratio ('P/S') similar to the market's historical P/S ratio by year 10. 'Market' is represented here by the Russell 1000 Growth Index, to which each of these companies will likely be added after IPO.

These are high bars to clear, and at first glance it’s encouraging that many of our Big Three proxies were up to the challenge. But remember that sales and earnings represent only the denominator of any self-respecting valuation ratio: Price action — which serves as the numerator — matters just as much. So even with 40%-plus topline growth, valuations might not look reasonable if the stocks trade very aggressively for the foreseeable future. In fact, one of the unmistakable conclusions of this research for us was that for its valuation to seem rational anytime during the next decade, a stock like SpaceX may need to “grow like Nvidia but trade like Microsoft” to support valuation expectations over time.

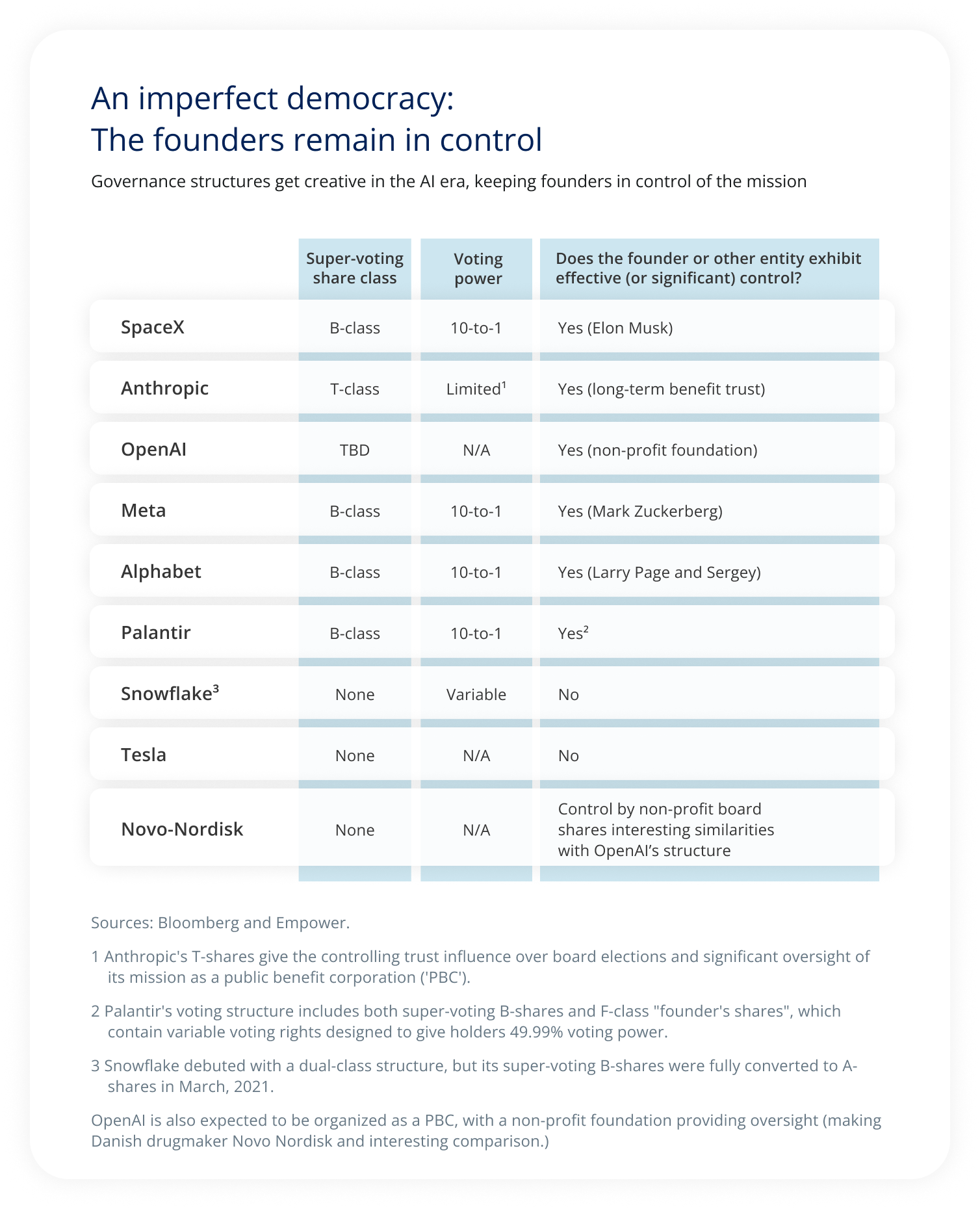

Deal particulars matter, too. For example, it’s not lost on institutional investors that SpaceX’s “B-shares” carry 10 times the voting power of the A-class shares being floated to the public, leaving company founder and CEO Elon Musk effectively in control of the firm and making it nearly impossible to remove him from his seat at the helm. And while that’s become a major sticking point for some institutions, other firms in our proxies list have similar — although arguably less draconian — characteristics when it comes to control.

Perhaps that’s a reflection of exactly how disruptive — both socially and economically — AI might be (which, for example, is one reason why Anthropic is expected to allow a long-term benefit trust associated with its status as a public benefit corporation to exert significant control over its corporate governance, and why OpenAI is likely to continue to yield significant power to its nonprofit board).

Or perhaps this is all just a function of how capital markets have evolved: Many of today’s IPO stars are led by a charismatic founder with a clear, even startling, vision of the future, and they’re waiting longer and longer to hand over even a portion of control of that dream to outsiders. That gives their leaders large, fast-growing franchises over which they’re understandably reluctant to cede control.

Governance structures get creative in the AI era, keeping founders in control of the mission.

Sources: Bloomberg and Empower.

1 Anthropic's T-shares give the controlling trust influence over board elections and significant oversight of

its mission as a public benefit corporation ('PBC').

2 Palantir's voting structure includes both super-voting B-shares and F-class "founder's shares", which

contain variable voting rights designed to give holders 49.99% voting power.

3 Snowflake debuted with a dual-class structure, but its super-voting B-shares were fully converted to A-

shares in March, 2021.

OpenAI is also expected to be organized as a PBC, with a non-profit foundation providing oversight (making Danish drugmaker Novo Nordisk and interesting comparison.)

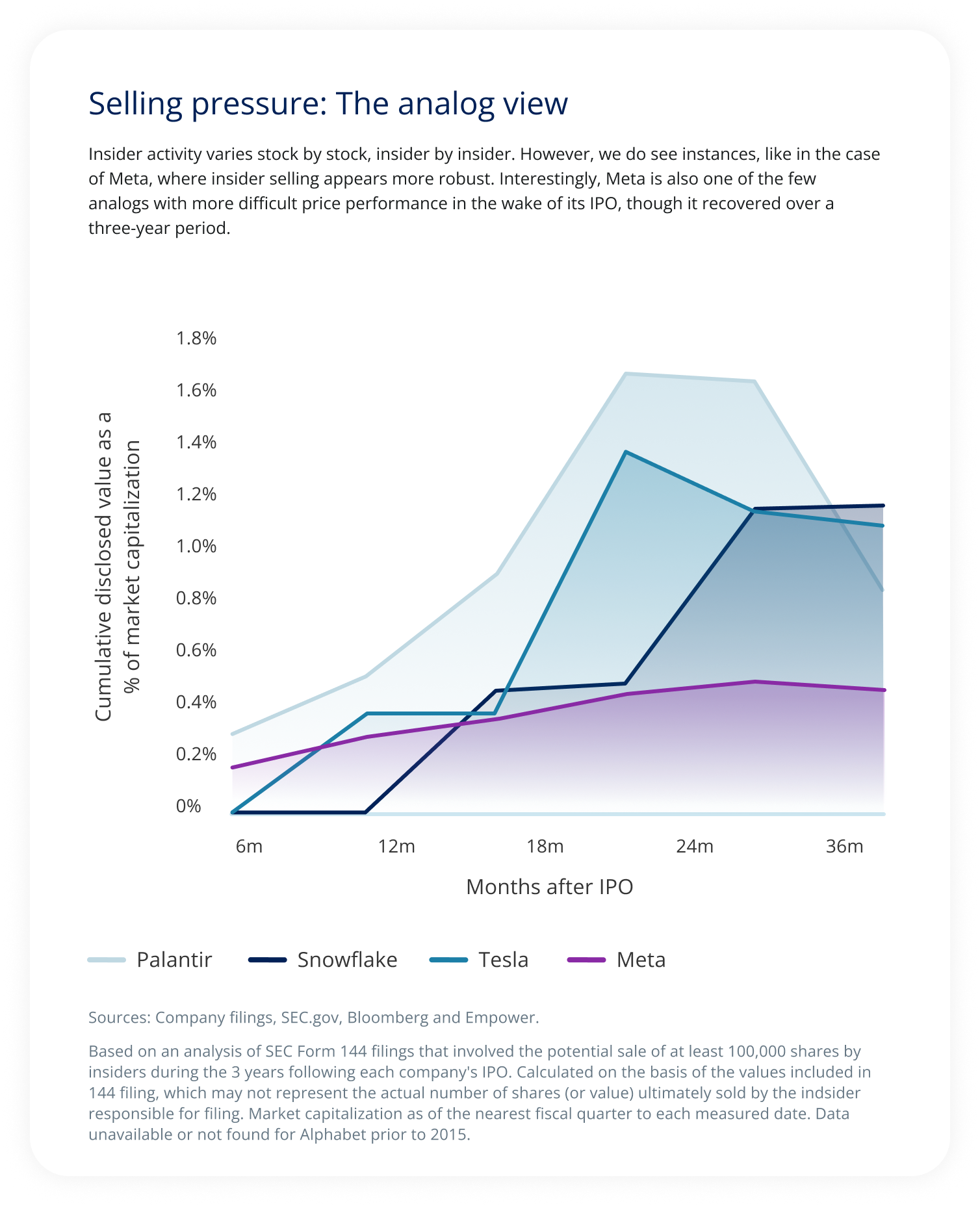

But the “founder’s dilemma” contains another caution for investors: insider selling. Traditionally, one of the more powerful incentives that private companies have had for listing their shares in public markets is to allow founders, co-founders, and early insiders to monetize their stakes. And while there’s nothing fishy or even mildly suspect about it, it’s still another potential pitfall to be aware of, particularly around lock-up dates, as we alluded to above in our discussion of continued volatility.

Based on an analysis of SEC Form 144 filings that involved the potential sale of at least 100,000 shares by insiders during the 3 years following each company's IPO. Calculated on the basis of the values included in 144 filing, which may not represent the actual number of shares (or value) ultimately sold by the indsider responsible for filing. Market capitalization as of the nearest fiscal quarter to each measured date. Data unavailable or not found for Alphabet prior to 2015.

At the end of the day, though, investing in any IPO — maybe even more so for these Big Three — means signing off on a vision: Whether you invest in Anthropic’s vision of dominating the entire enterprise AI value chain from development to deployment, OpenAI’s ambition to create artificial general intelligence for the benefit of all humanity, or SpaceX’s dream of establishing human colonies on Mars, you’re betting not only that the vision is worthwhile and achievable, but also that the company will meet various endpoints and milestones along the way. And point of order: Passive investors will increasingly make that bet, if and when these companies compose a larger part of broad-market indexes.

Interesting times ahead.

Explore the Q3 outlook

Explore the Q3 outlook

Explore the outlook: Overview » Research spotlight: The IPO triple threat »

Stay up-to-date |

1 A lock-up is a restriction companies place on early investors/insiders from selling their shares to the public market. Typically they are restricted for a period of time post-IPO to help limit a deluge of selling from hurting the public stock price.

This material is for informational purposes only and is not intended to provide investment, legal, or tax recommendations or advice.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. INV-WMLPNV-WF-6527700-0626 RO5590791-0626

Investment Insights