Q2 outlook overview 2026

U.S. economic and market outlook 2026

Q2 outlook overview

U.S. economic and market outlook 2026

Q2 outlook overview

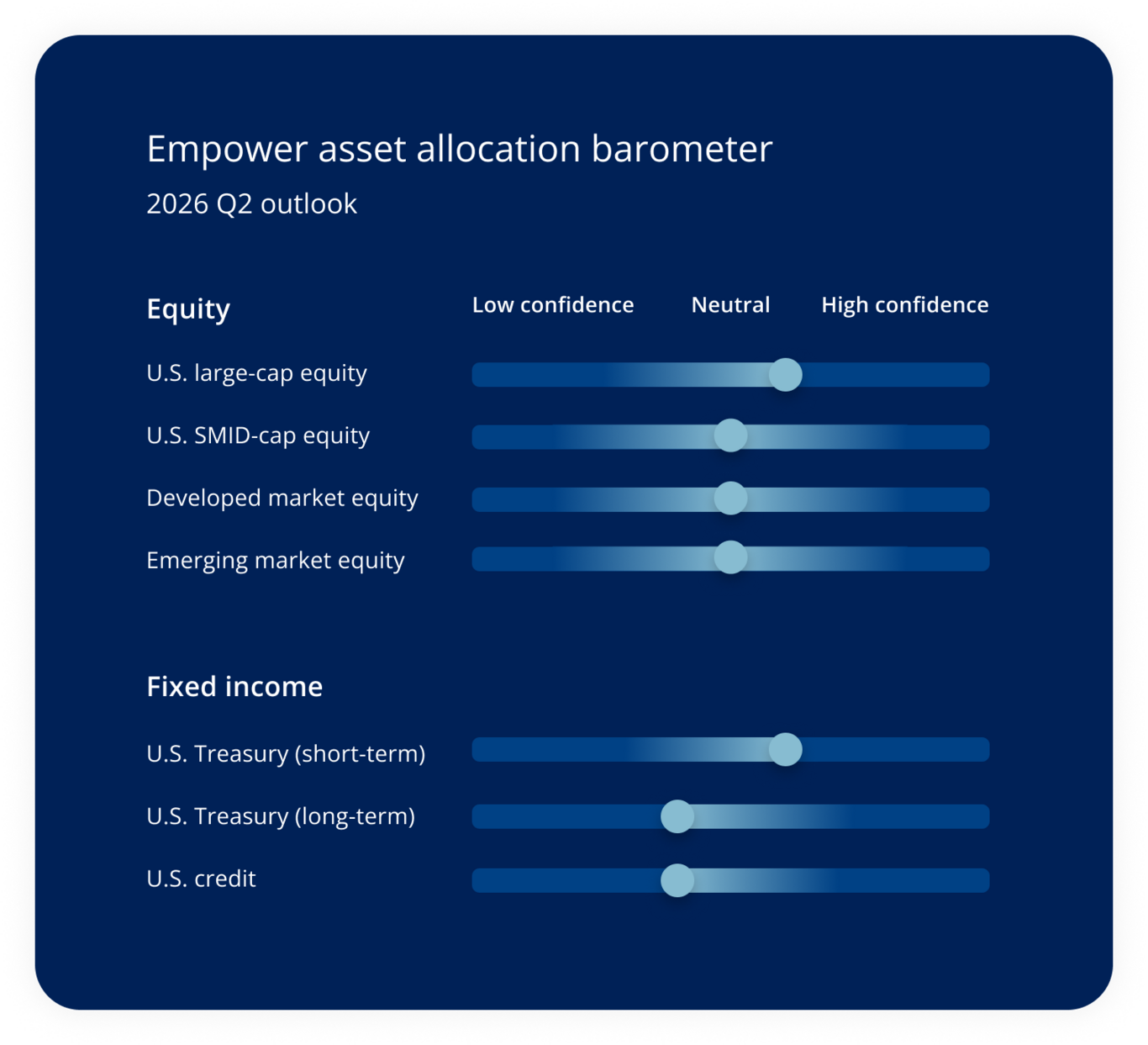

Asset allocation barometer

Equity

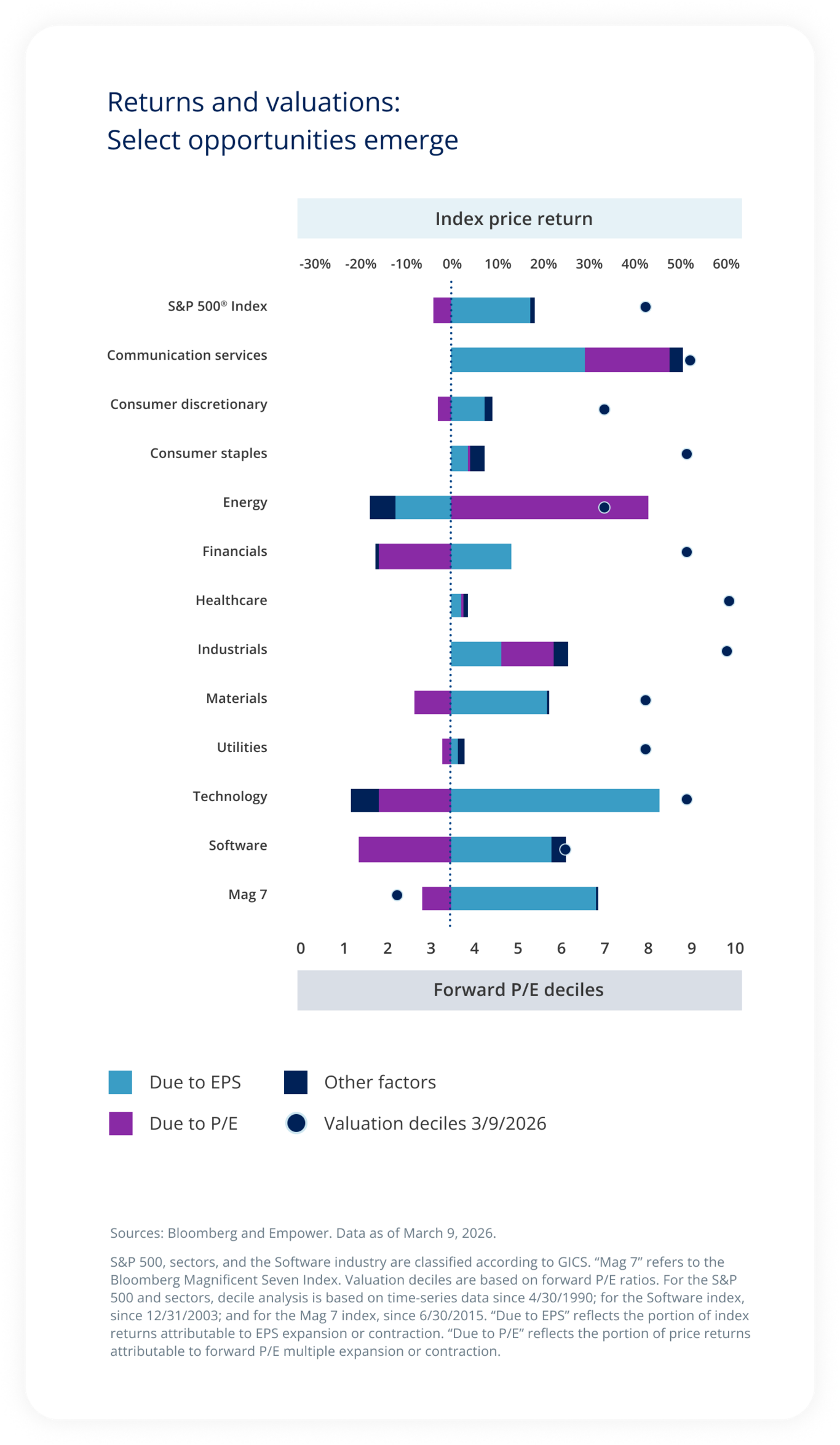

- As an asset class, we don't consider U.S. large caps attractive. Nevertheless, we think valuation opportunities have emerged in software and the Magnificent Seven (Mag 7), giving us more interest in targeted areas.

- Small-cap stocks remain more attractively priced relative to the broader market, meeting for our first condition for the asset class. The second — an accelerating economy — is less of a given. We think the economy is resilient, but not necessarily likely to surprise to the upside.

- Valuations have moved higher outside the U.S., though geopolitical pressure is pulling them down in real time. We are monitoring for opportunities.

- As with developed equities, geopolitical pressure is pulling emerging market valuations down in real time. We think this space is worth watching.

Fixed income

- Short-Term U.S. Treasuries: Yields remain compelling, paying us to wait for the next Fed cut.

- Long-term U.S. Treasuries: Yields are compelling here, too, but fiscal concerns make us modestly less constructive on the long end of the yield curve.

- Corporate fundamentals remain strong, but spreads are tight, with distressed areas of the market showing some signs of pressure.

Economy

A look back on November 2025

We believed artificial intelligence (AI) loomed larger than the traditional economic cycle

Our view was that the wild levels of spending by the hyperscalers — the AI providers — had created a new growth engine for the economy that was far more capital intensive and potentially less dependent on the U.S. consumer.

We nevertheless tracked the health of the consumer. Though we saw signs of weakening amid the lower-income cohort, we believed the mass market was buttressed by massive wealth creation from the housing market.

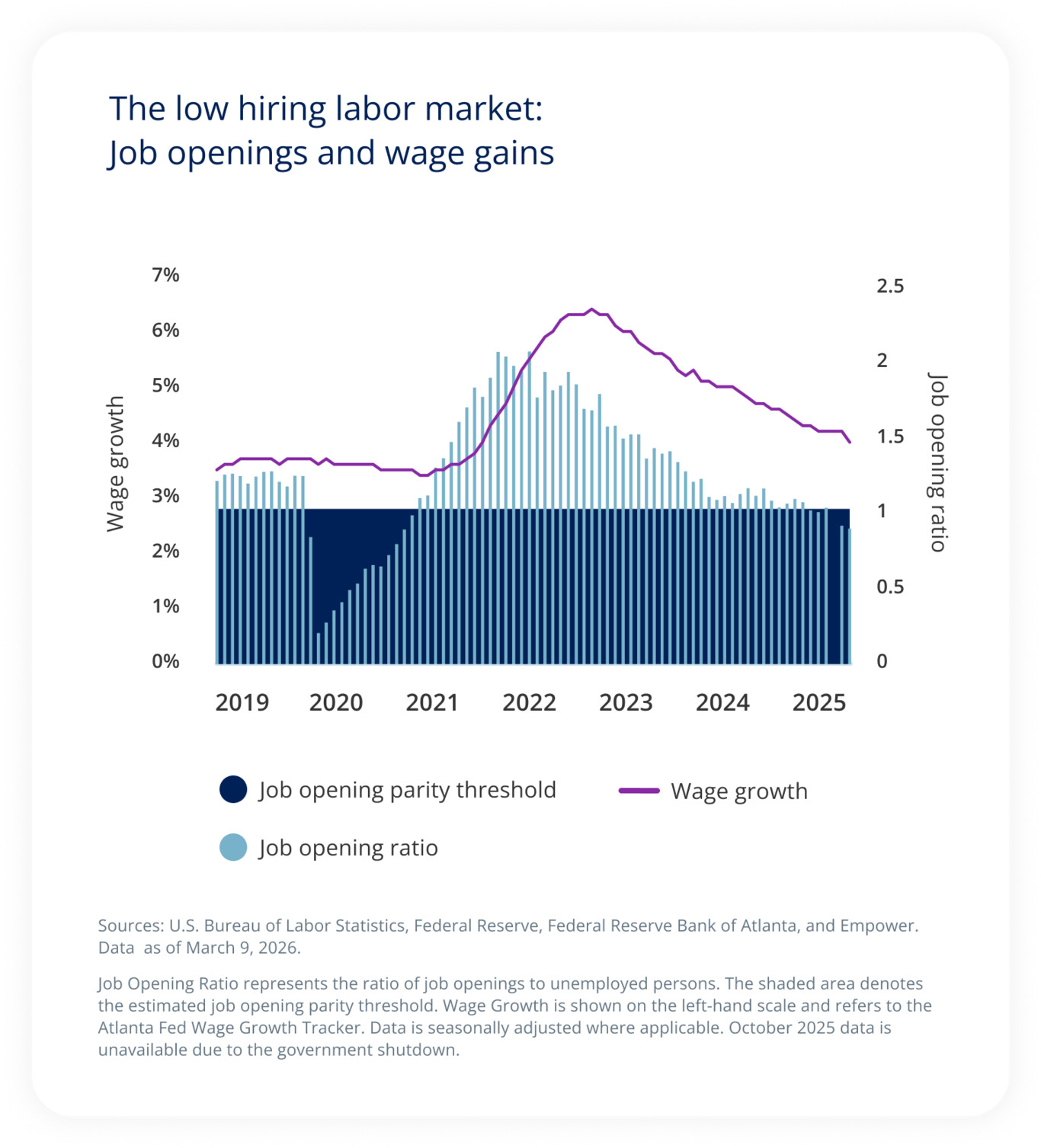

We noted deterioration in the labor market, but, due to strong corporate earnings, didn’t anticipate concerning levels of unemployment.

Since then

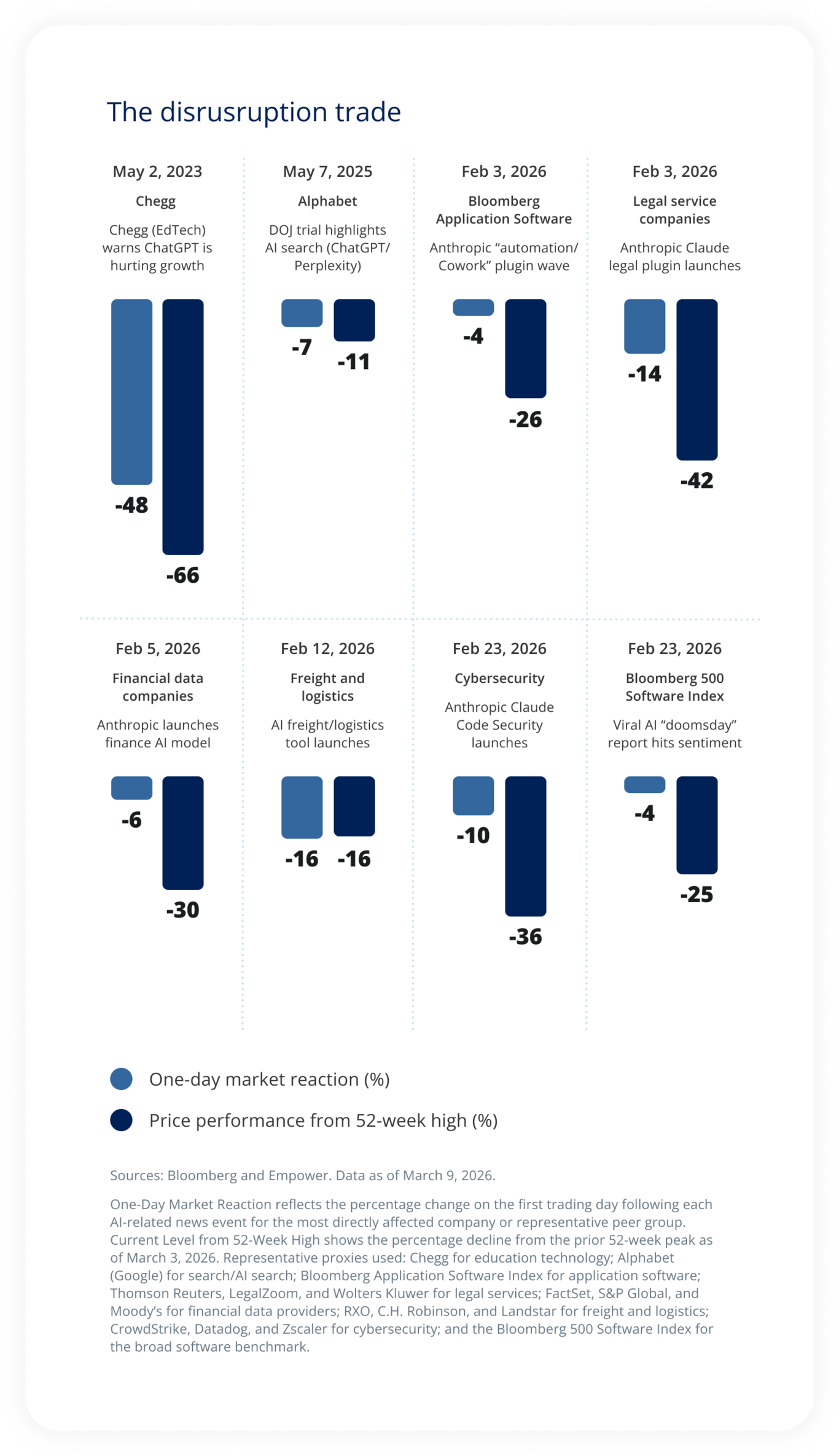

Indeed, Q1 has been all about AI

The AI spend continued to accelerate, with impacts felt across the AI supply chain. As announcements for new AI capabilities landed, economists and investors alike worried about the potential implications for affected industries, largely within the white-collar workforce.

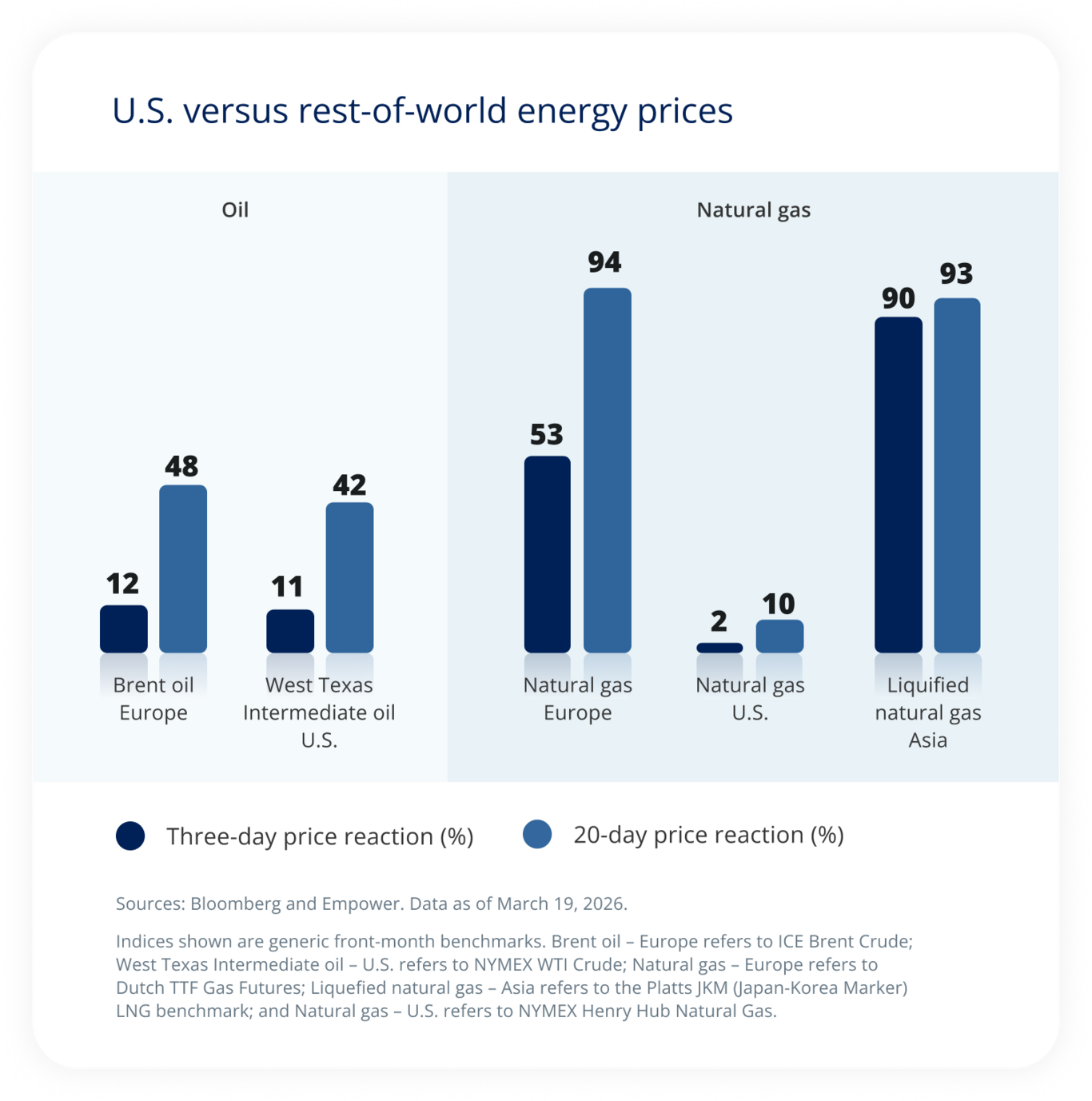

Geopolitical risk was the surprise of the quarter, with the Trump administration launching military strikes against Venezuela and Iran. The first has limited economic impact, but the second has the potential for greater disruption, particularly for energy importers.

March 2026

We expect further transformation from AI but must keep an eye on outside factors as well

We believe the AI data-center build is only in the second or third inning, which suggests it will likely remain an economic force for quarters to come, particularly in areas like memory chips (used for AI training and inference), construction and related materials (to build the data centers), and energy (as regulators attempt to manage the emerging energy demand).

Meanwhile, AI implementation is still in its infancy — we don’t expect a near-term economic transformation. However, with version-one AI capabilities emerging, we are monitoring signs of possible disruption in early impact industries like software. (So far so good: Evidence suggests software labor demand has remained stronger than the weak trends in the economy overall.)

The labor market on the whole deserves attention given the softness in hiring and the quieter pace of wage gains. However, we believe part of this is the result of economic normalization in the wake of the post-pandemic hiring surge, and we maintain our view that strong earnings will likely keep broad-based layoffs at bay in the near term.

The campaign against Iran has do-or-die characteristics and, as a result, may stretch at least into the early part of the second quarter. If so, we expect continued disruption to energy prices. This matters some to the U.S., but its status as the world’s largest oil and natural gas producer1 helps limit the worst effects of a supply disruption. Asian and European economies, both heavy importers, have greater vulnerability, particularly in natural gas.

We anticipate a temporary hit to headline inflation in the U.S. and a more moderate hit to core inflation.

Stocks

A look back on November 2025

The U.S. equity market increasingly looked dependent on AI

This risk was of course present in the size of the Mag 7 market cap, where many of the AI suppliers reside. However, it also reflected their relative revenue, earnings, and spending contributions to the overall market.

We were also leery of valuations — not just for technology — but across most sectors, with the possible exceptions of energy and healthcare. Our long-term valuation analysis suggested that nearly all sectors in the U.S. were at the high end of their respective ranges.

Still, we didn’t anticipate the U.S. stock market to collapse: The Fed had restarted its cutting campaign, fiscal stimulus was on its way (if not already at work), the consumer continued to spend, and earnings across sectors looked set to deliver.

Since then

Q1 returns have largely disappointed, with flat performance followed by geopolitical volatility

This was particularly true for the Mag 7, which delivered strong financial results but failed to inspire investors as AI doubt won out over AI excitement.

Despite their skepticism around the AI build, investors panicked as announcement after announcement of new AI capabilities rocked select industries. Investors worried legacy businesses like software would face new competition from AI model providers, squeezing their margins, potentially all the way to zero.

Not all was lost for U.S. investors: Forgotten sectors of the market started strong in 2026, including cyclical areas like energy and defensive areas like consumer staples.

They arguably benefited from two mildly contradictory narratives:

- The U.S. economy was on an upswing, particularly due to AI spending, benefiting areas like energy, industrials, and materials.

- Investors needed to take cover from the AI effect, hiding in unrelated areas (consumer staples).

March 2026

Potential selective opportunities have emerged

With AI exhaustion causing weaker results, select names within the Mag 7 now generally appear more attractively priced, boasting intact fundamentals but low valuations. In fact, as an aggregate, these stocks are nearly as cheap as they were post Liberation Day.

We also tend to view software as attractive; investors have sold the space en masse, with little distinction between potential winners and losers. However, we’re highly aware that fundamental risk has spiked due to the possibility that some of these companies may see greater revenue pressure. Relatedly, sentiment may remain aligned against these names in the near term.

Outside these select opportunities, we’re ambivalent about the U.S. equity market. We continue to recognize strong earnings generally across the board, but valuations offer little margin of safety for sectors like consumer staples, industrials, materials, or financials.

Bonds

A look back on November 2025

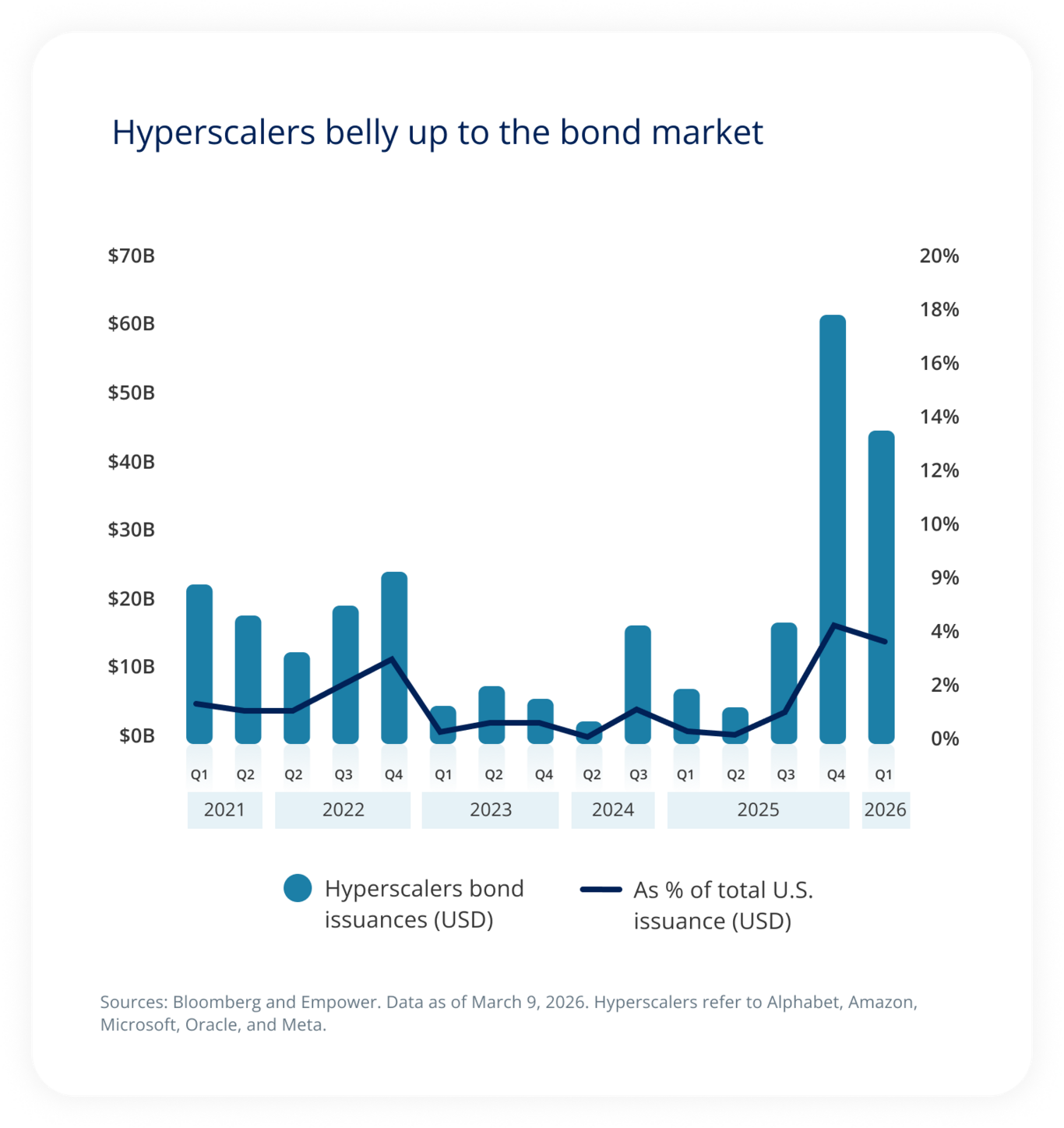

Hyperscaler debt issuance caught our attention, but we nevertheless expected a steady state for Q1

Credit spreads were tight, but fundamentals — both earnings and balance sheets — seemed solid.

Yields had come down across most fixed-income sectors but remained higher than 2022 levels, allowing returns to continue to benefit from higher coupons.

We expected a moderate pace of rate cuts, pushing back against the notion that the Fed funds rate was headed markedly lower.

Since then

Fixed-income markets were well behaved in Q1

Broad credit markets showed little sign of stress, though credit related to software and private credit lenders saw pressure build.

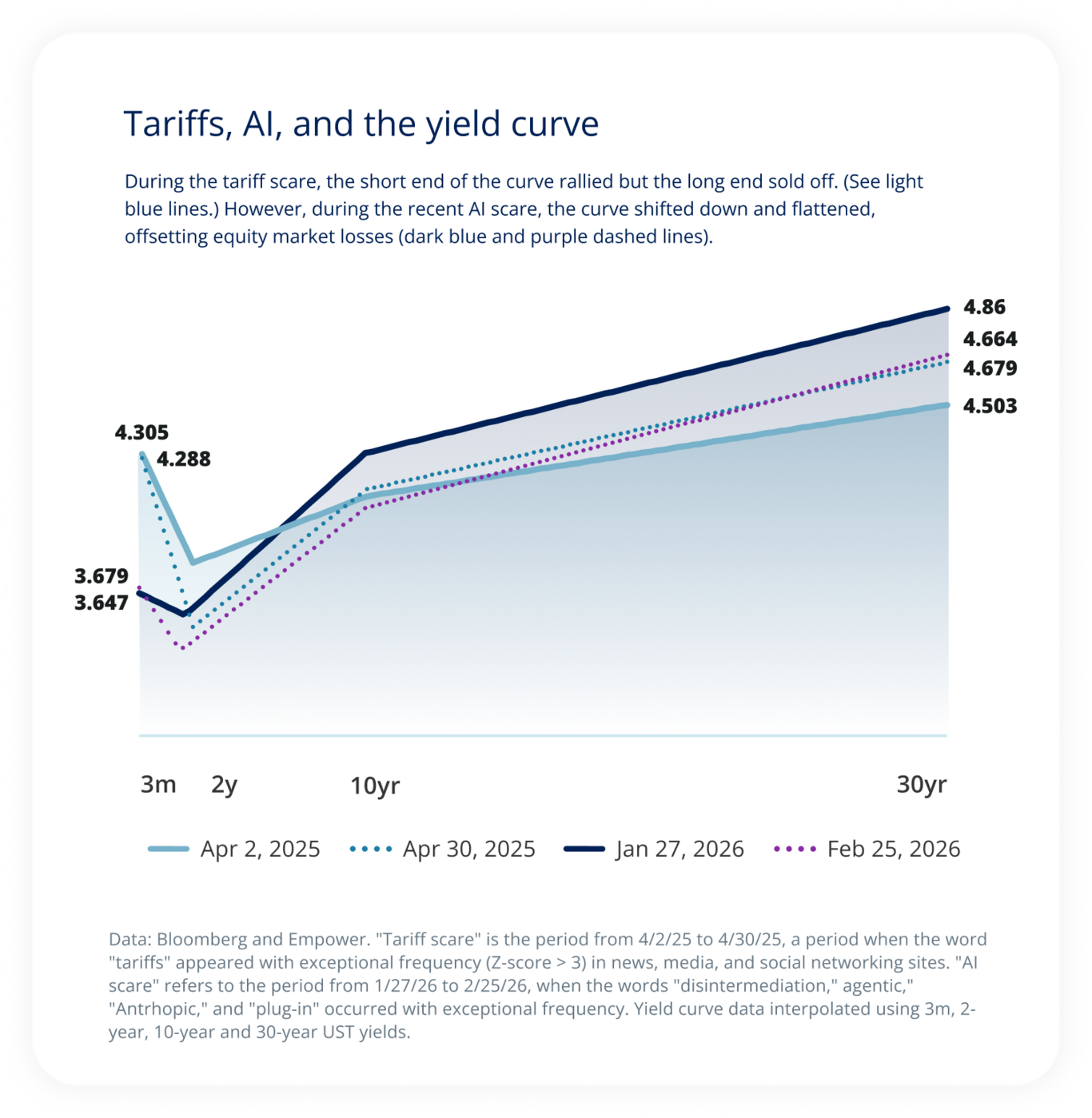

We saw some welcome defense from fixed income when U.S. equity markets stumbled, underscoring the value of higher yields. This is in contrast to prior periods, when bonds offered less protection, and highlights the difference in concern in Q1: business-model disruption rather than inflation concerns.

March 2026

We’re rolling forward our rate and credit expectations

We expect rates could edge lower over the course of 2026, though it’s unclear to us whether we will get a cut in Q2. Cross currents are fierce: Nominated chair Kevin Warsh likely has a predisposition to cut rates, and certainly hiring remains weak, but the Iranian war and the potential impact on headline inflation likely pushes against near-term cuts. We expect the longer end of the curve, which so far has failed to follow the typical cutting-cycle trajectory, to remain range bound.

If U.S. stocks face pressure from concerns around AI disruption, we expect the bond market could act as an offset. If energy price pressure persists, we would expect less U.S. Treasury market support.

Despite tight spreads, we remain sanguine on broad market credit, though we expect pressures to continue in more distressed areas. We continue to monitor hyperscaler debt issuance, but we don’t see imminent concern for the high-quality issuers that dominate public equity markets.

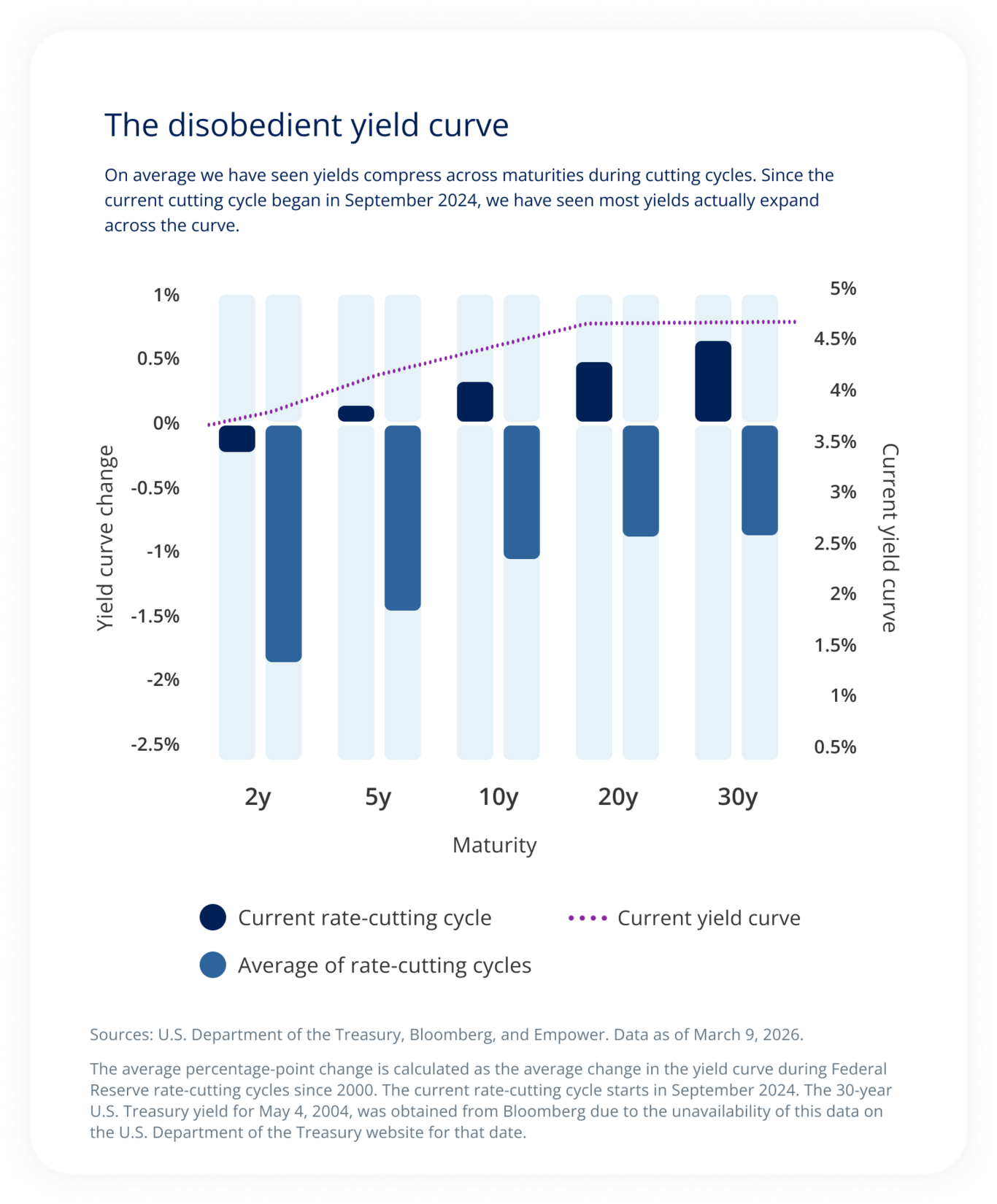

On average we have seen yields compress across maturities during cutting cycles. Since the current cutting cycle began in September 2024, we have seen most yields actually expand across the curve.

On average we have seen yields compress across maturities during cutting cycles. Since the current cutting cycle began in September 2024, we have seen most yields actually expand across the curve.

On average we have seen yields compress across maturities during cutting cycles. Since the current cutting cycle began in September 2024, we have seen most yields actually expand across the curve.

Sources: Bloomberg and Empower. Data as of March 9, 2026. Hyperscalers refer to Alphabet, Amazon, Microsoft, Oracle, and Meta.

Explore the Q2 outlook

Explore the Q2 outlook

Explore the outlook: Overview » Research spotlight: Affordability»

Stay up-to-date |

1 U.S. Energy Information Administration.

The research, views, and opinions contained in these materials are intended to be educational; may not be suitable for all investors; and are not tax, legal, accounting, or investment advice.

Investing involves risk, including possible loss of principal. The opinions expressed in this communication represent the current, good-faith views of Empower at the time of publication and are provided for limited purposes, are not intended as investment or legal advice, and should not be relied on as such. This content is based on the information available at the time of the recording and may change based on more current conditions. Past performance, where discussed, is not a guarantee of future results. Investing involves risk. This is neither an endorsement of any index, sector, or investment, nor a solicitation to offer investment advice or sell products or services offered by Empower or its affiliates. It is impossible to invest directly in an index. The information presented was developed internally and/or obtained from sources believed to be reliable; however, Empower does not guarantee the accuracy, adequacy, or completeness of such information. Predictions, opinions, and other information contained in this communication are subject to change and without notice of any kind and may no longer be true after the date indicated.

Commentary may contain forward-looking statements based on reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict.

The S&P 500® Index (“Index”) and associated data are a product of S&P Dow Jones Indices LLC, its affiliates and/or their licensors and has been licensed for use by Empower Retirement, LLC. ©2026 S&P Dow Jones Indices LLC, its affiliates and/or their licensors. All rights reserved. Redistribution or reproduction in whole or in part are prohibited without written permission of S&P Dow Jones Indices LLC. For more information on any of S&P Dow Jones Indices LLC’s indices please visit spdji.com. S&P® is a registered trademark of Standard & Poor’s Financial Services LLC (“SPFS”) and Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). Neither S&P Dow Jones Indices LLC, SPFS, Dow Jones, their affiliates nor their licensors (“S&P DJI”) make any representation or warranty, express or implied, as to the ability of any index to accurately represent the asset class or market sector that it purports to represent and S&P DJI shall have no liability for any errors, omissions, or interruptions of any index or the data included therein.

The research, views, and opinions contained in these materials are intended to be educational; may not be suitable for all investors; and are not tax, legal, accounting, or investment advice.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries. “EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

Empower and its affiliates are not providing impartial investment advice in a fiduciary capacity to the plan with respect to this material. The plan fiduciaries are solely responsible for the selection and monitoring of the planʼs investment options and for determining the reasonableness of all plan fees and expenses.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries. This material is for informational purposes only and is not intended to provide investment, legal, or tax recommendations or advice.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. INV-FBK-WF-5933000-0326 RO5271151-0326

Investment Insights