The Currency

Be current.

Be current.

Get insights and intel on your money.

*If you’re already registered with Empower, please use the same email address as your existing account.

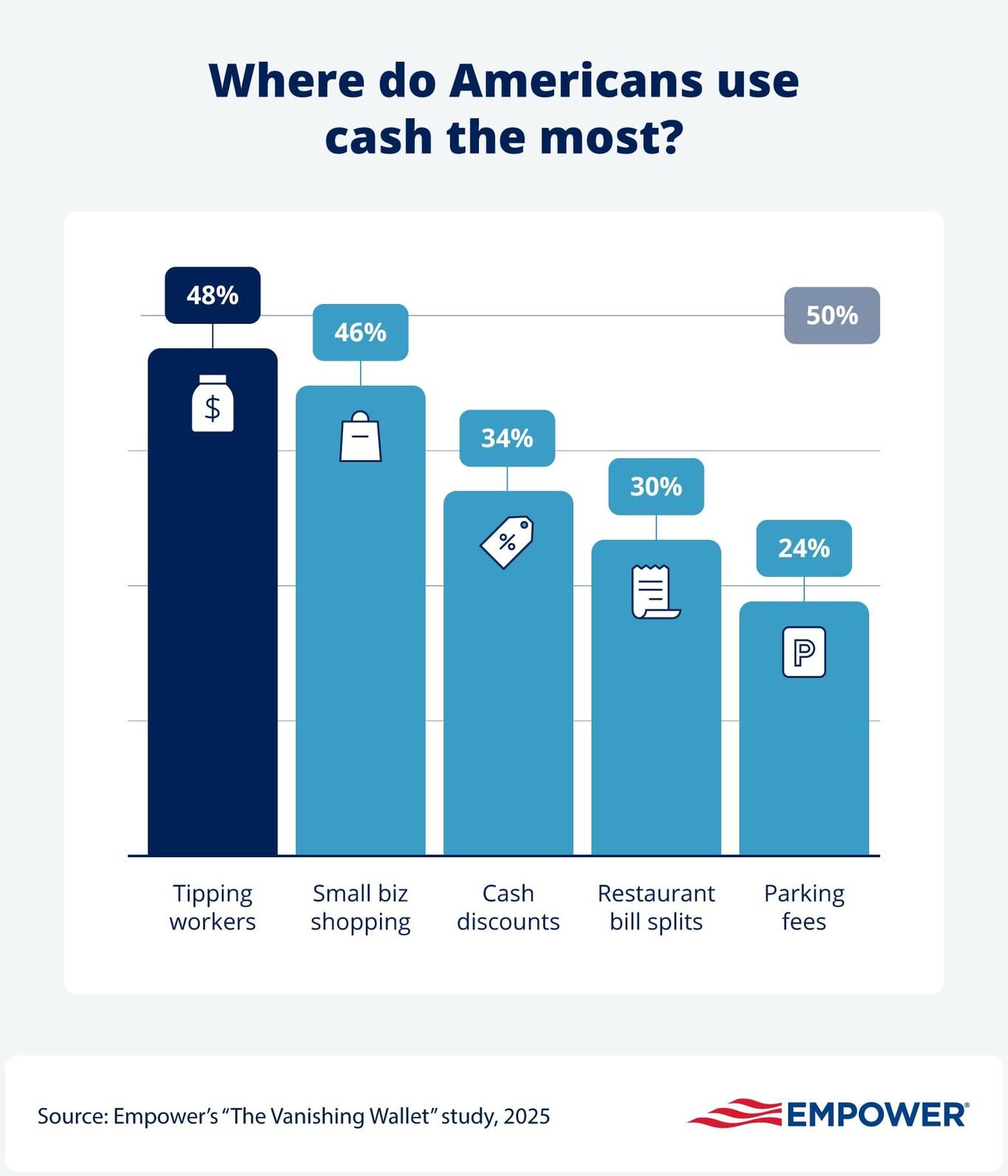

A third of Americans say they’re mostly cashless, though people can opt for physical money for specific reasons, according to Empower research:

A third of Americans say they’re mostly cashless, though people can opt for physical money for specific reasons, according to Empower research:

Explore by topic

Is a 529 plan worth it? Pros, cons, and when it makes sense

Money

Theme Slug

category--money

Pathauto Slug

money

Tax advantages, flexible rules, and long-term growth potential can make 529 plans a compelling way to save for education.

HSA contribution limits 2026 and 2027: Max contribution & eligibility

Money

Theme Slug

category--money

Pathauto Slug

money

Find the 2026 and 2027 HSA contribution limits, including max contribution amounts, eligibility updates, deadlines, and key rules to know.

Make a financial 'go bag': 10 documents you need in an emergency

Money

Theme Slug

category--money

Pathauto Slug

money

When you need to handle finances on the go, these important documents can keep your necessary information safe and secure.