Empowering America’s Financial Journey Government Sector 2026

Empowering America’s

Financial Journey™

Government sector

Fifth edition

Empowering America’s

Financial Journey™

Government sector

Fifth edition

Government retirement plans have remained remarkably stable over the past several years. Participation is steady. Savings behavior is consistent. Engagement continues to improve.

That stability reflects a durable foundation. But stability isn’t the same as readiness.

Financial lives are more complex and retirement outcomes are increasingly shaped by factors both inside and outside a plan. The opportunity ahead is to turn consistent behavior into stronger long-term outcomes.

Key insights

1

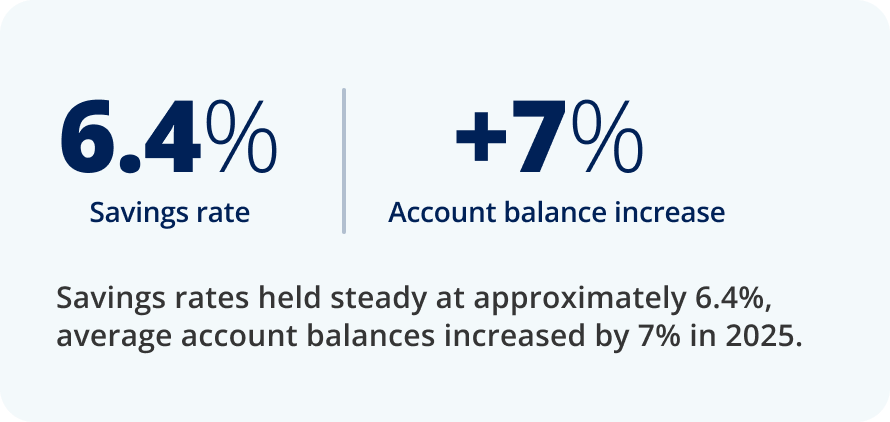

Savings behavior remains stable, but progress is gradual

While savings rates held steady at approximately 6.4%, average account balances increased by 7% in 2025. These trends reflect continued participation and long-term investing behavior, but they also highlight that progress toward improved readiness remains gradual. Stability alone isn’t enough without meaningful increases in savings over time.

2

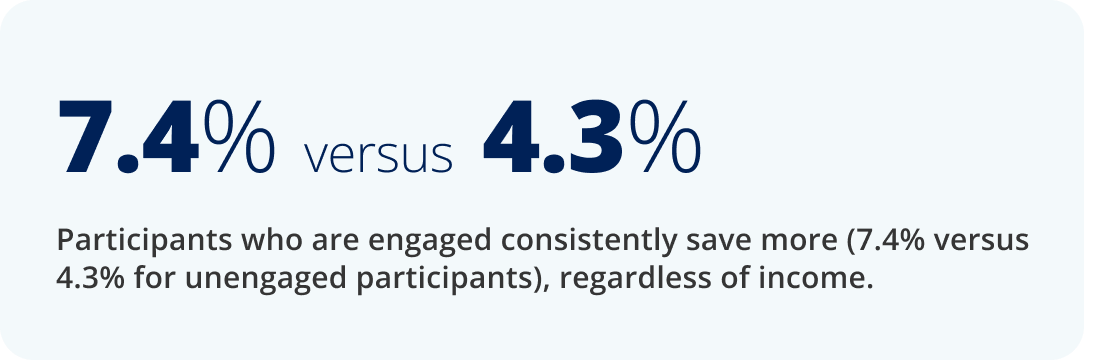

Engagement* is the strongest driver of outcomes

Engagement is the most powerful driver of participant outcomes. Participants who are engaged consistently save more (7.4% versus 4.3% for unengaged participants), regardless of income. In fact, lower-income participants who are engaged save at higher rates than unengaged participants who earn double the income. This reinforces a clear pattern: Engagement has a greater impact on outcomes than income alone, making it one of the most effective levers for improving results.

3

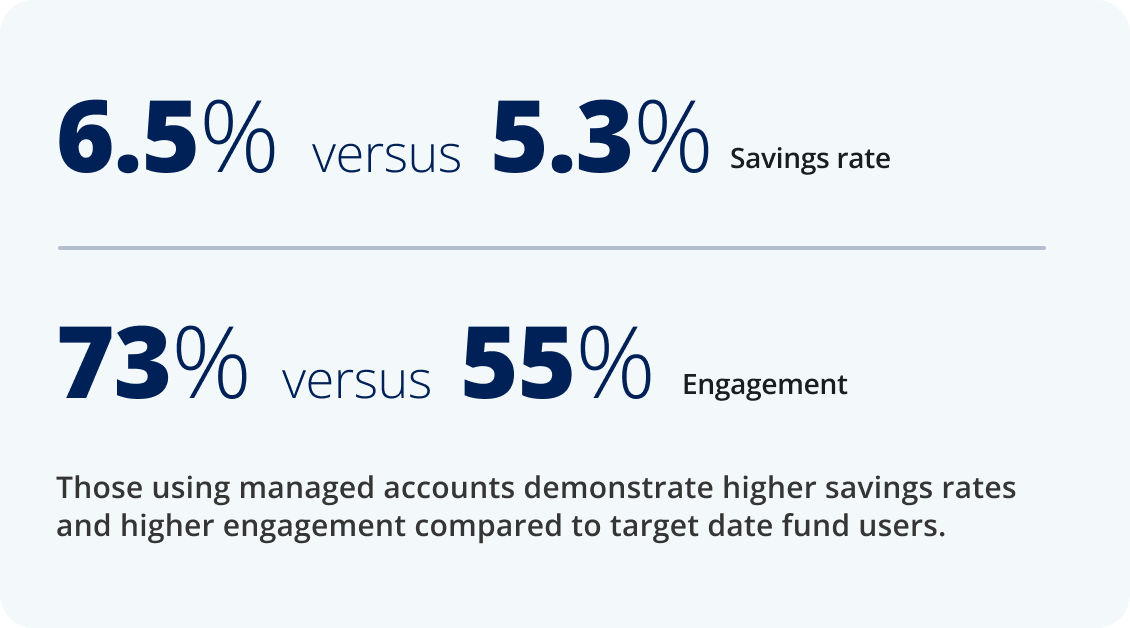

Participants are shifting toward use of advice and guidance services in a more complex environment

As financial complexity increases, participants are moving away from self-directed approaches and toward more structured, professionally managed solutions such as managed accounts, target date funds, and risk-based funds. A deeper look reveals that those using managed accounts demonstrate higher savings rates and higher engagement compared to target date fund users. This shift reflects a growing need for clarity, support, and more informed decision-making.

4

Financial realities differ across the public sector workforce

The public sector is not a single workforce. Savings behavior varies meaningfully across segments, from 6.1% in state plans to 9.2% in K-12 plans. These differences reflect variations in tenure, compensation, and financial priorities, highlighting the importance of understanding workforce-specific needs rather than relying on averages.

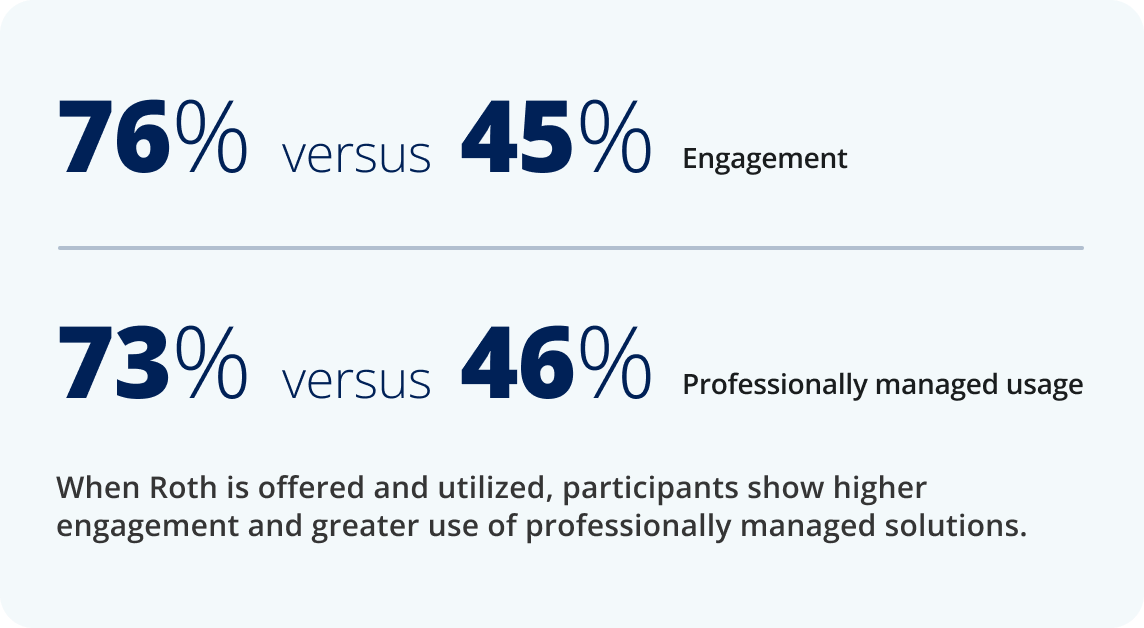

5

Plan features can help reinforce stronger participant behavior

Certain plan features are associated with stronger participant outcomes. When Roth is offered and utilized, participants show higher engagement, greater use of professionally managed solutions, and more active plan behavior overall. These patterns reinforce a broader shift: Outcomes are being shaped not just by participation, but by how participants interact with plan features and make financial decisions.

What comes next?

The system is stable, but better outcomes will depend on what happens next.

As participants navigate more complex financial lives, retirement plans are becoming part of a broader financial ecosystem. Improving readiness will likely require helping individuals connect their retirement strategy to their full financial picture, increasing engagement, and expanding access to help.

The future of public sector retirement will be shaped by how effectively plans support participants in making better decisions over time.

In its fifth edition, Empowering America’s Financial Journey – Government continues to provide insight into how government workers save, engage, and prepare for retirement — revealing both a resilient system and evolving measures of progress. |

* Engagement is defined as at least one interaction in a 12-month period between January 1, 2025, and December 31, 2025, through participant website, mobile apps (Android™ or iOS®), Empower Customer Care Center, and the Empower Retirement Solutions Group and retirement plan advisors serviced by registered investment adviser representatives. This excludes IVR interactions, email, mail, on-site group sessions, individual sessions, and webinars. Engagement is calculated for all active participants.

Empower analysis of internal defined contribution plan participant data, January 1, 2025-December 31, 2025. The data covers 2.8 million active participant accounts with their current employer from government defined contribution plans with balances greater than zero. Government defined contribution plans primarily include public 457(b), 401(a), 401(k), and 403(b) plans.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. WSA-WMLPNV-WF-6325372-0626 RO5491994-0626

The content contained in this blog post is intended for general informational purposes only and is not meant to constitute legal, tax, accounting or investment advice. You should consult a qualified legal or tax professional regarding your specific situation. No part of this blog, nor the links contained therein is a solicitation or offer to sell securities. Compensation for freelance contributions not to exceed $1,250. Third-party data is obtained from sources believed to be reliable; however, Empower cannot guarantee the accuracy, timeliness, completeness or fitness of this data for any particular purpose. Third-party links are provided solely as a convenience and do not imply an affiliation, endorsement or approval by Empower of the contents on such third-party websites. This article is based on current events, research, and developments at the time of publication, which may change over time.

Certain sections of this blog may contain forward-looking statements that are based on our reasonable expectations, estimates, projections and assumptions. Past performance is not a guarantee of future return, nor is it indicative of future performance. Investing involves risk. The value of your investment will fluctuate and you may lose money.

Certified Financial Planner Board of Standards Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design), and CFP® (with flame design) in the U.S., which it authorizes use of by individuals who successfully complete CFP Board's initial and ongoing certification requirements.