Empowering America's Financial Journey 2026

Empowering America’s

Financial Journey™

Fifth edition

Empowering America’s

Financial Journey™

Fifth edition

Workplace retirement plans have made steady progress over the past five years. Participation remains strong. Savings behaviors are holding. Engagement continues to grow, even as the financial landscape evolves.

That progress reflects a durable foundation.

But resilience is not the same as readiness, especially as people continue to navigate increasingly complex financial lives that extend well beyond the retirement plan.

In this fifth edition of Empowering America’s Financial Journey, we expand the lens. We combine the behaviors of 6.7 million participant accounts with insights from more than 1,000 plan sponsors.

For the first time, this brings both sides together: what individuals are doing and how plan sponsors are making decisions.

The result is a clearer understanding of what’s working and where new opportunities are emerging.

Key Insights

1

Clarity and engagement drive stronger outcomes.

Engagement continues to be one of the most powerful drivers of long-term progress, but its effectiveness can often depend on how clearly people understand their financial situations and what steps to take next. Engagement can be more effective when it’s intentionally built into plan design, not treated as a separate communication effort.

2

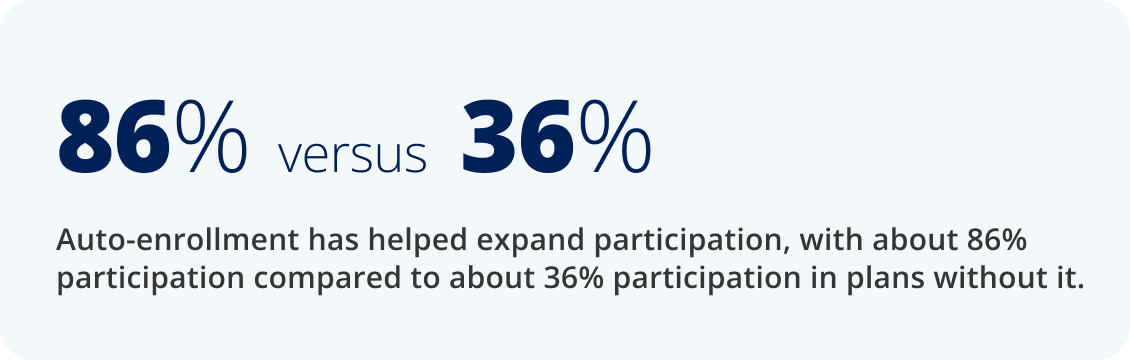

Access has improved. Progression is the next opportunity.

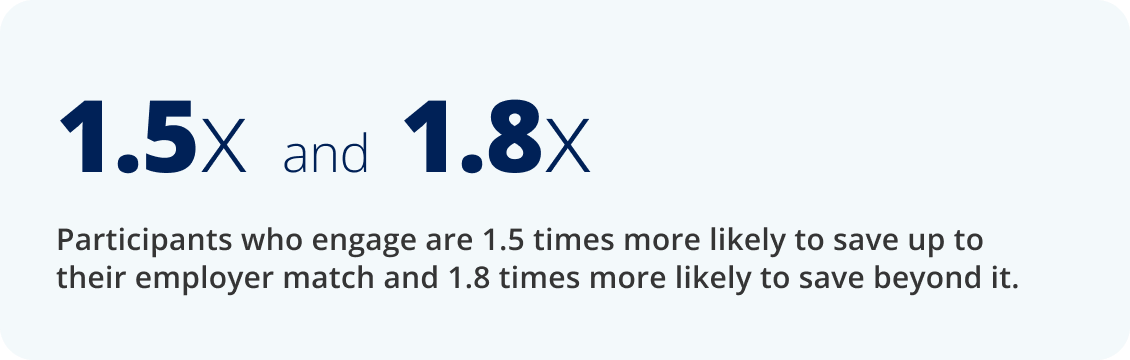

The next step is to help individuals build momentum and increase savings over time. When automatic features aren’t paired with engagement strategies such as escalation, reenrollment, and access to advice, participants often remain at low default contribution rates. Over time, this can become even more pronounced, as these participants may fall short of the savings rates often needed later in a career, when more personalized guidance and advice become increasingly important.

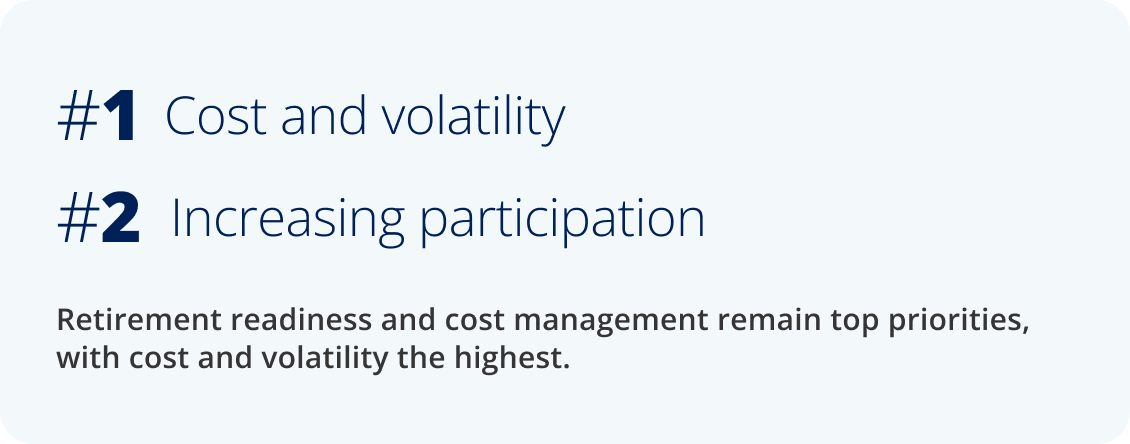

3

Sponsors are balancing outcomes with responsibility.

Sponsors aren’t choosing between retirement readiness and cost management, though; they’re managing both in tandem. These tradeoffs can influence how plans are designed and how much support participants ultimately receive.

4

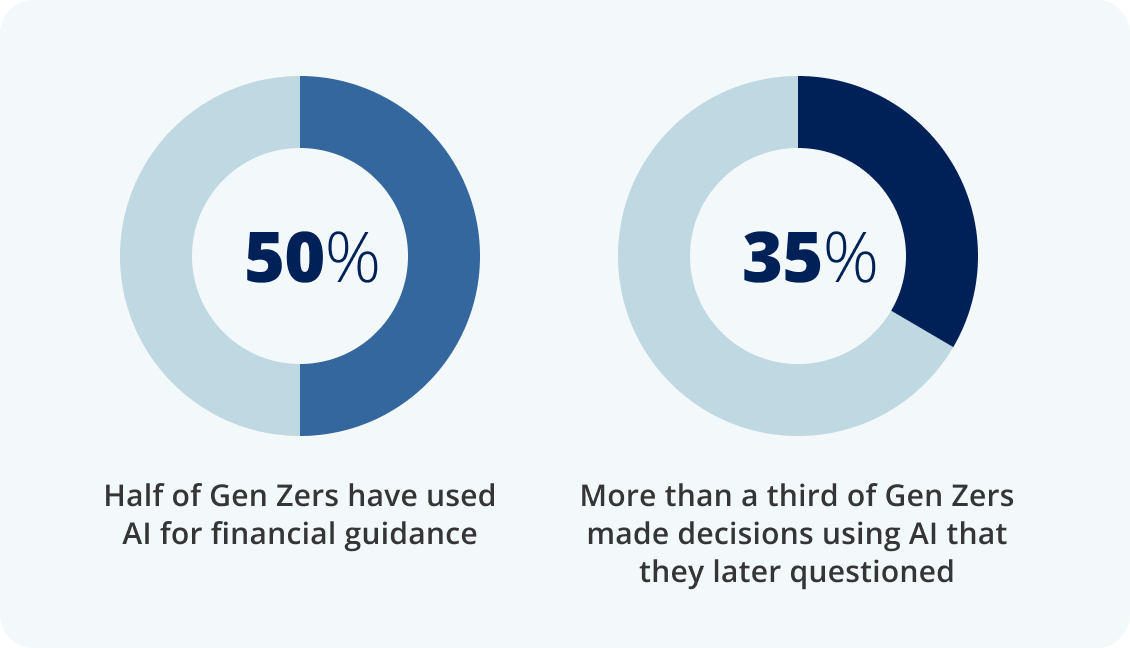

More access is creating new expectations.

Participants have more tools than ever, including artificial intelligence (AI), and are engaging in new ways. The opportunity is helping turn access into clearer, more confident decision-making. Access alone doesn’t lead to better outcomes without the context and direction to act on it.

5

The system is expanding beyond retirement.

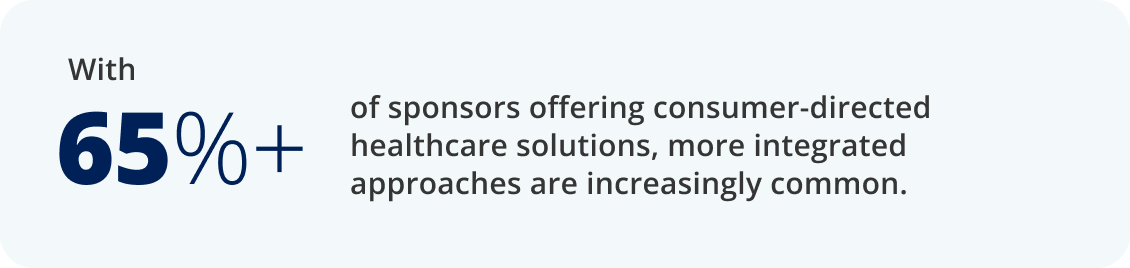

Retirement plans are increasingly part of a broader financial ecosystem connected to healthcare, equity compensation, and overall financial well-being. This creates a growing need for more coordinated support and guidance across an individual’s full financial picture.

We’ve already seen meaningful progress. What comes next is turning participation into sustained progress, improving financial clarity, and connecting retirement to the broader financial realities people face every day. This is an opportunity to create a more integrated, more personalized experience that connects financial wellness, long-term planning, and advice to support how people navigate their financial lives at every stage of the journey.

Explore the full study to see how retirement plans can evolve into more cohesive, personalized financial experiences that help participants take action. |

Empower analysis of internal defined contribution plan participant data, January 1, 2025-December 31, 2025. The data covers 6.7 million active participant accounts with their current employer from corporate defined contribution plans with balances greater than zero. Corporate defined contribution plans primarily include 401(k) plans from for-profit organizations. They do not include 401(k), 403(b), and 457 plans from government institutions, not-for-profit organizations, or Taft-Hartley plans or nonqualified and other supplemental plans.

The 2026 Empowering America’s Financial Journey™ (EAFJ) plan sponsor survey includes data collected from March 4-19, 2026, via an online survey of plan sponsors from organizations that currently partner with Empower. A total of 1,076 plan sponsors participated.

Empower refers to the products and services offered by Empower Annuity Insurance Company of America and its subsidiaries.

“EMPOWER” and all associated logos and product names are trademarks of Empower Annuity Insurance Company of America.

©2026 Empower Annuity Insurance Company of America. All rights reserved. WSA-WMLPNV-WF-6190600-0526 RO5414686-0526

The content contained in this blog post is intended for general informational purposes only and is not meant to constitute legal, tax, accounting or investment advice. You should consult a qualified legal or tax professional regarding your specific situation. No part of this blog, nor the links contained therein is a solicitation or offer to sell securities. Compensation for freelance contributions not to exceed $1,250. Third-party data is obtained from sources believed to be reliable; however, Empower cannot guarantee the accuracy, timeliness, completeness or fitness of this data for any particular purpose. Third-party links are provided solely as a convenience and do not imply an affiliation, endorsement or approval by Empower of the contents on such third-party websites. This article is based on current events, research, and developments at the time of publication, which may change over time.

Certain sections of this blog may contain forward-looking statements that are based on our reasonable expectations, estimates, projections and assumptions. Past performance is not a guarantee of future return, nor is it indicative of future performance. Investing involves risk. The value of your investment will fluctuate and you may lose money.

Certified Financial Planner Board of Standards Inc. (CFP Board) owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™, CFP® (with plaque design), and CFP® (with flame design) in the U.S., which it authorizes use of by individuals who successfully complete CFP Board's initial and ongoing certification requirements.